Well here we go again. Will it be a wild week–as most have been in recent times or will it be a little more calm this week? A few things to watch this week are the release of FOMC meeting minutes on Wednesday afternoon–I am certain there is little to no new news in the minutes–but you know this market can react to what is already known. On Friday we have PCE (personal consumption expenditure) inflation. Expectations are for improved readings from a year ago–of course if this is not the case obviously the market will react.

Last week the S&P500 traded in a range of 3810 to 4091 last week and closed down 3% from the previous Friday–although it took a massive rally off the low Friday to even end the week with just a 3% loss.

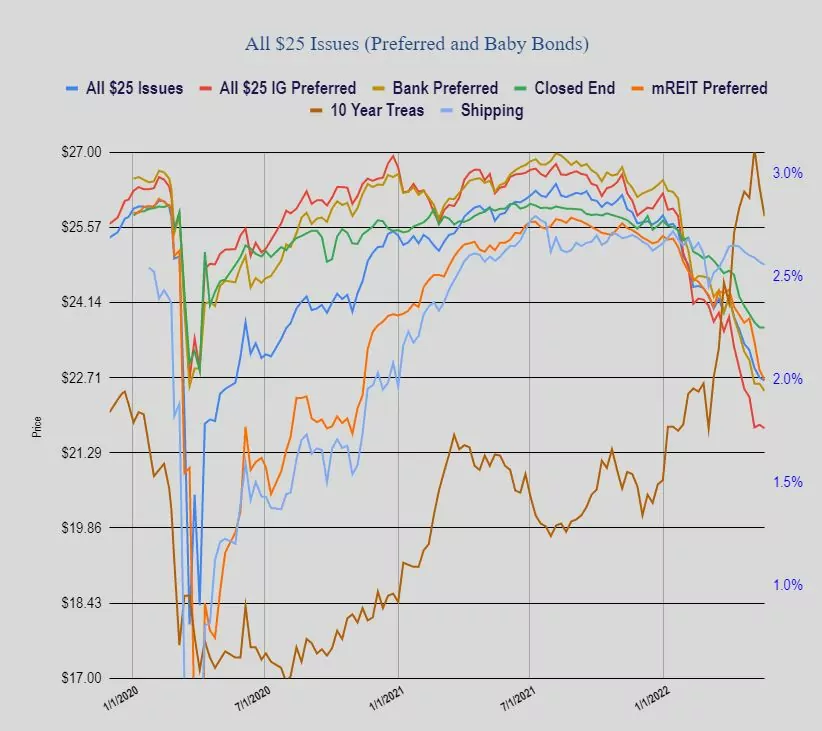

The 10 year treasury traded in a range of 2.77% to 3.01% before closing the week at 2.79% which is a close 14 basis points below the previous Friday. At this moment the 10 year is trading a few basis points higher at 2.82%.

The FED balance sheet rose by $4 billion. We are just 7 days away from the start of the balance sheet runoff—also known as ‘quantitative tightening’.

Last week was a ‘flattish’ week for $25/share preferreds and baby bonds. While interest rates moved lower last week shares of income issues moved slightly lower–getting tossed out with common stocks by nervous nellies.

The average $25/share preferred and baby bonds fell by 6 cents last week. Investment grade fell 2 cents, banks fell 7 cents, CEF preferreds were flat with shippers off 6 cents. With a little market stability this week we could see a bit of a bounce in income issues–but of course market stability is not very likely.

Last week we had no new income issues priced, but we did have Conifer Holdings (CNFR) register a new issue of baby bonds–but no pricing of the issue has occurred.

Although I am not complaining, I am bewildered as to why my bonds and preferred stocks did so well today (May 25th)?

Today the market moved higher after the Fed minutes were released …. “the rate increases the Fed already has in mind were “not going to be pleasant” as they force Americans to pay more for home mortgages and auto loans, and possibly dent asset values.”

I can’t believe that the two .5% interest rate hikes coming in June and July have been fully priced in yet. I also don’t see that these are anywhere near enough to tame inflation. Not with the profligate deficit spending by our government.

HI..Tim today looks, Normal, investors taking money out stocks and putting them in bonds and preferred stocks,for safety, hopefully? the sell and run..is slowing.. Georges

In lieu of the poor Walmart and Target earnings, has the market discounted the possibility of poor earnings coming up 2nd and 3rd quarter? 10 year Treasury yield looks like it is starting to roll over? That puts inflation and the Fed in a squeeze!