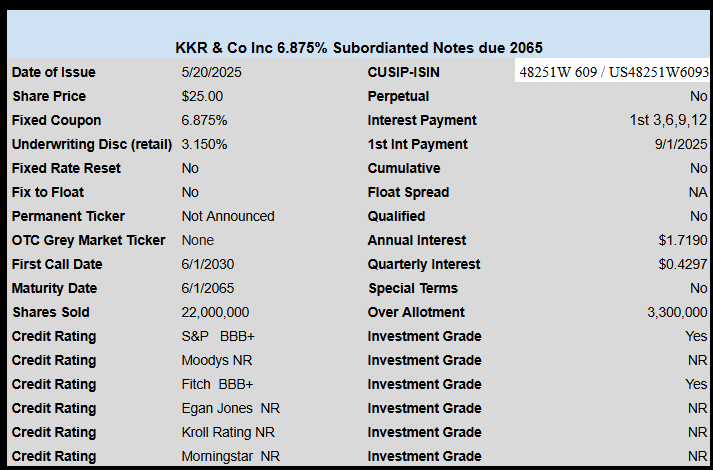

Asset manager KKR & Co has priced their previously announced baby bonds.

The issue prices at 6.875% and have a maturity date of 6/1/2065.

This is an investment grade issue from S&P and Fitch, although the company has the right to defer interest payments for 5 consecutive years without a default being declared.

Closed end fund Carlyle Credit Income Fund (CCIF), an owner of CLOs (primarily the equity tranche has a 8.75% term preferred (CCIA) outstanding which has a maturity of 10/31/2028–BUT an optional 1st call date starting 10/31/2025.

This is a monthly payer at 18 cents month on the last day of the month and at this moment is trading at $25.53.

We don’t know what interest rates will do between now and October, but if they fall there is a real chance that the CCIA issue will be redeemed on 10/31/2025—or at a minimum fall back to near $25 simply on the potential for a call. In my opinion if shares rise into the high $25’s one should consider selling.

This is an issue that I bought a number of times in 2024, but exited (at $26.67) on the giant silly spike back January. I will potentially re-enter if shares fall down to the $25.20 area (I have a few token shares in the account yet).

Below are press releases from companies with preferred stock and baby bonds outstanding. Additionally, news of a more macro economic importance may be posted.

Earnings season is over for now and not much news is being posted by company’s that are of interest so for the next 6-8 weeks postings will be relatively lite.

Things are relatively quiet today with no economic news releases. I guess about the only ‘news’ that is out there is news on whether the house and senate can pass a budget bill and what will it contain. I guarantee that no matter what they pass it will have too much spending in it to suit me. I have little faith in the DC folks and it doesn’t matter which party they belong to.

I am really curious about what prices are doing out there in the retail space. I hardly ever ‘shop’–my wife does 95% of our shopping–the other 5% I do on Amazon. The few items I buy haven’t changed in price yet and I guarantee most of the stuff is manufactured in China. Next week we get the release of the personal consumption expenditures (PCE) report–but it is for April so not as recent as what I would like to see.

So for now I am just sitting back and watching the politics play out—I am waiting for someone brave enough to tackle the ever growing deficit spending–I may be waiting a long time.