Are you ready for another week with big moves in equity markets? I am pretty darned certain we are going to see some big moves, which make me nervous, but there is nothing I can do about it—not going to sell, but probably will be doing a little buying—in fact I have a target in mind for today. Of course I will post anything I do.

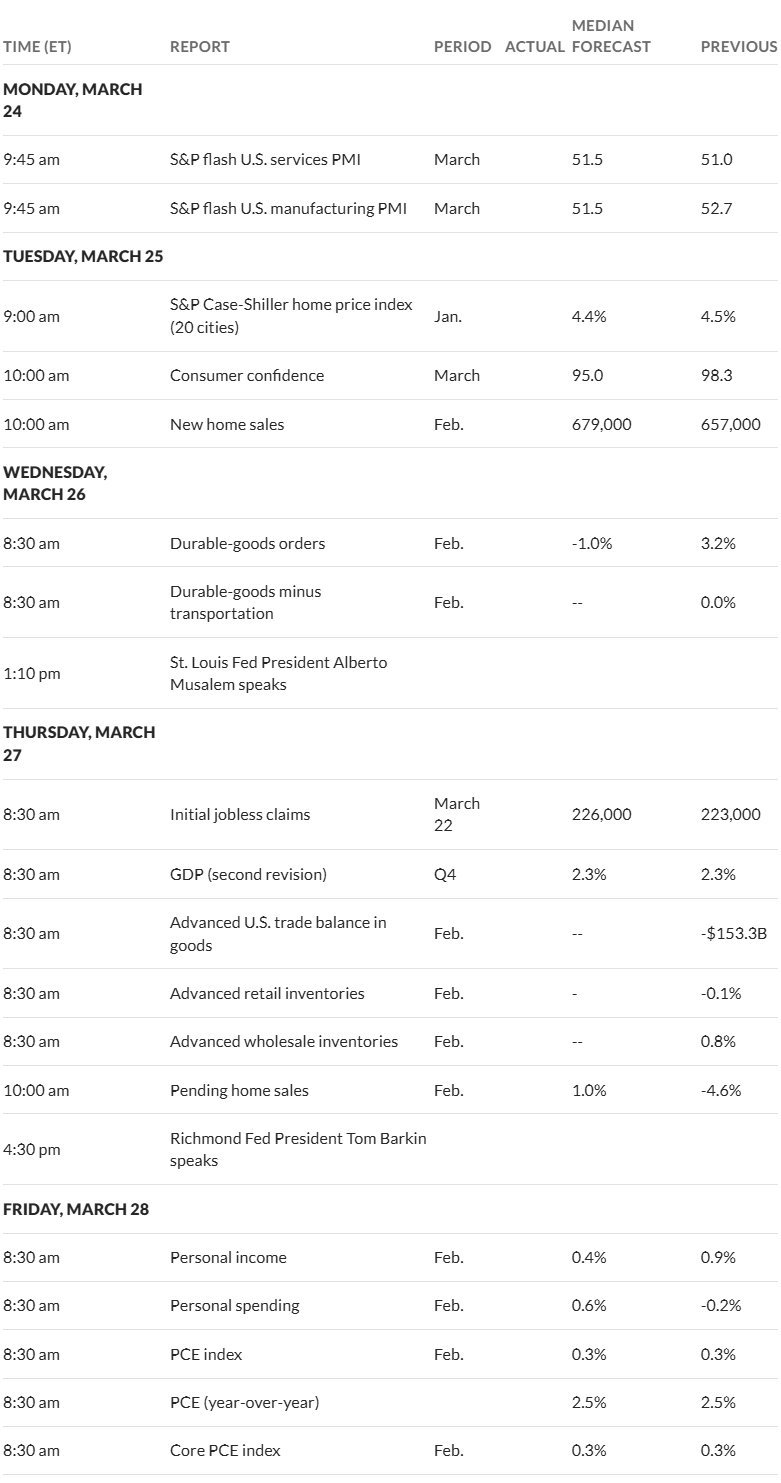

Last week the S&P500 moved higher by a measly 1/2% (or thereabouts) and the range it traveled in was ‘relatively’ mild compared to the recent past. The range was only in the neighborhood of 1%. This week we have the personal consumption expenditures (PCE) number being released on Friday which we all know will be important, but we also have durable goods and consumer confidence numbers being released and markets will decide if they are important or not.

The 10 year Treasury wanted to push lower all week long and hit a low of 4.17% on Thursday before bouncing to close the week at 4.25% which was 5 basis points lower than the 4.3% close the previous week. Housing release numbers last week were mainly strong–building permits and housing starts BUT at the same time builder confidence fell to low levels. You have to ask if housing permits and starts were so strong why are the builders feeling poorly? Existing house sales were quite a bit above expectations–contrasting with recent consumer confidence numbers which have been pretty weak. Once again these contrasting numbers lead me to believe that folks are somewhat confused as to what direction this economy is taking.

Of course we had the FOMC decision to leave interest rates unchanged–and chair Powells presser left me with the impression he is a bit confused as well–what will tariffs do to inflation etc? There are no firm answers and more data will be needed to have a firm conviction.

Maybe the largest economic announcement last week was that quantitative tightening was getting a little looser as the FOMC announced they were cutting the run-off to around $40 billion/month from $60 billion. I had suggested this could happen last Monday on the ‘weekly kickoff’–I was thinking maybe they would cut the runoff in 1/2, but 1/3 works. We’ll see if it helps move interest rates a bit lower.

The Fed balance sheet fell by just $4 billion last week–we’ll see if this starts to show the average monthly at $40 billion right away–no doubt in my mind this will happen instantly. If this helps rates down 5-10 basis points it will keep a little of the political pressure off the Fed – FOR NOW.

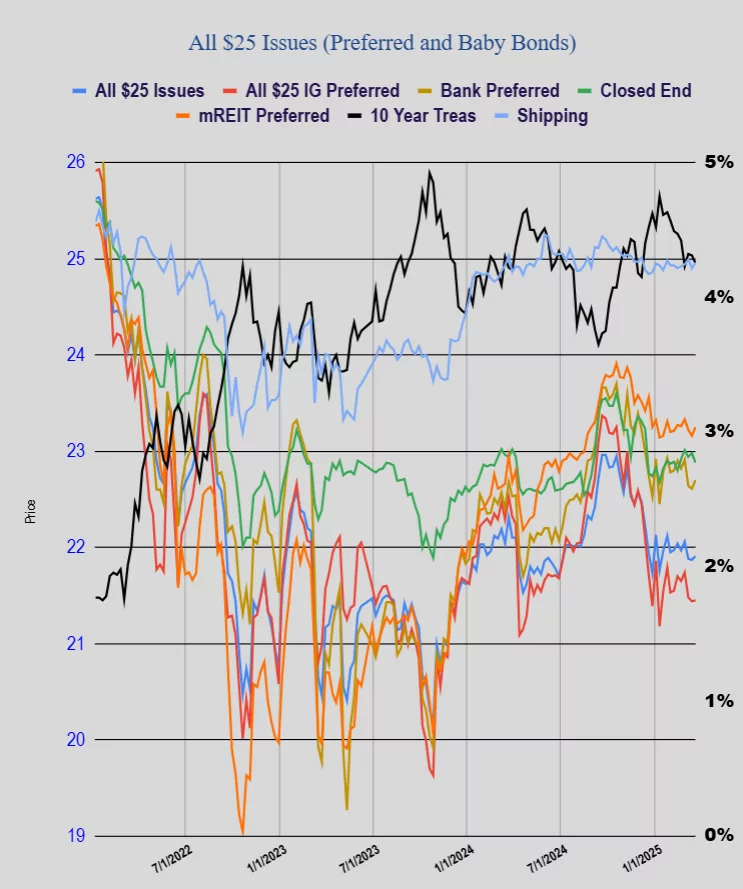

Last week was pretty quiet in preferred stocks and baby bonds as the average $25 share price rose by 4 cents. Investment grade issues rose a penny, banking issues rose 7 cents, CEF preferreds fell a dime with mREITs off a nickel. Shippers popped higher by 6 cents.