Well it is that time again – time for up and down and down and up. My question is have investors and traders finally accepted that there is more upside to the Fed Funds Rate or not?

Last week the S&P500 moved lower by just over 2% last week from the close the previous Friday, although the index moved in a range of around 7% during the course of a wild week caused by the CPI report as well as the FOMC meeting and interest rate hike. Of course Jay Powell slapped markets to reality making sure it was understood that more interest rates were yet to come.

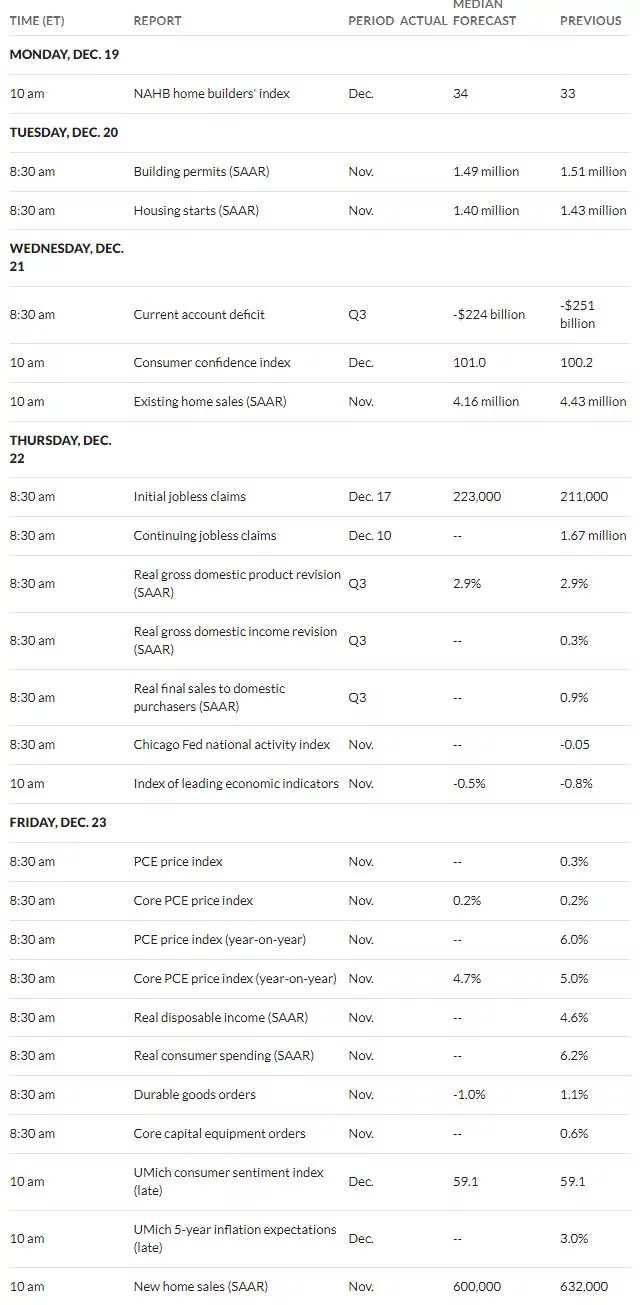

The 10 year treasury moved in a range of 3.42% to 3.63% before closing the week at 3.48%. Honestly with important economic news I would have thought interest rates would have moved more violently and at higher levels. This week we have bunches and bunches of economic news–most of which are not likely newsworthy, but the personal consumption index (PCE) on Friday is most important and it will come on a day of low volume. The Fed claims that this inflation indicator is important to them.

The Federal Reserve balance sheet moved higher by less than $1 billion – looking for a plunge in assets in the next week or so as the rate of runoff has slowed in the last few weeks and we will see catch-up to the $95 billion monthly rate.

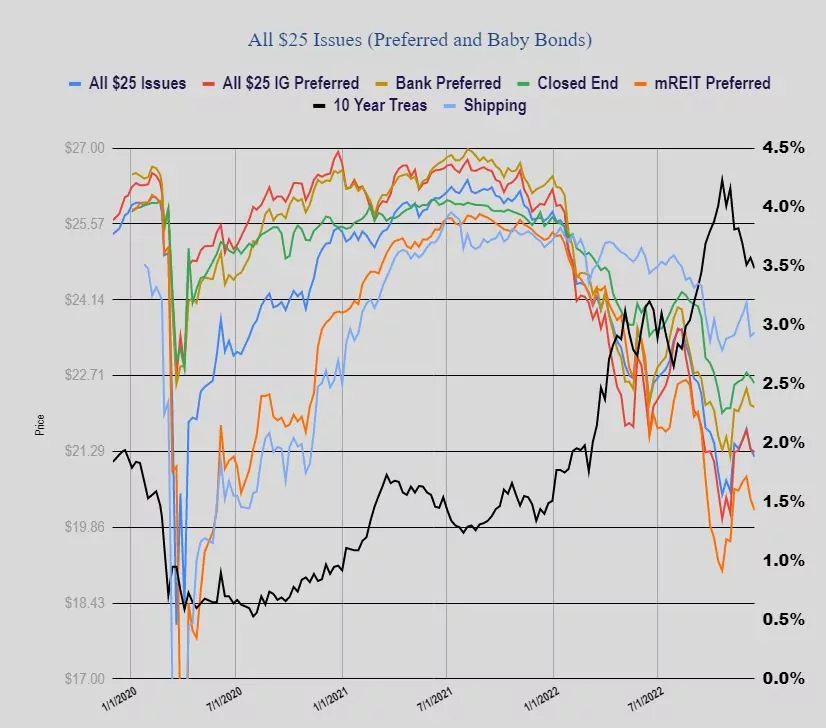

Last week the average $25/share preferred and baby bond fell by 16 cents. Investment grade issues were off 6 cents, banking issues off 4 cents, mREIT issues off 21 cents and BDC baby bonds were flat.

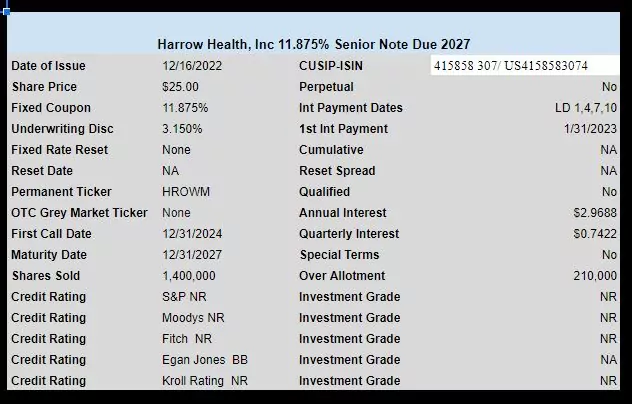

We had 1 new income issue price last week with Harrow Health (HROW) pricing a new baby bond at a huge 11.875%. The other issue that HROW has outstanding is a 8.625% issue trading at $23.12 -theoretically this issue should trade much lower today. This issue will trade in the next week or so under ticker HROWM–no OTC grey market trading.

Talk about a weekly kickoff just got back from beer run and grocery store fired up this tube. my “stink bid” from a few weeks ago filled for 500/sh of GDV-H@ 23.22. that’s over $500 cap gain forget the dividend. learned this at III, thanks guys happy holidays

Mike, You inspired me to take most of the cash in my wife’s IRA and put it into buying her some GDVprK. Only a 4.25% coupon but at $19 purchase price that comes out to 5.6%. If/when it ever gets called, there will be a 31% capital gain. To preserve domestic tranquility, I try to keep anything in her account investment grade. She already met her rmd for this year so it was idle cash.

Vinny,’ in an ira that can be a in kind RMD distribution when the time comes, 72 or when ever, 5.6% qualified dividend ain’t bad. Mike

Mike, The qualified part doesn’t really matter because anything coming out of her IRA gets taxed at our marginal rate. What impressed me more was the investment grade.

Mike – What are you getting at regarding “in an ira that can be a in kind RMD distribution?” What’s possible? I always satisfy RMD by withdrawing cash… Not the best way to go???

2WR, you can withdraw any holding you have in an IRA and have it count towards your MRD. So it does NOT have to be cash. They use the value on the day of the transfer to count towards the MRD amount. We did this in an account a few weeks ago and have done it for years.

2wr

If you want cash- but you can do in-kind transfers of any stocks to your taxable brokerage account. Those that are down and have good chances of rising again make good transfers, plus- you don’t stop those divs.

Gary been doing this for years I’m 83 now.

2WR, you can also have any part of your RMD donated as a qualified charitable distribution (QCD) to the charity of your choice (If your broker supports it). I donate appreciated stock but look forward to being able to use this option when I turn 72.

Thanks, all…. I realize I don’t have to take out cash and have never liquidated any securities in order to do so….. But what’s the advantage of taking out anything that is possibly down in value now? Does your holding period start all over again once you transfer a security out? If so, then any future appreciated sale is going to be taxed the same as if I leave it in the IRA UNLESS I plan to hold it for longer than a year once transferred out, right?

As you can tell, I’ve never paid much attention to tax efficiency when considering RMD amounts…

2WR, think about the case where you try to keep an account 100% invested. You do no have any cash available to make the MRD. In those cases, we usually transfer Bonds/CDS/UST’s to make the MRD. It lets you hold the bond to maturity without forcing a sell to cash. Obviously not every IRA has an allocation to fixed income, but many do and this might fit. . .

Thanks…. I guess that doesn’t apply to me because I always seem to have enough cash hanging around to make the RMD

2WR, when you hit 100, you will have to take out ~ 15% per year, so that would be a large cash balance to carry. And yes, we are pushing that in one of the accounts we manage. . .

2wr, according to https://tickertape.tdameritrade.com/retirement/in-kind-ira-distributions-stock-rmds-17385, an in-kind transfer a) resets the basis to the value when you withdraw and b) resets the cap gains clock as well.

SWVXX yield over 4% (4.03%) this morning

Schwab hasn’t posted for Dec — where did you find it?

just click on the SWVXX symbol in Schwab.

Yeah, they are holding interest payments until 12/31 since it’s the end of the year.

I see where it came from- ‘7 day yield’, but that is not a declared div- which I was hoping to find.

I’m holding SNOXX – same deal so far. And I know about the hold to the 30th.

thx

Yes isn’t it great $Market funds are back in vogue …..probably ramp up to 4.25-5% in a few months. Beating a lot of AAA bonds.

…..probably ramp up to 4.25-5% in a few months. Beating a lot of AAA bonds.

SPAXX the FIDO sweep ac I use is even up to 3.50%..dont have much in that in my 3 ac anymore w all the pfds I have been buying since the June swoon.

The huge refi needing to take place in CMBS in the next 2yrs may be the thing that pushes the FED to back down and/or shut QT. One of the main reasons for QE was to prevent destroying commercial r/e, one of their biggest concerns back then. They are setting up for disaster imo. Early signs may be seen if and when r/e companies/reits draw down bank lines, which I have not seen yet. So far albeit at higher rates financing is able to be done, even ofc reits are getting money like BDN, HIW, BXP..

Most folks starring down big losses this year in 60/40 or other portfolios may turn more and more to pfds seeing rates of 6.5-8% and more that have been tested in worse situations, of course many will go in cash as well. Fidelity and others are already allocating to their funds. 2023, here we come!

Hi Bea – you aren’t that worried about Reits like SLG, VNO, Hpp etc?

I sold my Slg pri for $2 loss just because I am concerned how poorly the common behaves

No -that is what makes a market. But you have to look at your own risk tolerance and if it makes you nervous, sell. I see nothing wrong with tightening up your risk tolerance putting your SLG pfd money somewhere else. I can appreciate that. I am up a little on my SLG pfds and will keep.

SWVXX – has a 180 day holding period otherwise you pay a $50. Fee a TD.

BIL could be nice substitute.

I don’t think so, I’m in and out of that fund (SWVXX) on a weekly basis for trading fixed income and preferred.

Schwab Value Advantage Money Fund® – Investor Shares

A convenient way to access potentially higher yields on cash

No transaction fees to buy or sell

At TD that’s what they told me.

That’s outrageous. I use Schwab and don’t pay any fees or commissions on it.

I’m pretty happy with Schwab.

Only times, I’ve paid anything:

I spent $6.95 on an OTC trade for AGRIP.

Bought a bond on the secondary market and they charged me a $10 markup.

Thanks. I got somebody who gave me false info.