Well I hope everyone got their brains rested up so you can navigate what is almost certain to be a wild week–it looks like we should have lots of twitter action ahead as DJT has been active the last few days. In particular in regards to Apple, the EU and Putin. Of course one never knows but it seems that the number of potential twitter targets continues to grow.

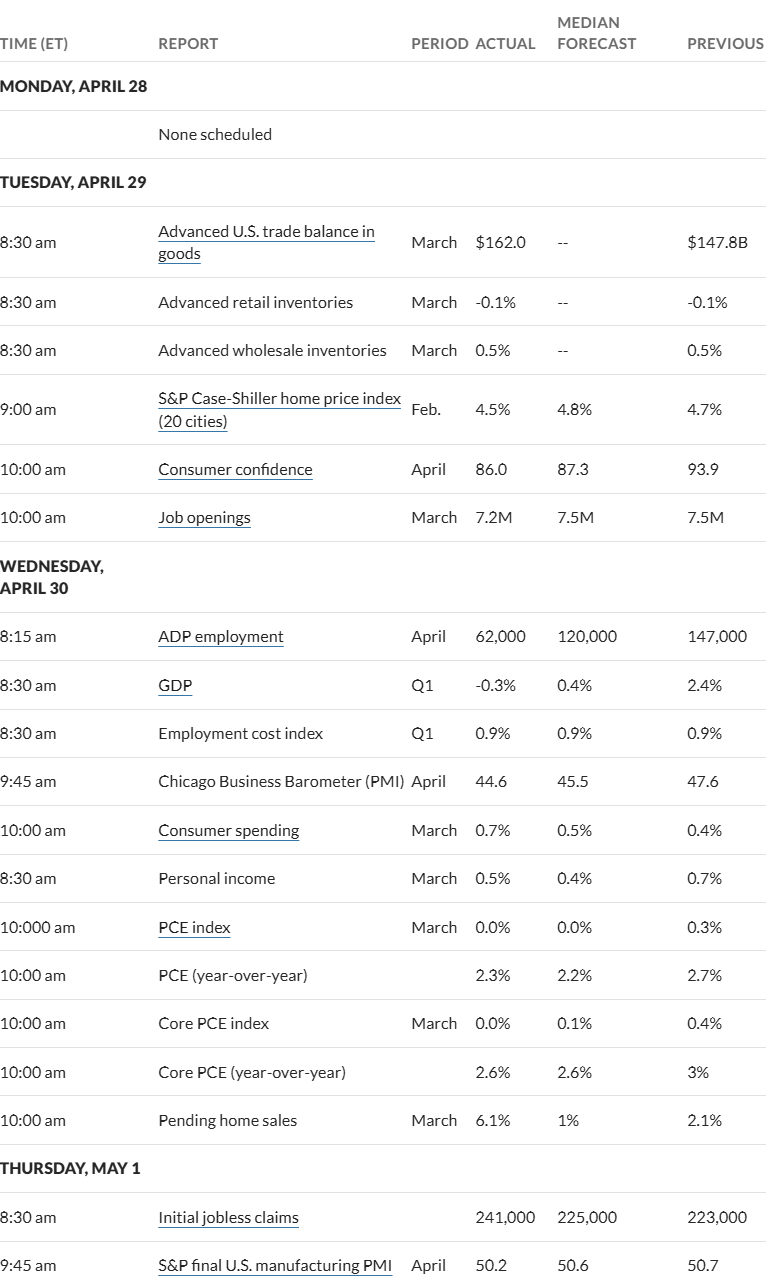

The S&P500 fell by 2.6% last week from the close the previous Friday at least partially on the back of tech stock Apple being battered on Friday based on a DJT twitter attack through the week from the administration threatening high tariffs if iPhone production was moved to the U.S. We all know that there is no way to move that production anytime soon so it is likely that there will be a ‘deal’ cut on a timetable to move it onshore. We didn’t have any particular economic news that was important in a major way so markets are moved on tweets.

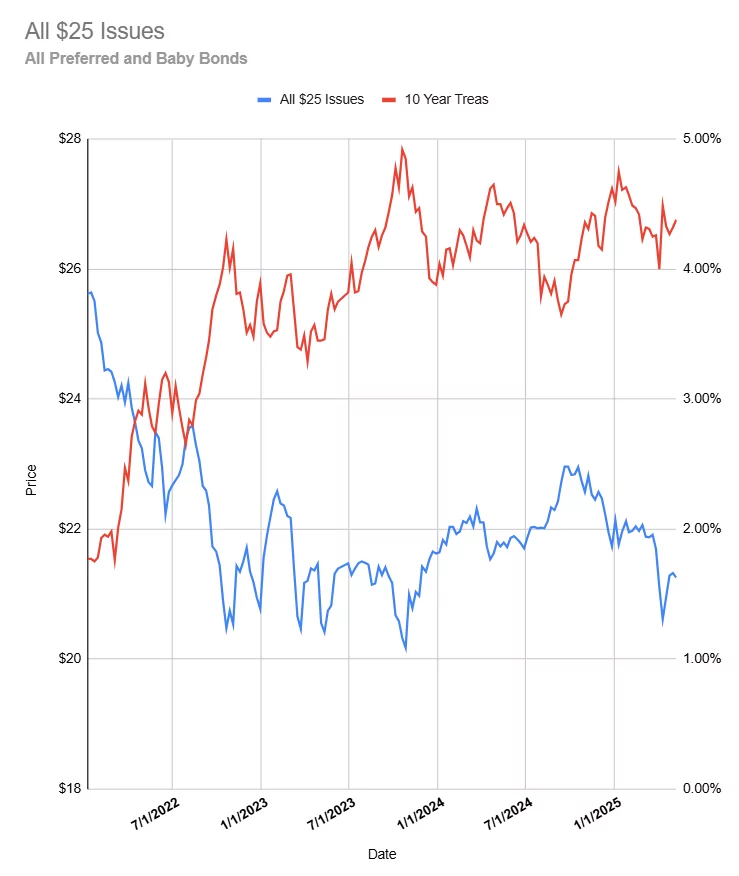

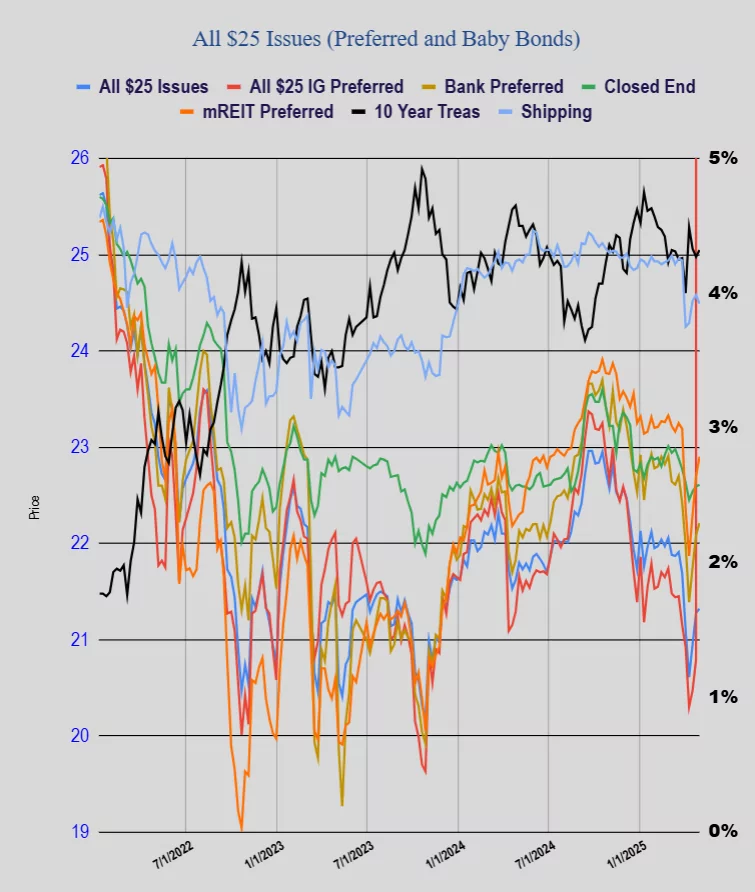

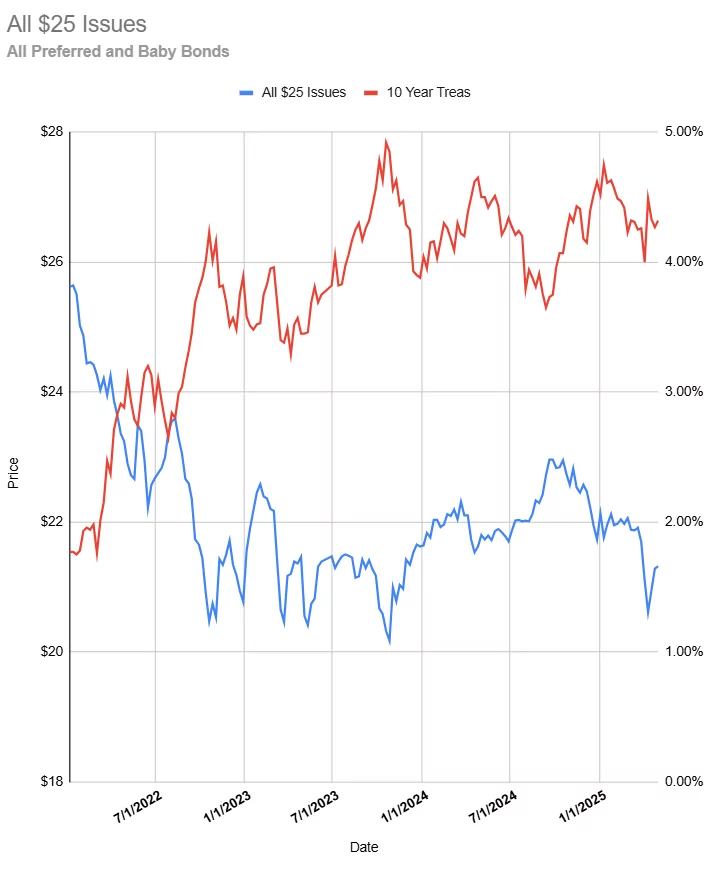

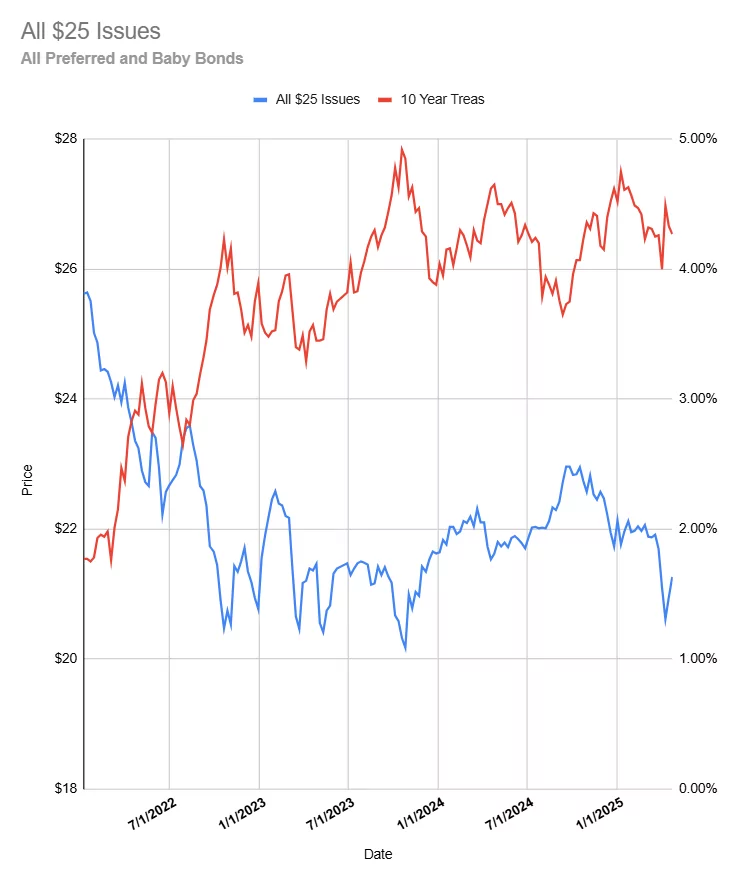

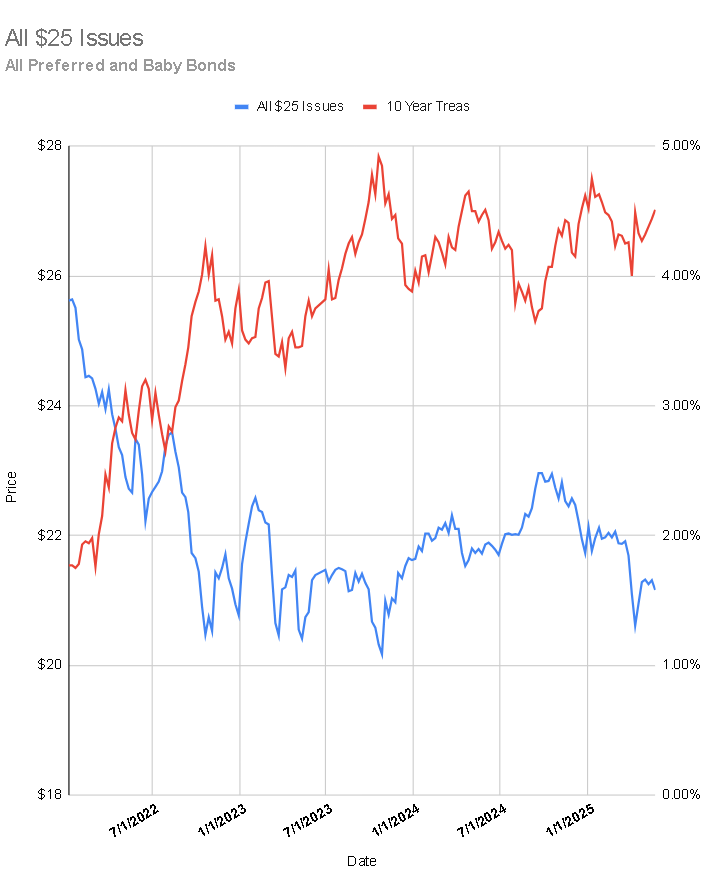

The 10 year treasury closed the week at 4.51% which was up 6-7 basis point from the close the previous Friday. The yield had been as high as 4.63% earlier in the week because of some treasury bond auctions that had more tepid demand, but investors decided that to buy Thursday afternoon and Friday bringing the yield down somewhat.

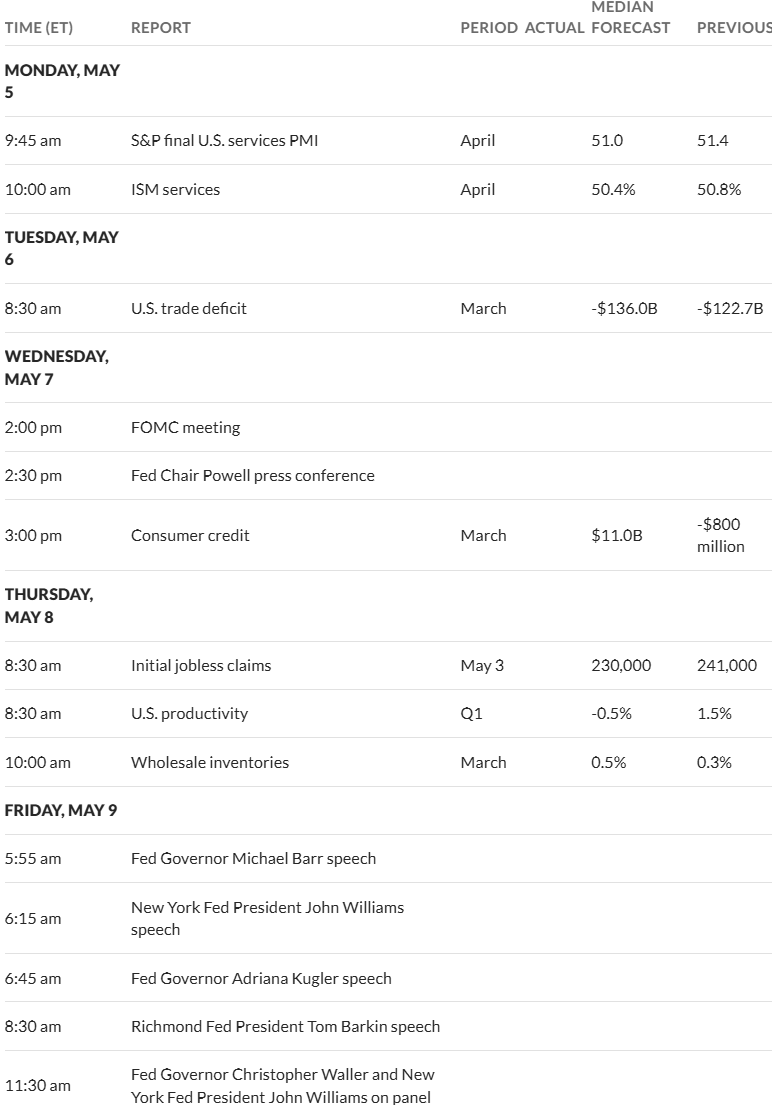

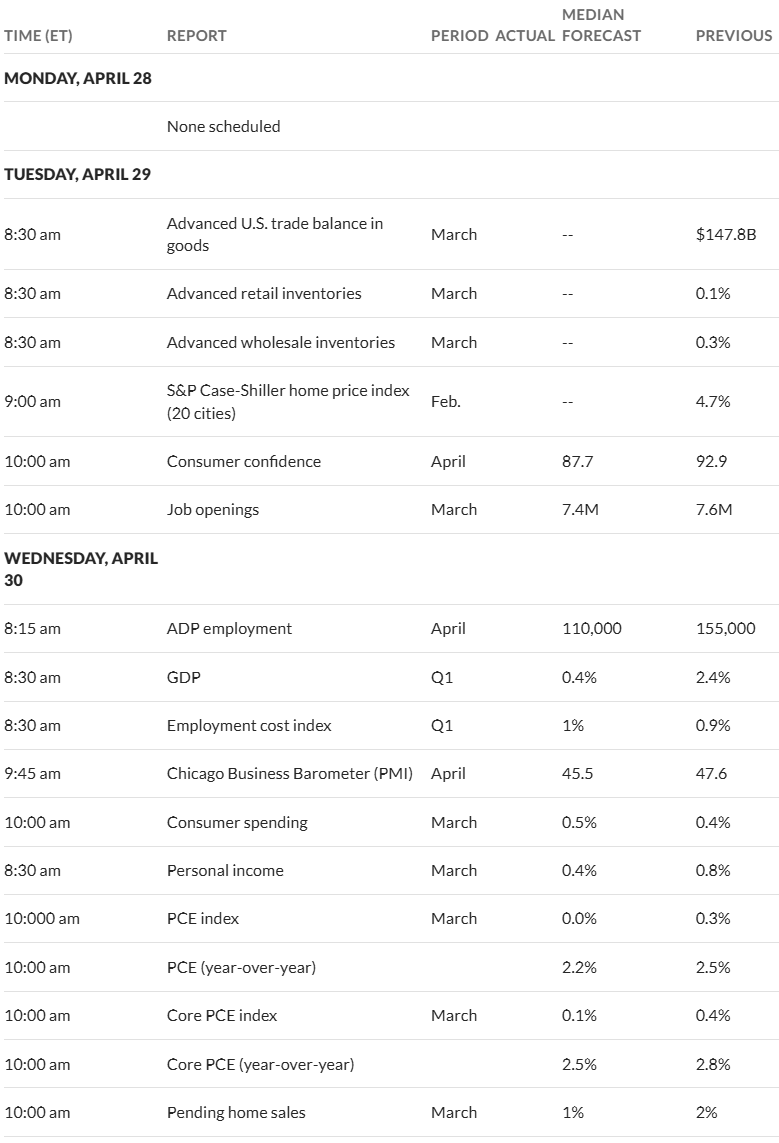

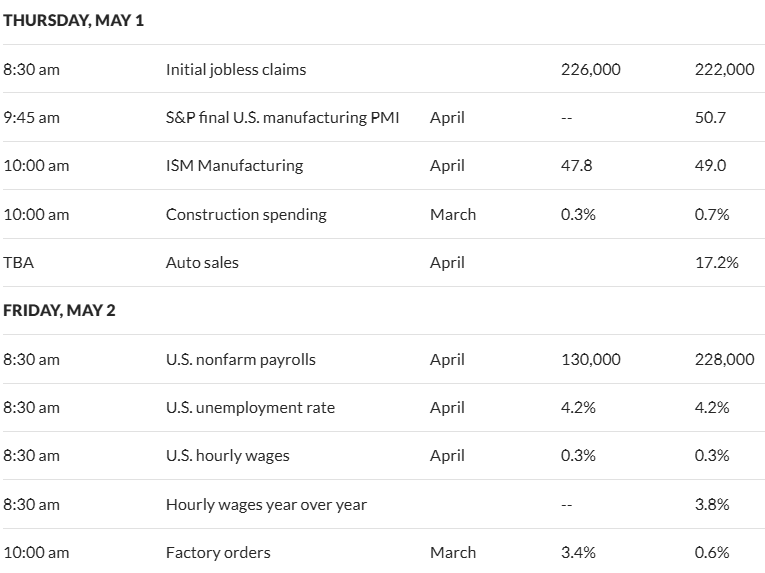

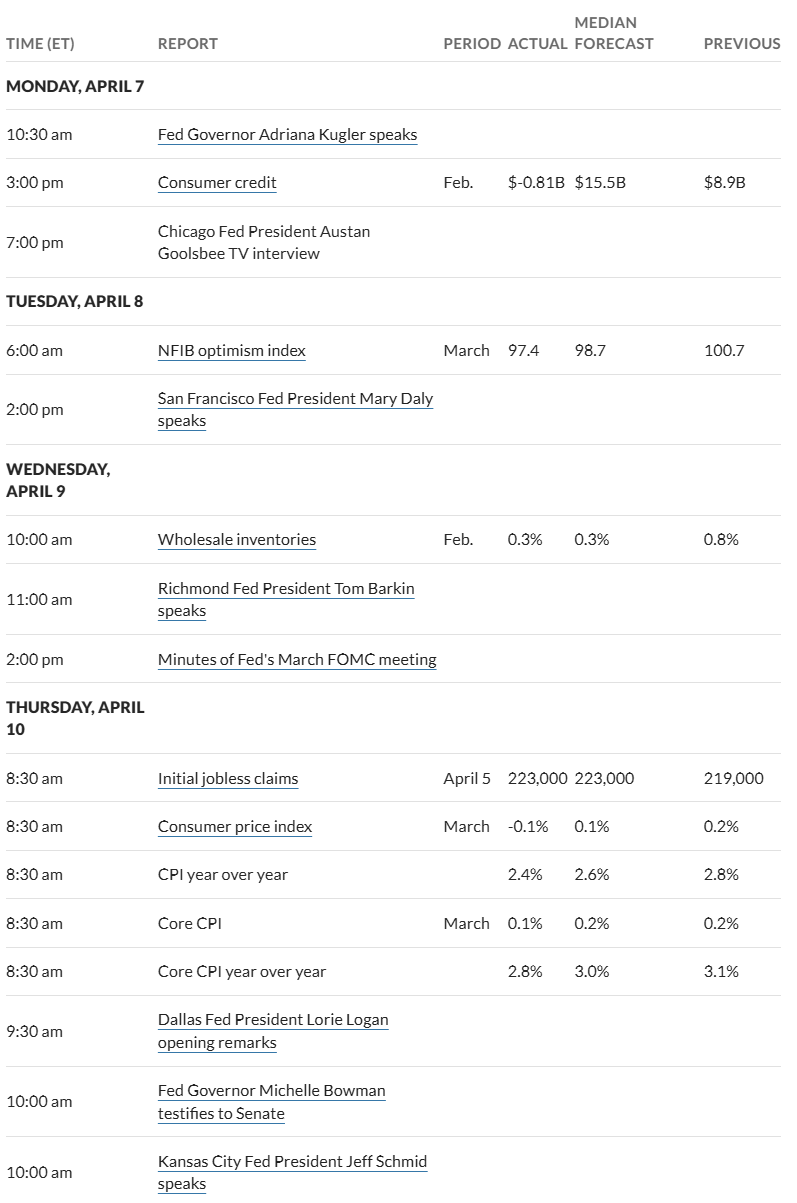

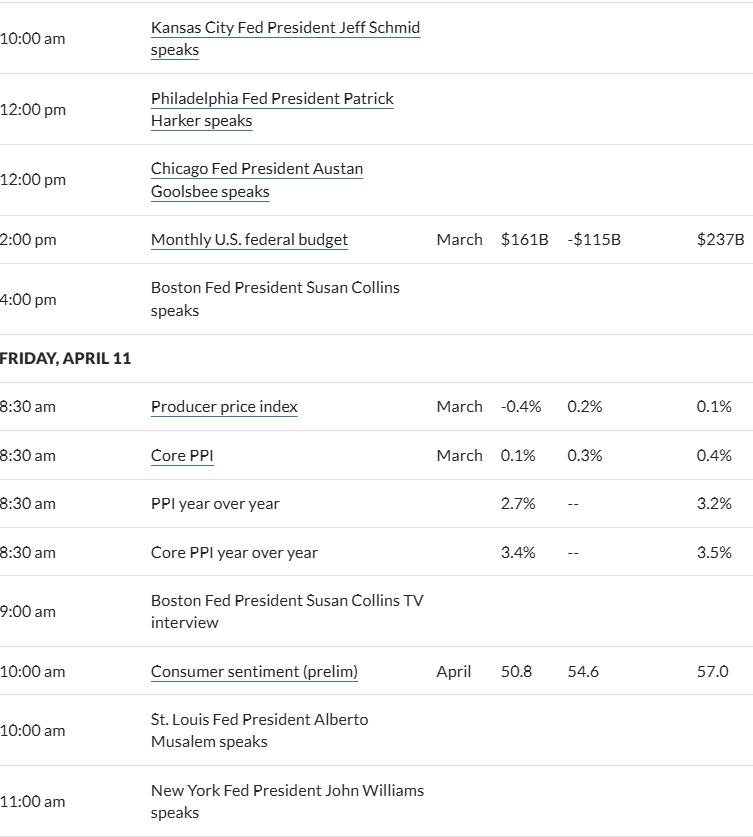

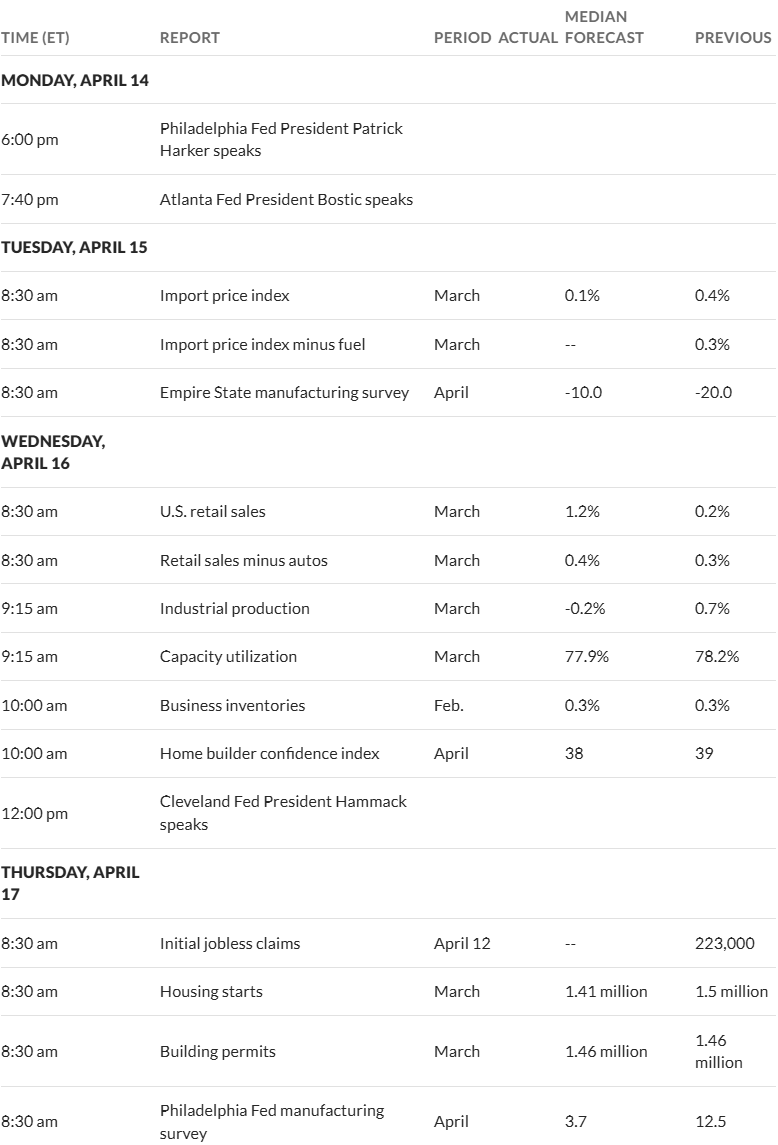

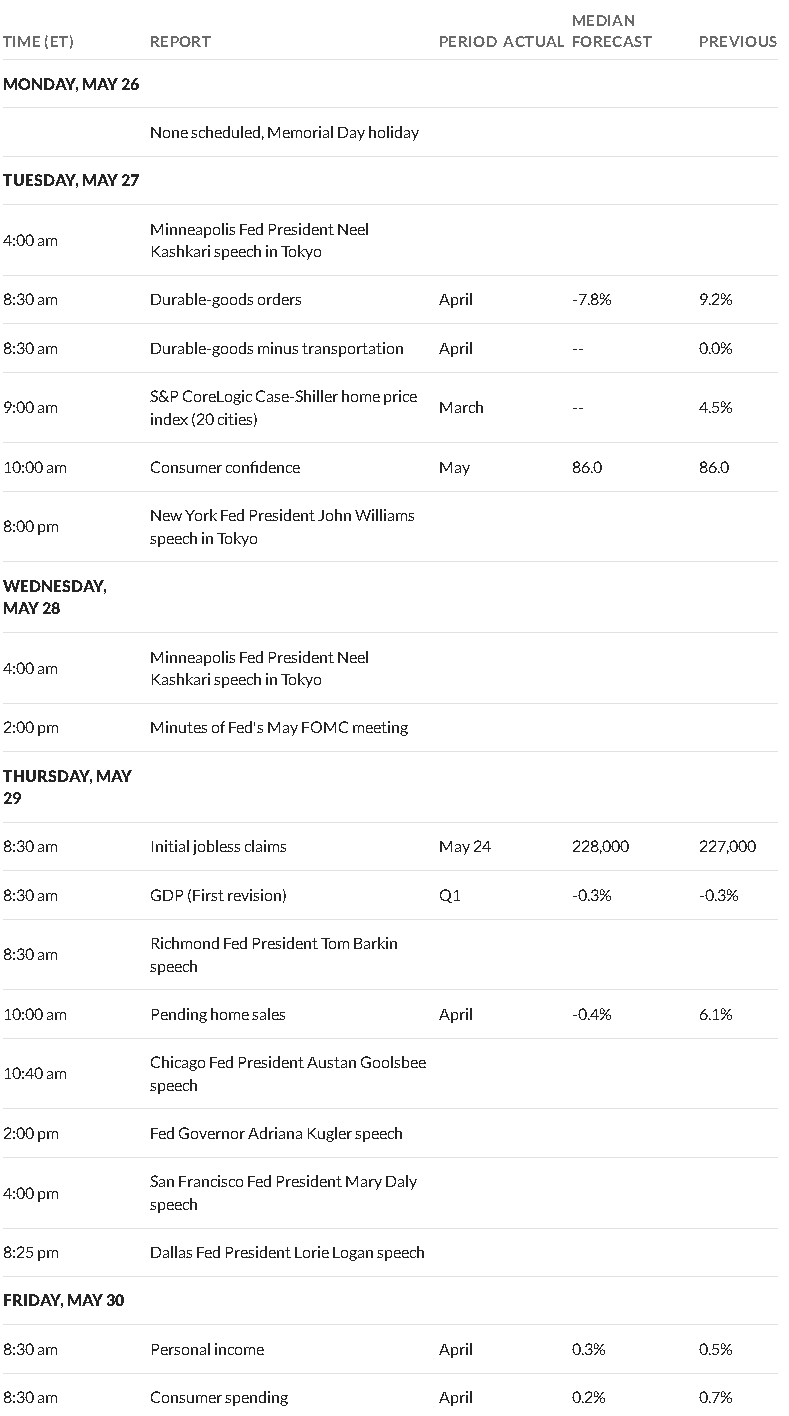

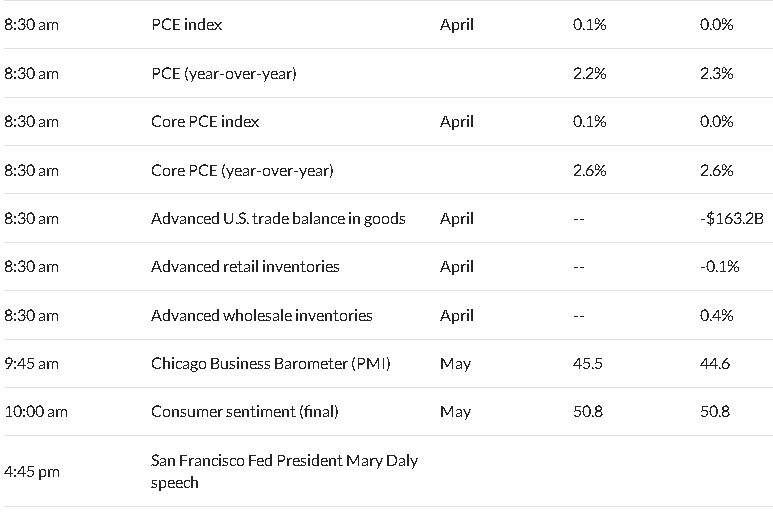

The coming week will bring a few important pieces of economic news with the FOMC minutes being released on Wednesday and then 1st revision of Q1 GDP being released on Thursday–the original number was a minus .3%. We wrap up the week with the PCE (personal consumption expenditures) being released–will it show a jump in inflation or not?

The Fed balance sheet assets fell by $29 billion last week—after a number of weeks in a row where the balance sheet remained fairly flat it was expected we would see a fairly large drop.

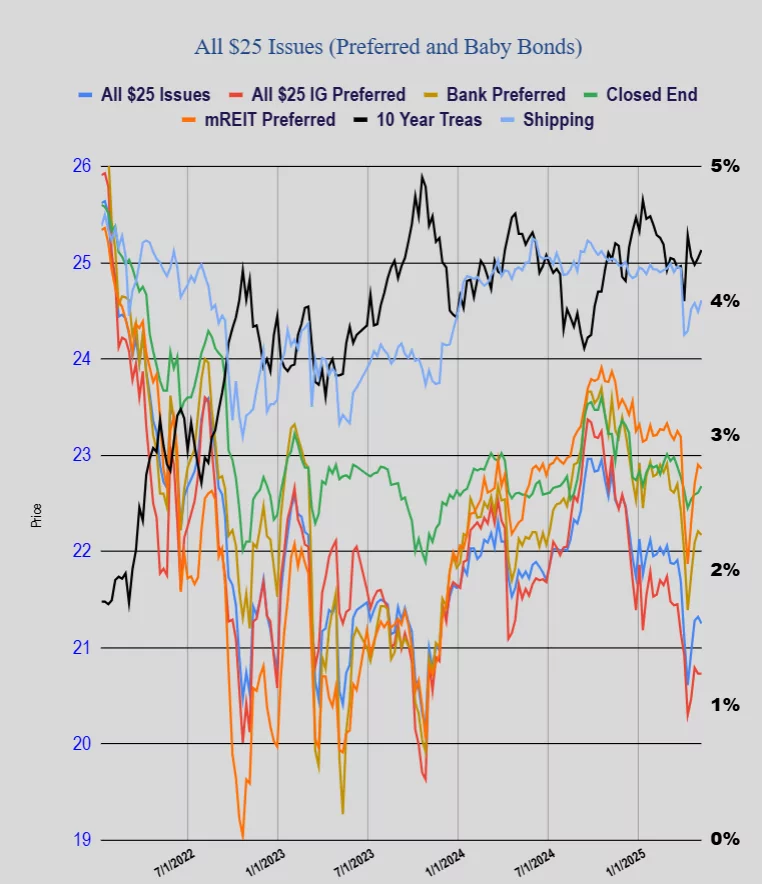

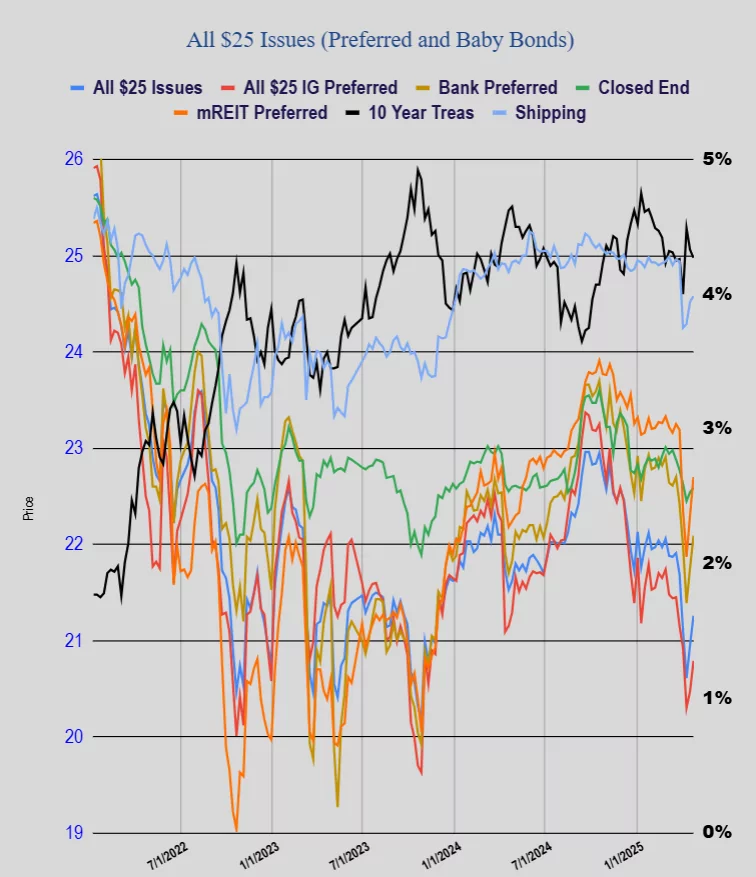

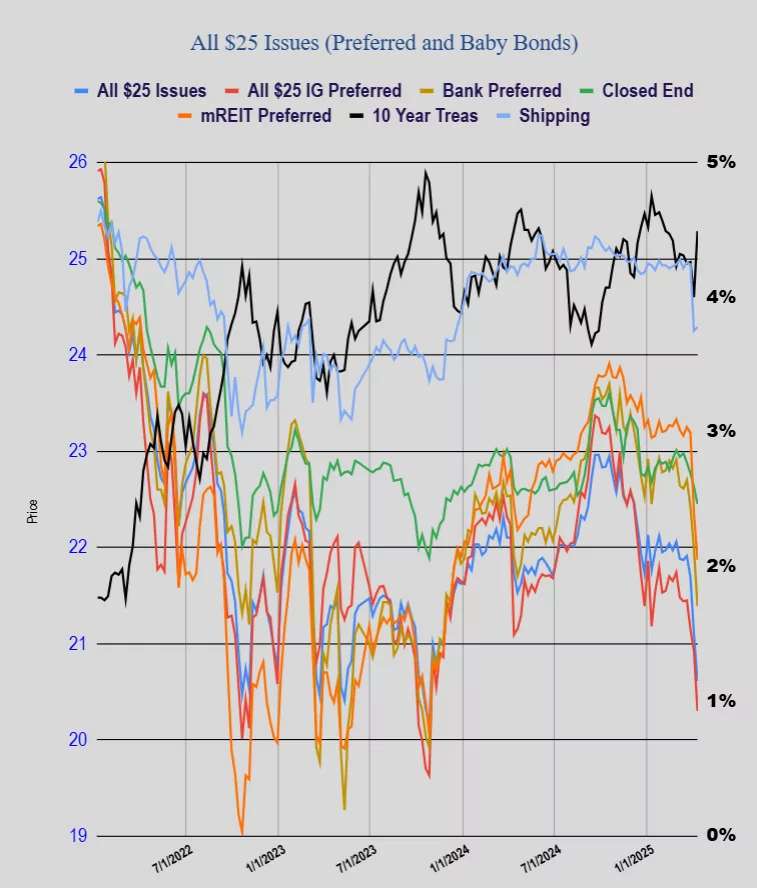

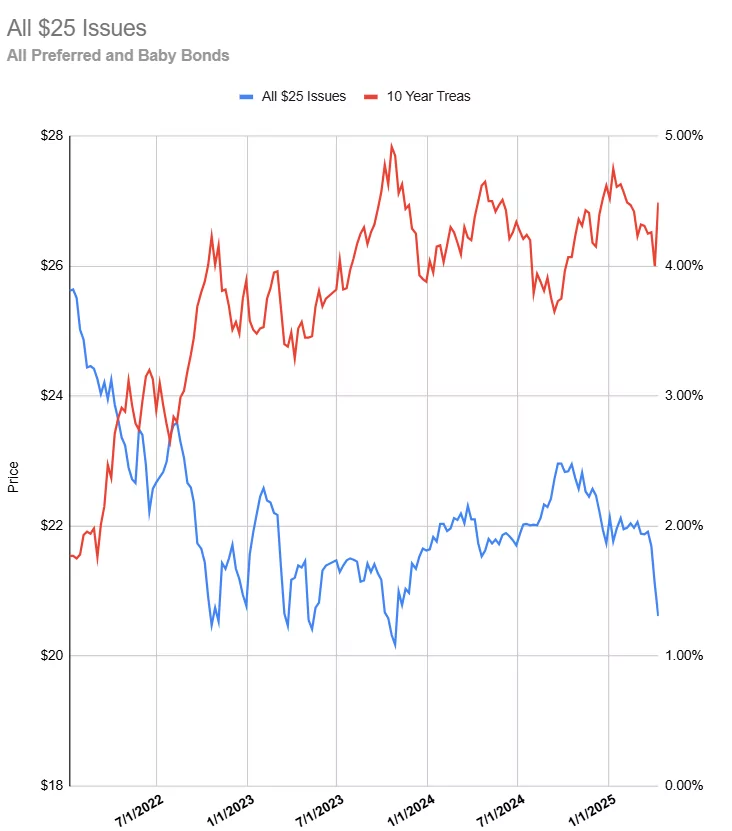

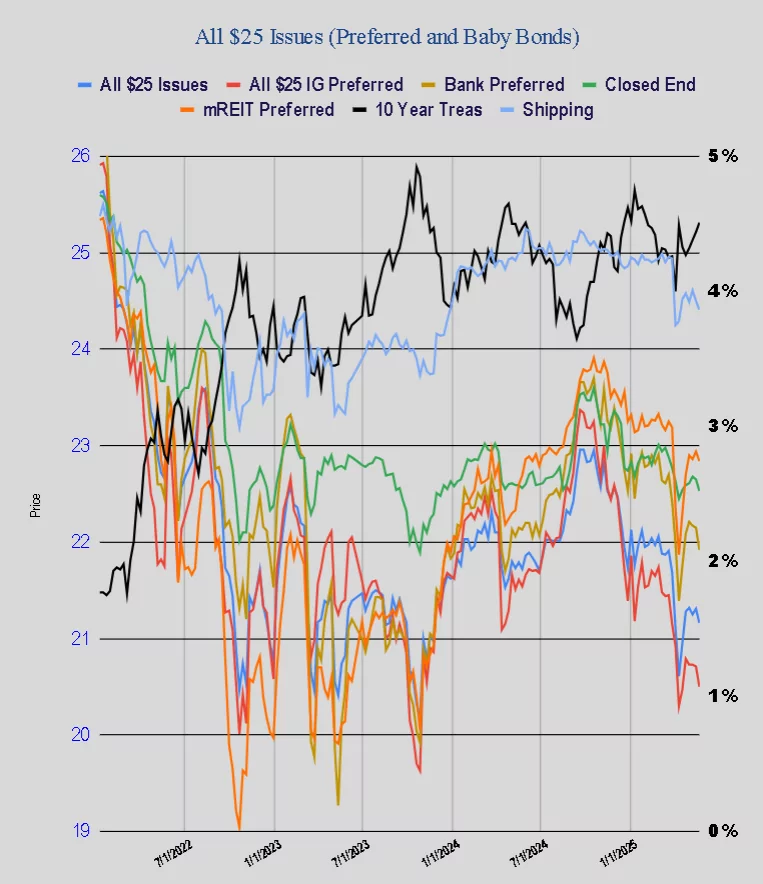

With movements in the 10 year treasury yield last week we got more moves down in the average $25/share preferred and baby bond prices. The average share was off 15 cents with investment grade issues off 21 cents, banking preferreds off 20 cents, CEF preferreds off 12 cents, mREIT issues off 10 cents and shippers off 9 cents. Over the course of the last year the average share price is down 2-3% BUT since September 2024 the average share price is DOWN almost 8%. As one might expect the most damage was down in the high quality issues with investment grade issues down over 12% since September.

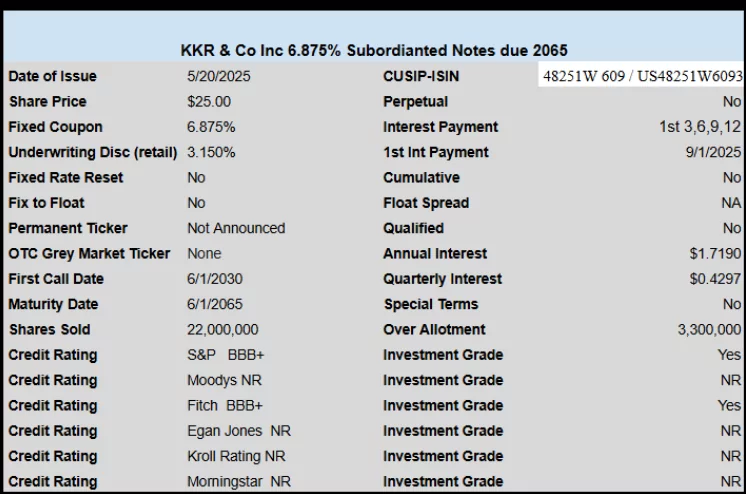

Last week we had just 1 new issue price as asset manager KKR sold a investment grade subordinated note with a coupon of 6.875%.