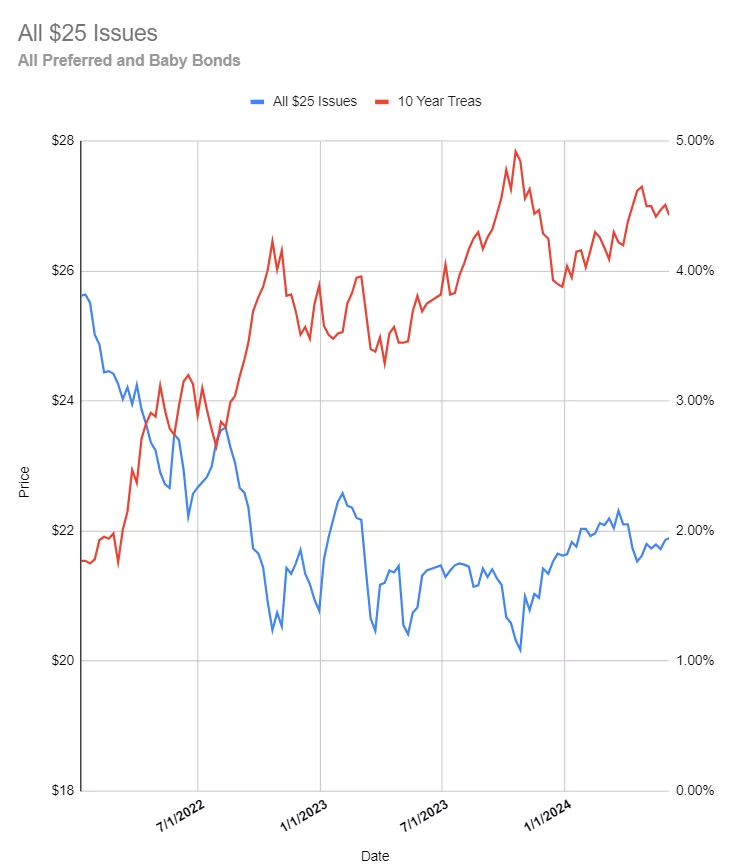

Well once again the the 10 year treasury yield is falling – now at 4.19% this morning. The bet now seems to be a ‘soft landing’ in the economy. Certainly the most recent data points that way–BUT it is only one months worth of data. Markets seem to get a little overly stimulated to declare ‘soft landing’ only to get whipsawed when the next set of data runs contrary to this thought. Today and next week we don’t have inflation or employment news being released so it would seem we should see some drifting in the markets.

I continue to study the chart below–is there any doubt that the 10 year treasury yield and the average $25/share baby bond and preferred trade price move in an inverse fashion? As I have stated before I expected the 10 year treasury yield to drift lower into the fall and then start to move higher based on the huge over supply of debt being issued by the treasury–I hope I am wrong and the move higher doesn’t occur.

This morning I have entered buy orders on both the Spire 5.90% perpetual preferred (SR-A) which is trading around $23.90 and for the CHS 6.75% perpetual preferred (was fixed to floating, but now is fixed) (CHSCM) which is trading around $24.95. So today I am buying for the ‘safe’ bucket. The Spire issue is split investment grade at BBB/Ba1 while the CHS issue is not rated, although I personally view it as investment grade. I reviewed the most recent earnings release from Spire from 5/1 and the earnings were excellent–very solid. CHS relesed earnings which were down from the year ago quarter–but this agricultural cooperative (or maybe one considers them a crude oil refiner) has shown variation in income for years, but over the course of time this company is very profitable.

Bfs and Rexr preferred issues ready to pop any moment now

Bfs and Rexr preferred issues ready to pop any moment

Definately !! one of my favourites with huge upside potential and e nice yield !

Took 25% position in WRB-E. My type of issue. IG by both Moody’s & SP. 6.29% under PAR. Yielding 6.05% (coupon 5.7%).

Bought some SSSSL at $23.90

(Sutter Rock Capital Corp 6.00% Notes due 12/30/2026)

Good Morning Tim; Good buy on the CHSCM, but Iam sure you are well aware that the “call date” on that issue is SEPT. 30th, 2024. I have called them twice in the last 6 months about if they plan on calling these issues but they always give the same answer—LOL—That is something the board may look at in the future but at this time there has been no decision. Like I’ve said before I truly suspect some really Big Farmers and Big Shareholders have asked them not to call these issues. Its just a “gut feeling”. Here’s my “Case in Point” their issue of CHSCO has been callable since SEPT. 26th, 2023 yet THEY HAVE NOT CALLED IT. WHY??? And its a 7.875% issue!!!

Tim, with rates drifting down and a few preferred like term and FTF coming due or resetting over the next 6 to 8 months I expect to see a small flood of new issues coming to market or even bond issues being announced during this time to take advantage of refinancing these higher interest rate preferred. If you’re reading the tea leaves correctly then these new issues with lower rates will sink lower in price if rates go up.

Currently we could see some discounted lower yielding preferred rising in price as investors think rates will be heading lower and these below par stocks will have a combination of price growth and you can lock in a higher current yield. You can already see this as they are above their 52 week lows.

This could be a head fake if rates rise later in the year this will push prices down on the older low yield and the new just issued lower yield stocks. Guess we stay vigilant and learn to ride this roller coaster.

I am positioning similar to your thinking. This is why, I will allow the money market to increase instead of buying more CD’s. The increased dollars in my pocket for a 1 year CD versus a money market is just not attractive to me. That is because of the the lost opportunity (cash tied up in CD’s) when new issues hit the market.

Charles, you are correct in assuming rates are going down today, and may go back up tomorrow. Without the backstop of ZIRP and/or Fed buying treasuries, no one can accurately predict anything. But there is one small thing a person can do, IF they decided to play in IG fixed perpetuals. Buy the issues of the same going market yield ~30% plus under par. At least if interest rates do head lower, at least you are rewarded with a cap gain…..instead of a no cap gain call notice. About any fixed perp I own has been recently bought 30-40% under par. Those are the only ones I am personally interested in, in this segment.

I can find fixed IG issues 30% below par BUT most have meager coupon rates. Do you have a coupon rate factored into your approach? Right now, I am limiting my fixed-rate purchases to IG issues that have a coupon of 5.5%. Why? Coupons of 4% – 4.75% may be perpetual money with very little chance of being called. Issues like BAC-P concern me. Interested in your thoughts on the lower coupon rates. Thanks

All sorts of Ameren, Eversource, or NGG preferreds have actual yields of 6.25% with any patience. And as far as percentage of dividend coverage by profits from which preferreds are paid from are off the charts in safety coverage compared to any other QDI preferreds on the market. … But specifically to your question, yes, these are 4% range par issued preferreds. I personally dont want them called and want the cap gain appreciation and trading opportunities. So I basically only specifically do the ancient ones issued 80 years ago for the exact reason you do not. So our philosophies are a bit different. Now I have a few issued that will mature or shorter durations stuff. But that allocation serves the purpose you mentioned.

There is no guarantee any 6% issue will ever get called. They are all labeled perpetual and generally must be assumed to be such. So I personally dont play the game of, “this may possibly be called so I will buy it instead to protect myself”. If I want call protection, I buy issues that will ensure that. Or an almost certainty type such as an SPNT-B or a WCC-A. But those arent perfect examples being they are reset perpetuals with an outrageous reset adjustment.

Thanks for the clarification. Yes, the older illiquids are not part of my investing strategy.

I do agree that preferreds are perpetual which is why those who continually point out that long maturity dates of baby bonds befuddle me. At least baby bonds have a maturity date, unlike preferreds.

Steve, the key is to understand what you own, and stay inside your personal comfort zone. I have a different take and maybe its just because I am used to it all and been involved with them and my tolerance is different. But to me its just an is what it is. Perpetual preferreds have been around in the US since the 1800s. A long duration baby bond (specifically the subordinate debt ilk which is typically what they are) to me are the exact same thing as a perpetual preferred and trade as such. The only real major difference is the company pockets the tax break and keeps it, instead of allowing you to have it.

Grid after the 2007 to 2009 meltdown I totally understand your point of view, especially at my age.

SCE-PH went x-dividend today and I picked up some at 25.09 not the best price of the day. But I believe next qtr it starts to float.

Charles it started floating three months ago. The good thing about this issue is it quickly pays out after going exD.

Grid,

Schwab says (in answer to your statement) ….”in theory, but at Schwab we do things a little different here”

Pig, Im not a huge fan of this Schwab experience, but just like getting old, I will eventually learn to accept it.

Grid, I don’t think most of the market has it figured out yet on these SCE-PH, 15 million people in their service area and 5 million accounts. Yes they just called one trust preferred, but they usually take their time.

Charles, I think market did 3 months ago. It went about 15 cents over the bloated divi before retreating slightly before exD which is fairly normal. It will trade roughly like SPNT-B until Fed yanks the Funds rate. With a weak 2.99% adjustment, I wont fall asleep on this one.

Grid, You are completely right on these FTF Fixed to floating. Not as good as ones with a 1yr or 5yr reset. We have no idea where rates are headed in the future. Notice how with rates dropping this past month or so that companies have been taking advantage and issuing new preferred,and some have been calling preferred at the earliest call date and causing stocks to drop back down to par leaving people with capitol losses. The meager reset on the SCE-H if rates were to drop could cause it to go below par, over the last 40 years we have seen that before. That just means you buy at the lower price to get the adjusted yield and capture a possible gain when it swings the other way. It also means you have to watch more closely than you would with your old Ute stocks.

Buying 4 to 5% preferreds for my wife’s retirement plan–yielding 6 to 6.5 %. Don’t expect them to ever be called. Should be SWAN investments.

I have been also been doing this for my lady’s mad money annuity like income stream account. It will help keep minimize the times her hand is dipping into my personal money bucket.

I have a nice chunk of SR-A too. My basis is around 23.70 bot in bites, nice yield over cash rates for a quality issue. Bea

I had a large chunk of my ARCC called away overnight so now looking for a place to park the funds. I had owned that since 2017 (basis about 17.55) and have collected a ton of divvy along the way (some of it DRIPed. Plus, it’s on the high end of its long-term range so I am fine with letting it go. I may be interested to buy it back around 19 if it gets there.

Meanwhile, where do I park all those $$$?

yazzer-

An Option call on the BDC- right?

ARCC called??? Please explain. I am overweight in ARCC.

June 14 (Reuters) – Globe Life (GL.N), opens new tab has started a review of “potential vulnerabilities” in a web portal that could have allowed unauthorized access to its customers’ information, after an inquiry from a state regulator, the insurer said on Friday.

The issue was related to access permissions and user identity management, the company said, adding that it had removed external access to the portal.

Globe Life retained security experts to investigate the issue and help with remediation efforts, it said, adding that the incident has not had a material impact on its operations so far.

The company did not identify the state regulator it received the inquiry from. Insurers are not regulated at the federal level, but by the state in which they operate in.

There are like 4 main areas of concern made about GL. Problems on a web site are NOT part of them. And truth be told most if not all corporations have cyber securities issues. When trans union experian equifax got hacked it was a warning that all data bases are at risk. NOT a big deal