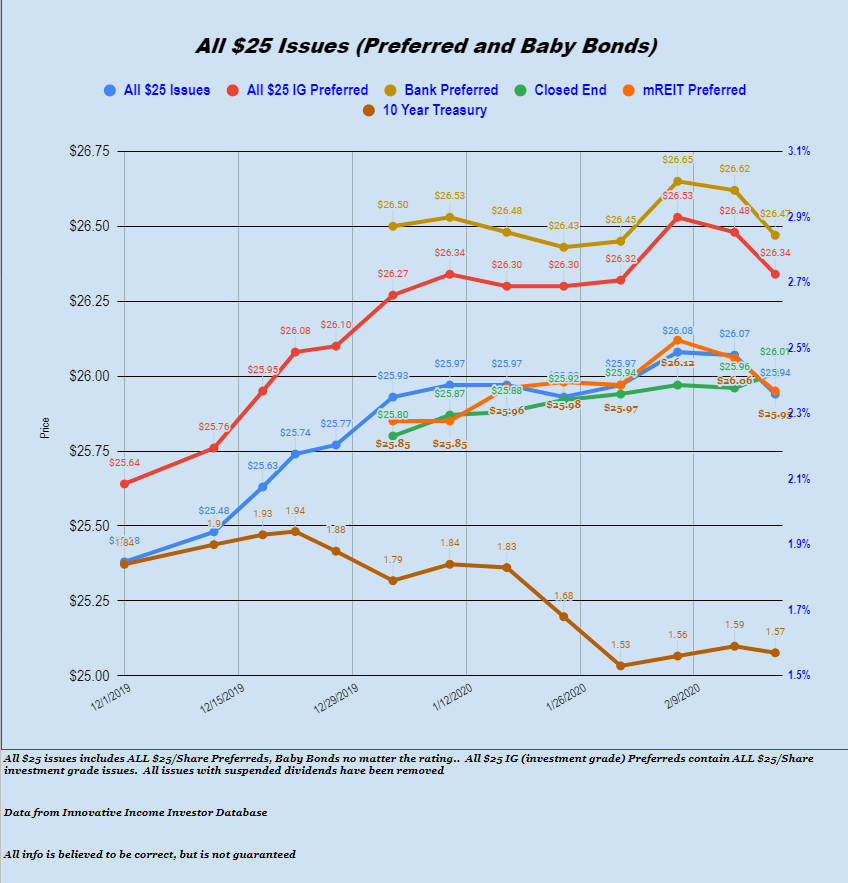

We have discussed on here many times ‘sock drawer’ holdings–those that we really like for the dividend/interest they pay us, but also for the safety they bring along. These many times as what I call ‘base holdings’. I try not to sell them–and many times I don’t pay attention to them daily.

It is obvious to all on this site, that I, along with many others, have been reluctant to jump on the spate of low coupons issues that have been presented to us during the last many months.

This leaves us with excess cash in accounts that is earning maybe a 1.50% money market interest rate–sometimes even less.

Because of this I use some of my excess cash to buy some short term holdings (flipping and dividend capture) with the desire to earn just 1-1 1/2% in a month—I’m not asking for much–just a friggen 25 to 40 cents/share.

NOTE–nothing here should convey the idea that myself and folks on the site are about short term trading–quite the contrary–we love to buy and hold, but we have to have issues that are of the right risk/reward and allow us to sleep at night–the low coupons offered currently just don’t cut it.

Well for the most part this has been like ‘shooting ducks on a pond’-for months and months, although January was much more difficult than December in this regard.

But as some commenters have noted today there are a number of decisions that have to be made–and here are a few examples–some of which I may have outlined on the Flipping and Dividend Capture discussion page.

Triple net lease VEREIT has a 6.70% monthly paying preferred (VER-F) outstanding which has been a great preferred to own. Unfortunately the company has been redeeming shares–in chunks of 4-8 million–as you can see here. Fortunately it is a 43 million share issue so it will take a while to get all the shares redeemed at this rate. During the last partial call in December shares fell to near $25–I owned a small position at that time and added a decent chunk after the fall. Today the issue hit $25.73–I am out after collecting 2 monthly dividends and a capital gain.

So the decision was–let it ride and see if it goes higher–or will they call some more shortly thereby driving the price down? I decided that it best to exit with the gains and wait for the next partial call and see what develops.

I bought a full position in the TravelCenters 8% baby bonds (TANNL) on 1/21/2020 for $25.43 looking for shares to rise into the ex-dividend on 2/13. I have a GTC sell in at $25.90 right now–today it closed at $25.79. I have achieved my initial goal with a near 1 1/2% gain and obviously could sell right now–but I believe that there is just a bit more upside in the issue prior to the ex date next week. If my GTC executes fine–otherwise I will have to decide whether to take my gains or hold through the ex date for the 50 cent capture. The issue has been callable since 2017–but I believe it has no risk of a call.

Lastly for now–I had bought the B Riley 6.75% baby bond (RILYO) at $25.71 on 1/13 hoping for a quick and profitable dividend capture. It went ex-dividend the next day 1/14 for 42 cents.–poor idea. Typically I want to buy on a dividend capture 2-3 weeks before the ex date, but I made a bad decision to buy the day before–just antsy with too much cash on hand. Anyway I continue to hold the issue and finally today see about a 20 cent net gain–all in all not really that bad, but timing was really bad and this isn’t really an issue I want to hold long term. So my decision is to exit immediately for just under a 1% gain, hold a bit longer and see if I can squeeze out another 5-10 cents–or just be patient and hold closer to the next ex date in April before selling. As alway I want to have a rib eye steak gain–hamburger steak isn’t that great.