Last week opened with the SP500 at 2558 and hit a high of 2641 before closing the week at 2488–around a 3% loss on the week.

The 10 year treasury traded in a range of .57% to .72% before closing the week at .59%.

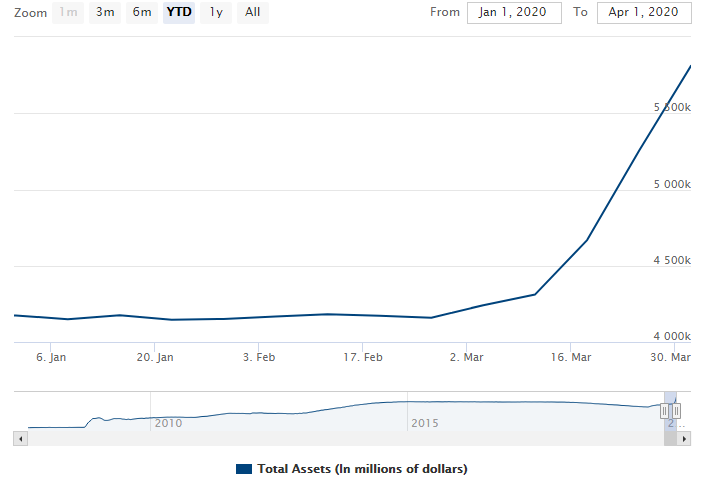

The Fed Balance sheet grew by $600 billion last week–a 3 week total of $1.5 trillion to a new highest balance ever of $5.8 trillion. The printing presses are running as fast as they can run.

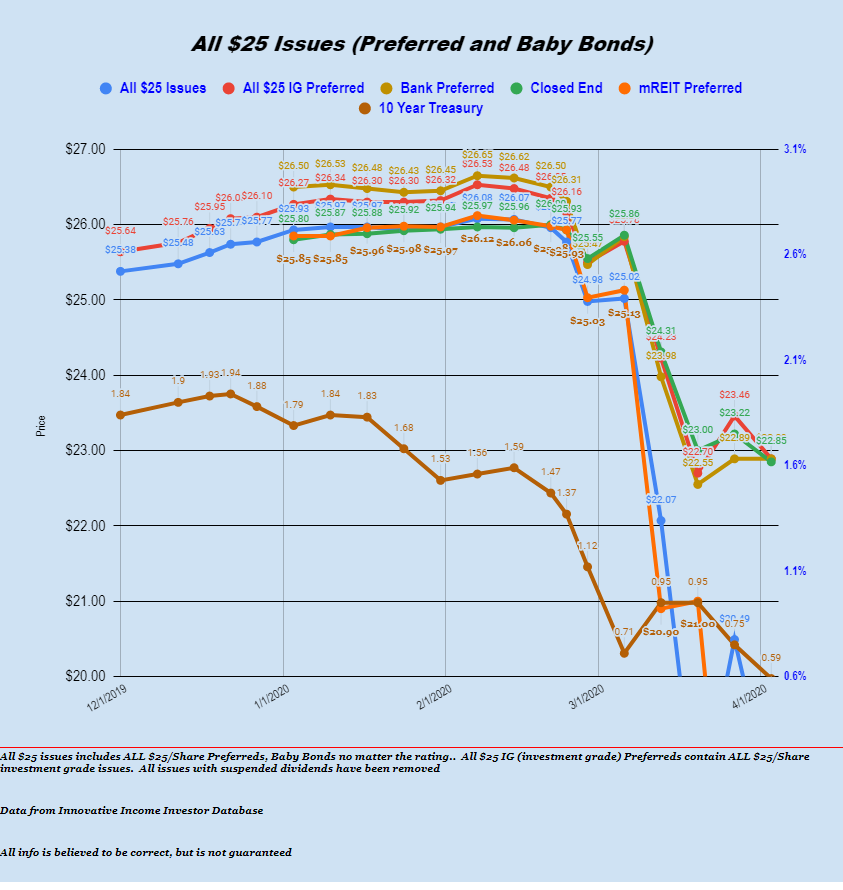

The average $25 issue of preferred stock and baby bonds fell by about $1.50/share last week to $18.90.

Banking issues were exactly flat last week at $22.89. mREIT issues were hammered much lower–by $5.50 per share and this remains a very dangerous sector. CEF, Utility and investment grade issues were all lower, but only by 1-2%.

So we are kicking off the week with strong futures markets–in my opinion too strong (but maybe I’m wrong) and I know that I won’t be buying today–as shown by last weeks action in preferreds and baby bonds it remains ‘early in the game’. While it is so tempting to start to pick up shares investors have to be very careful to not get carried away and instead to ‘leg in’ to positions.

I am about 55% invested so I remain with high levels of dry powder–most of my holdings are utility and CEF preferreds and baby bonds bought at lower levels–this is where I prefer to be now–but I am chomping at the bit to buy some lodging and housing REIT issues, but it is too early for these segments. I am trying to be patient.