Last week the S&P500 fell by about 2.9% as the Russia/Ukraine war rages on and we are not seeing a likely resolution on the horizon.

The 10 year treasury traded in a fairly large range of 1.71% to 2.2% before closing the week at 2.00%. Rates are sharply higher this morning around 2.08% as we stare at a Fed rate hike of 25 basis points later in the week. The 2 year treasury is trading over 1.82%

The Federal Reserve balance sheet rose by $6 billion last week.

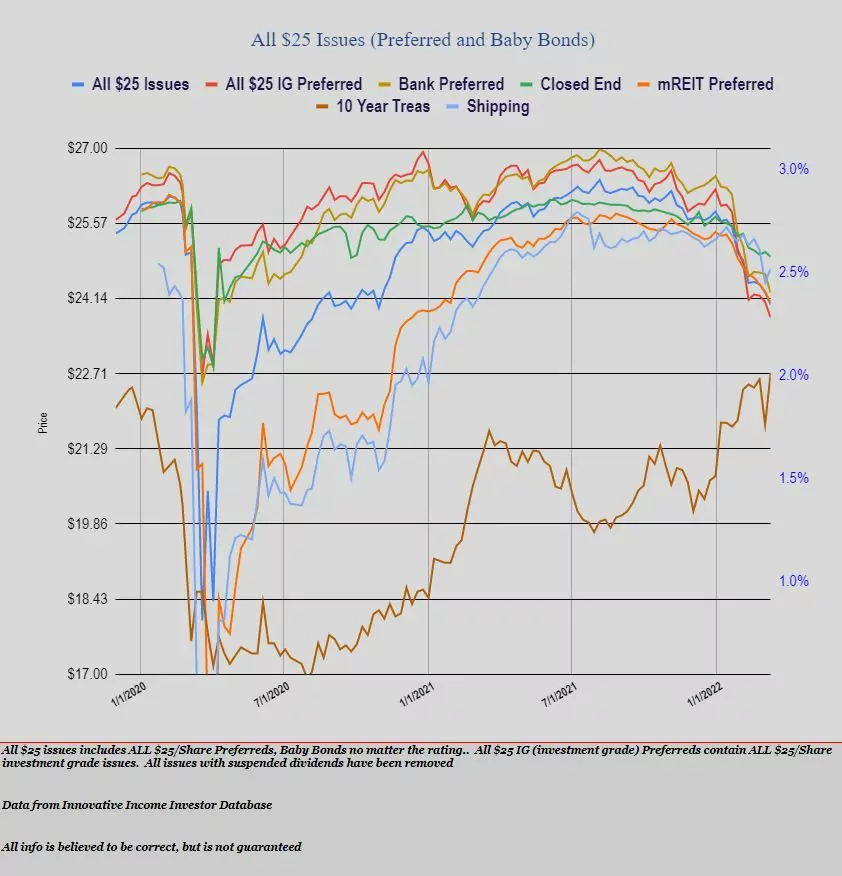

Last week was another ugly week in $25/share preferred stock and baby bonds as the average share fell by almost 1% (23 cents). Investments grade issues fell by 30 cents, banking issues fell by 36 cents, closed end fund preferreds fell by just 9 cents. So we continue to see prices falling, which should be no surprise, thus we will have more favorable pricing for future investments–of course there will be some capital loss pain to be endured as interest rates move higher.

Last week we had not new income issues priced.

Remember when inflation was transitory….

10 year and 30 year treasuries way up today by 11 basis points. 30 year now at 2.46%

I’m long SPNT-B now. Good value at this price.

Any foreign taxes withheld from dividend payments? Thanks

David P

Looks like things are falling again today because they are falling. I am noting the low volume of trading on many of my holdings which are down anywhere from a little bit to 1% or more. On no news. Seems that people probably get frustrated somewhere and sell, and with many of these holdings it does not take much volume, not much at all, to move the price significantly. While it is frustrating, I check the new on each of my holdings and see no fundamental reason for a decline. What I call then dropping because it’s dropping. At some point, difficult to know when, it will all reverse. Then people will say, wait I can get a 7% yield for THIS? And buy. And then then it will start to melt up. Wait it out. My 2 cents.

Larry – Don’t you think the fundamental reason could not be necessarily company specific but perhaps more due to the rise in Treas yields and the upcoming Fed announcement?

Yes, but all of this information has been around for a while. This is across the board, affecting things with floating rate features that should be much better protected on interest rate risk.

“Dropping a lot today”

Indeed. Any idea why?

Hi!

What do you guys think of TIPS right now?

Thanks.

D.

In this environment when looking to add to a fixed-income portfolio that has many IG rated low coupon preferreds that are largely in the red as most bought before mid-Jan 2022 what should one be looking to add?

Fix-to-float callable soon in next few years such as STT-D yielding 5.8% or buy low coupon IG preferreds like JPM-M trading in low $20s and thus yielding 5.1% with better appreciation potential?

msquare..JPM-L has a little higher coupon and at $21.3x yields 5.4x%. Little more current yield, still nice discount

I would think your going to have to be happy with the approximately 5 to 5.4 yield for a very long time since these will never be called unless rates return to the ultra low rates of our past. Remember that JPM is only paying the issued rate which may be along time before they can issue another preferred at those rates again. And what about the principle with even higher rates? This is just my reason for not touching any of these.

William,

What would you like to get in the way of a yield from a preferred that is non-cum, QDI, and issued by JPM? Eventually one has to bite the bullet and buy. One will probably never catch the pinnacle of yields. Do you feel “like” we are going back to the early 1980s or early 2019? I guess I am asking because we often paralyze ourselves from buying because we “fear” things can get worse. At some stage we have to set a goal and stick to it based on some “common sense” factors. I realize inflation is the monster in the closet but eventually that too shall pass unless you think we are heading to 1970.

So what would make you happy? Do you have a number ready to act on? Let’s assume you still plan on living for another 20 years to give some type of base line here on assumptions.

Buying things like ABR-D with plus 7% yield as I can live with that should it not ever be called. I consider these from high quality companies and management that I thoroughly research financials, which I am comfortable doing.

Dropping a lot today