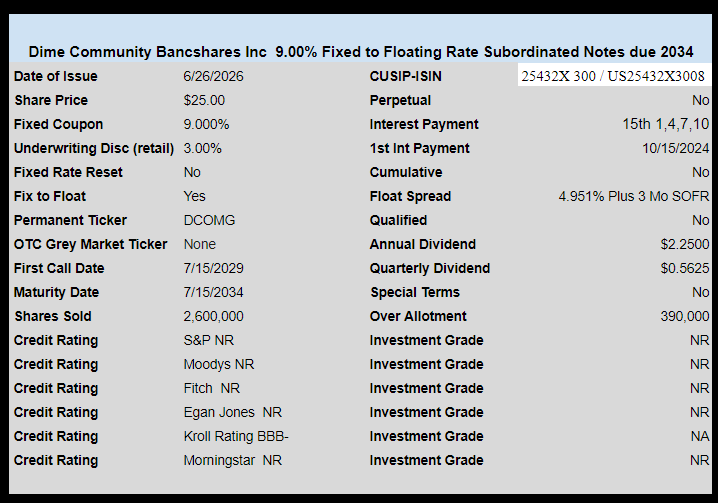

As noted in the comments section by ‘Rocky Mountain Hiker’ Dime Community Bancshares (DCOM) has finally priced their new baby bond which is a fixed to floating subordinated note with an initial coupon of 9%. Higher than I would have guessed.

Starting in 2029 the issue will float at 3 month SOFR plus a spread of 4.951%.

The issue will mature in 2034.

The pricing term sheet can be read here.

DCOMP trading with a 8.81% current yield ; why the disconnect ?

It’s a small issue and has always been quite thin.

Looks like 8.14% @16.90 down about 15¢

17¢ spread, 16619 shs Almost $10 off all time high- not sure DCOMG will be a winner even at 9%

DCOMP is a perpetual non-cumulative preferred. This is a cumulative 2034 bond, albeit a subordinated one.

DCOMG trading today 7/2 fwiw

Florida Atlantic University recently did a report on the banks with the greatest exposure to CRE relative to their size. I believe DCOMP was #1.

https://business.fau.edu/departments/finance/banking-initiative/bank-exposures-commercial-real-estate/index.php

I have seen a bank’s exposure expressed in several different ways, CRE / total assets, CRE / total office property loans, CRE / total equity, etc. All give different rankings. Exposure to CRE appears to be somewhat difficult to determine. Personally I tend to pay attention to exposure to office properties and shopping malls if I determine it as this seems to be where the biggest CRE problems are. I also don’t have hardly any of my portfolio involved in banks. Customer’s Bank and Synovus make up my two banks, and I view both as very transient parts of my portfolio. I will sell them at the drop of a hat. However, I am mindful that the hat can look fine on Friday and drop over the weekend based on recent history!

I analyzed the methodology used to calculate CRE exposure in that study and I was not a fan. Biggest thing I thought was wrong was including owner occupied CRE loans as CRE and not commercial. Those are full recourse loans and the borrower is responsible for paying the loan regardless of the value of the underlying collateral. If Google gets a loan for an owner occupied office, they have to pay off that loan regardless of whether they use it or if the office’s value falls dramatically. They can’t hand over the keys and walk away from that loan.

That said, owner occupied CRE loans are often being made to borrowers who otherwise may not be able to get a loan or certainly not one on attractive terms.

Landlord, on that report I posted the link to there was a second tab you could flip to and it shows tier one capital and several other columns I think that was more informative.

I was keeping the link on the chart to refer to banks I might be interested in that have preferred. Dime isn’t one of them.

Very good links there Charles!!!!

The equity values looks way off for many of these banks.?

Much lower than the value I see…..stock price times shares outstanding.

Any ideas Charles??

HI ,, what is a CRE report.. #1 being,,, good or bad.. ? Georges

CRE = Commercial Real Estate. Lots of large urban office properties are under pressure because of the work-from-home era, plus insane local tax and other policies. Some of the properties are being sold at very large discounts to recent valuations, so loans on bank books may be under water.

What the CRE number (for an individual bank) doesn’t show is the size of the loans, types of businesses, exact locations, and current credit quality of the borrower. So taking one metric and extrapolating an outcome may be difficult, so many are choosing to avoid the banking industry because there is no way to determine what the true exposure may be.

Further, there were a few bank blowups in the last 15 or so months, so that has investors on edge too.

CRE may also include multi-family homes (apartment buildings). That segment may be more robust than office space.

I have no plans to buy this issue and have not done any research on Dime asset mix.

CRE includes office, multifamily, industrial, retail and hotel. Office has secular headwinds from work from home, multifamily has headwinds from excess supply hitting the market, retail has headwinds from e-commerce. Hotel is a very cyclical industry with thin margins (all the fat profits go to the branding/marketing companies Hilton and Marriott). Industrial is the safest as a beneficiary of e-commerce.

The national office market has a very high vacancy rate near 20%. However, 90% of vacancies are in the bottom 30% of the market. Typically Class B and C buildings.

Landlord – in the case of DCOM they seem to have a large (31%) exposure to NY area rent controlled multi-fam. When I read that it is an immediate pass for me, but I’m sure I missing something.

Any thoughts on that particular segment?

The 9% coupon might seem high, but the market might think three-month SOFR will be lower than 5% during the back end. If you build an IRR model for the whole thing and assume the net IRR only needs to be 8%, it’s assuming a yield of about 6.5% after FTF, which implies three-month SOFR at about 1.5-1.75% (all approximate).

Today I’ve seen this new issue:

NextEra Energy, Inc. 7.229% Equity Units Due 6/1/2027

I’ve never bought equity units and no idea how they work.

Better study before you buy an “equity unit”. Many people buy these looking at yield and thinking its a preferred. Then finding out the hard way it had a mandatory conversion into common and took a financial bath. Unlike fixed preferreds which largely beat to the drum of interest rates and credit spreads, equity unit issuances ultimately will beat to the drum of the direct common stock price movement.

Grid:

Great points on the mandatory convertible equity units. Rida’s army of sheep took a big time bath on AQNU as it is now time for it to convert into shares of AQN, which have collapsed in the last 3 years since AQNU was issued.

Seeing sob story comments on SA with his truly lost soul followers getting hit for 60% losses on that one. Ouch.

Grid got into a discussion with someone about a year ago about the risk of owning a mandatory conversion BB and this was when the common was higher priced and they were trying to buy a Kentucky utility? The deal fell through and the stock price collapsed shortly afterwards. I heeded Grid’s warning and was in and out for a quick flip.

There is so much knowledge on this website — you guys are like savants. I know this a lot to ask, but can someone please teach me how to go about placing a fair value on this note given the current price of DCOMP. There are just so many variables to consider — my head is spinning. All I know is that this new issue seems super cheap. Any sharing of knowledge with respect to the valuation process would be greatly appreciated.

AF – this issue and the recently announced OXLC issue both look a bit puzzling relative to the existing preferred. So you will want to wait to see how these trade. Personally I own OXLC and ECC preferreds and am planning to focus some time on these when we see how the new OXLC issue trades.

As I have said on this board I much prefer CLO equity to regional bank common stock and prefer term preferred on CLO equity CEFs to regional bank preferred. But this is just my opinion and plenty of folks will disagree.

For the purposes of this discussion let’s assume the perpetual does not get called (seems a reasonable assumption to me).

There are three factors that I would consider here:

1)It’s a regional bank – on any given Friday the common can tank and the following Sunday there can be an “emergency” meeting with FDIC and JPM the outcome of which is that all DCOM common, preferred and Jr debt holders get zeroed out. A few days later JMP will announce how profitable the takeover was.

2)A collorallary to item 1 is that there is no meaingful difference in seniority between regional bank preferred and subordinated debt (IMO). So if this was an equivalent term preferred vs a sub note (it isn’t) I would not give up even 1 basis point for the note relative to the hypothetical term preferred.

3)Given items 1 and 2 At this turns into an interest rate play. You have to assume these notes are money good (big assumption) and then value them based on the relative interest you get compared ot the preferred. You have a fixed perpetual vs a fixed/floating 10 year note. What you can do here is build a few case scenarios in an XL spread sheet assuming different SOFR rates and see which one pays you the better return over the term of the issue. I would assume that preferred stays flat in value, the notes return par on schedule and that neither issue gets called.

One of the posters on this thread is on this track with the IRR comment.

FWIW

Thanks. It appears to me that the issuers are being forced to pay way up to get new deals done. Same thing seems like it happened with NEWTG vs. NEWTI. It’s becoming a pattern. The Oxford Lane baby bond pricing was really a stretch.

Is it me or is 9% a bit much for a Kroll rated BBB- issue? And I posted on another thread, why such a small issue at $65MM (with a potential follow-on of about $10MM). I own DCOMP so this is all just a little bit perplexing to me, especially with the deposits they are gathering from NYCB and others.

Interestingly, the common is doing well and actually broke out of it’s downtrend, albeit on low volume. But DCOMP is down since the filing.

If this is priced at 9%, then DCOMP, at a minimum, should be trading a couple bucks lower than it is today. Otherwise, I don’t have anything to say about Dime, other than its apparent high CRE exposure.

Why would dcomp which is yielding an approx 8% QDI be a few bucks lower then it’s current price compared to the baby bond that is just interest? I feel if the bank cannot pay the preferred there is very little hope for the baby bond. I value 8% QDI more then 9% interest which for me will end up getting taxed more then i pay for qualified dividends. Cap stack wise… in this situation.. I will probably treat them equally.

Its likely a Tier 2 capital raise. Being its a sub note, it isnt any “safer” than a preferred. Assuming the company stays profitable its actually cheaper for them to issue a 9% sub note than an 8% QDI preferred.

Are you interested at par or below? Right after I decided to withdraw from the preferred stock/baby bond area and buy T Notes and CDs, I’m slowly being sucked back in with pricings like DCOMG and NEWTG.

This isnt any indictment on the issue, but I dont see myself participating. Never been a big “bankie” person to begin with, but I already have three and that is plenty for me. Have a decent amount in BANFP and not eager to part with. Already have 2WR’s personal bank NEWTG , and just reentered WAFDP. Not eager to sell anything for it, and dont have any more real CD maturities until August. And if I decide to put those soldiers into the line of fire at that time, I doubt it would go into that sector either. Keep in mind this is a just a personal philosophical/psychological hangup, not a true investment strategy reason.

Why is a 9% note cheaper to issue than an 8% preferred (where the dividend can always be deferred if needed)?

Roger my working assumption is the company is viable and remains so. If I were not assuming that I don’t think either is a viable purchase. That being said the 8% preferred is paid in after tax dollars by corporation. The sub note is paid out in pre tax dollars. So counting the NY state and fed tax rate that is about 27% give or take. So issuing the sub note is effectively costing Dime comfortably under 7%.

Gridbird, Interesting point about the note being paid in pre-tax money while the preferred is paid in after tax money as long as they have profits. Is this true also for baby bonds? It seems with interest rates being raised that companies are issuing notes and baby bonds more than preferreds.

dj, with banking it gets a little complicated. See the DCOMP preferred can be used for the banks Tier 1 capital purposes. Subordinated debt can only be used for Tier 2 and I assume (but guessing being I am not a bank expert) Tier 3. So they plug different capital holes (subordinated trust debt was disallowed by regulators as Tier 1 capital after Great Financial Crisis) and are not necessarily interchangeable.

Now for regular C Corps, its different. For companies looking to keep their credit rating higher or avoid a downgrade, they will use preferreds or subordinated debt. My experiences of research shows credit rating agencies treat preferred and subordinated (especially deferrable subordinated debt) as the same. In other words they give them both a 50/50 split equity/debt treatment for credit purposes (senior unsecured for example is treated as 100% debt credit). So many companies now issue that sub debt because it allows them to pocket the tax deduction instead of giving it to the investor in the form of a QDI preferred. And if a going concern blow up hit a company, one would typically find it isnt worth anything more than a preferred. As in ZIPPO.

So yes companies can issue low cap stack debt and get away with it as a preferred and they keep the tax break. Yes baby bonds get a tax deductions. Baby bond is just a generic term though. A BB could be a senior secured all the way down to a junior subordinated note. The BB is just vehicle on who they are targeting to buy the IPO. Which is more retail investor focused.

Wow…. Thanks Grid! I read this several times, refreshed my memory of Tier capital definitions, and think I have absorbed it. I need to get more knowledgeable with investing in debt since that has become a major part of my portfolio. I have generally avoided banks in my portfolio, but do have a couple of preferreds, one from CUBI and one from SNV. I bought SNV- D a little while ago with the thought I would get a few quarters worth of divys and then they would call it. We will see….. Guess I inherited the dislike of banks from my grandfather. He was a successful farmer and also had a sawmill. A non smoker who grew tobacco and then cut timber in the winter and sold the lumber. Always kept his profits in coffee cans buried in the smokehouse and other farm buildings. When the bank holiday came in the Great Depression years and farms were foreclosed on afterwards he would dig up a can and go shopping. Bought hundreds of acres of farmland in the 1930s.

I am not sure if this helps but if you want something that is easily traded without a cusip and actually has some teeth to get paid something in case of liquidation you would want something like EAI.

https://www.quantumonline.com/search.cfm?tickersymbol=EAI&sopt=symbol

All this labeling of stuff as “notes/senior notes/subordinated notes/junior subordinated notes/unsecured notes” and etc.. in most cases means diddly squat in reality when the company is leveraged and has very little in the way of useful/valuable physical assets. The whole bank, mreit, etc.. will simply blow up and there is not enough left over to pay investors of almost every sort.

Now if you are talking about a truly established company. Say Walmart or what have you.. all of these levels truly have meaning when the company most likely owns tons of sellable assets during liquidation. Then you actually have to do the math to see what each level gets in the end. “Most” of the stuff we see and discuss here on this forum recently.. it is almost a pointless exercise due to how they often fail. Which is suddenly and spectacularly.

I am a tourist in this neighborhood, and I do notice a big difference on this visit. A while ago, a new issue would be priced that appeared to be undervalued and it would move up to approximate my expected price. Now, the new issue stays flat and they whack the existing comparable security — i.e. DCOMP.

FYI, one could have bought or sold DCOMG today at $25.10, and that was with strong momentum in DCOM (underwriters probably covering shorts to get the deal done).