Well here we go once again going into what is 100% certain to be an exciting week with plenty of economic news to drive markets up and down.

Last week the S&P500 traded in a range of 3933 to 4034 -relatively speaking a quiet week – a range of just 2.5%. The index closed at 4026 – near the high. Of course the week was just 3.5 trading days and portions of those days were light on volume. This week is destined to be much more volatile with many economic releases of importance.

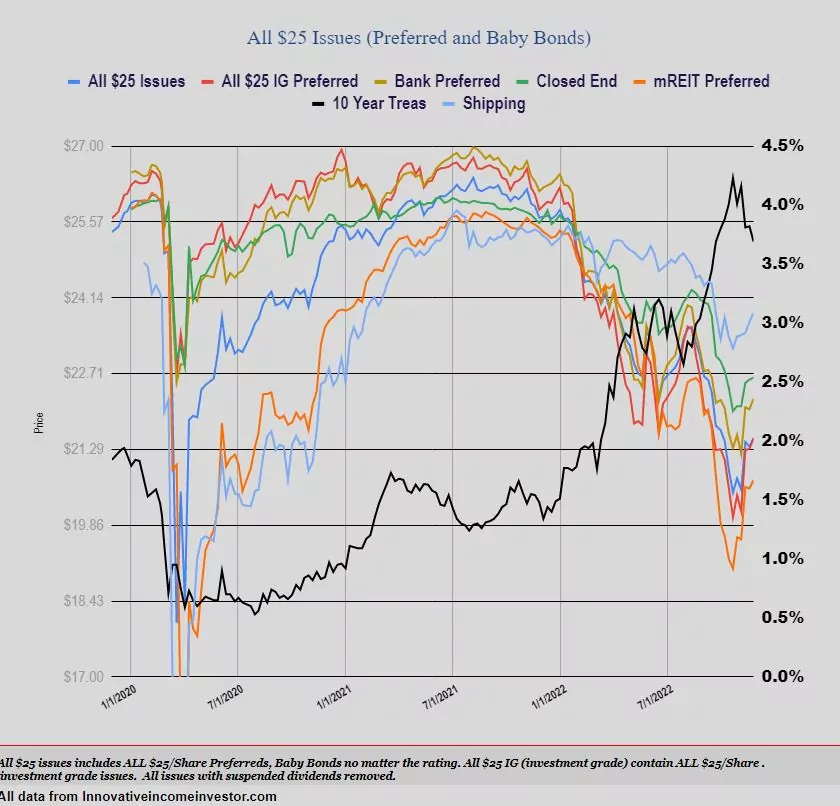

The 10 year treasury traded in a range of 3.68 to 3.83%, closing 3.69% – perfect! A nice narrow range which keeps income issue moving a little higher. Whether rates move up or down as long as they don’t move too quickly preferreds and baby bonds won’t react much.

The Federal Reserve balance sheet data was not released on Thursday as is the norm – with the holiday on last Thursday. We should see the number later today. Of course we remain on a $95 billion monthly reduction schedule–we are creating a little room for the next quantitative easing cycle (when it comes–and it will come but we don’t know when).

Last week we had green prices on $25/share preferreds and baby bonds. The average share moved higher by 16 cents. Investment grade issues moved 19 cents higher while banking issues moved 20 cents higher. CEF preferreds only crept up by 4 cents with mREIT preferreds up 17 cents. We are now about 5% higher overall than 4-6 weeks ago.

Last week we had no new income issues priced.

https://seekingalpha.com/news/3911623-affiliated-managers-group-upgraded-to-buy-at-jefferies-on-2023-growth-outlook

Tim, your last SA article got a mention this morning in the news feed.

Eladio–SA doesn’t differentiate between the baby bonds which I wrote on and the ‘main ticker’ of the common shares. Oh well.

10 year – if we are going to get a higher high in yields and I think we will then support should hold in the 3.56% – 3.48%. Let’s see if it holds. Thanks again Tim for all your work to keep this site going. ATB

Thanks TimH