While today is pretty darned quiet–equities are up the tiniest of amounts right now (1/5%) and interest rates are up 2 basis points to 3.98% you can be certain starting at 9 a.m. (central tomorrow) that we will see much more action and movement. There is no way that Jay Powell can testify to congress for 2 days without some fireworks going off. Honestly if markets were flat for Tuesday and Wednesday I would be perfectly happy.

Overall preferreds and baby bonds are a tiny bit green–just like the equity markets–the tiniest of green. I think that Powell will have to put on a hawkish tone for congress–so I think that interest rates will head back over 4% tomorrow, but if you made any bets on what I ‘feel’ you would be a loser–typically prices move in the opposite direction to what I ‘feel’.

We had the new Jackson Financial (JXN) issue announced this morning and as usual we have some good comments on the issue–and thought on fixed-rate resets in the comments–it is great to see since we have so many really smart folks here–the comments make one think a bit deeper about the new issues. Thanks to all that comment and help make me and all readers smarter. Well let’s see where it prices–earlybird ponders 8.125% or so on the initial rate and 1 notch below investment grade.

Annuity company Jackson Financial (JXN) has announced a new fixed-rate rest preferred. A fixed-rate reset preferred has a fixed rate for 5 years and then ‘resets’ every 5 years at the 5 year treasury plus a fixed spread (yet to be announced).

JXN is new to the retail market and we will have to do some due diligence on them.

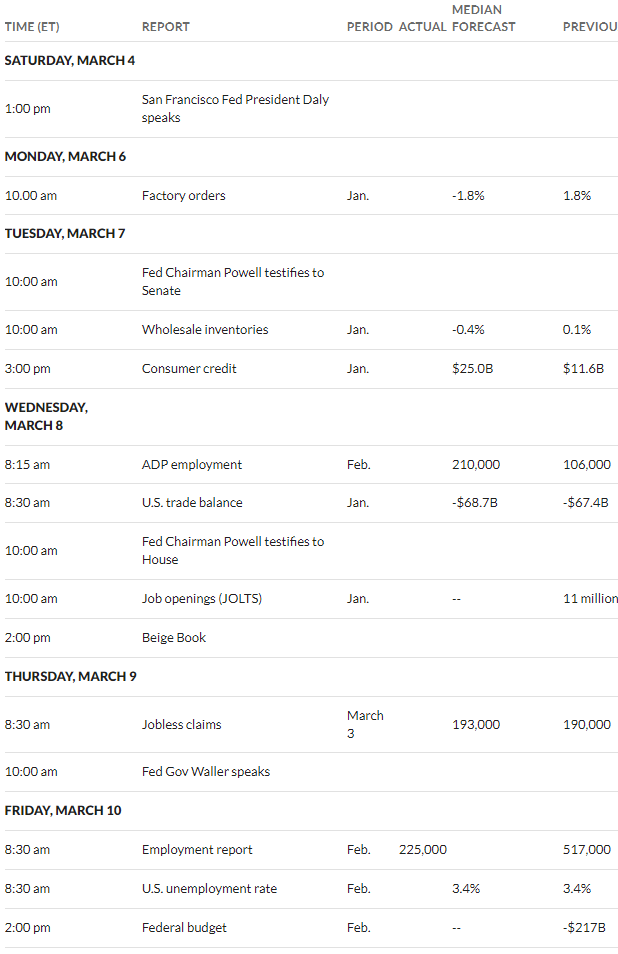

Well here we go into what is most likely going to be a pretty wild week. We have Jay Powell testifying to both of the senate and the house–so you know there will be fireworks of some sort.

Last week the S&P500 rose by 1.9% and closed right near the high for the week. Although most economic data remains hotter than forecast equities just keep staying up–for now.

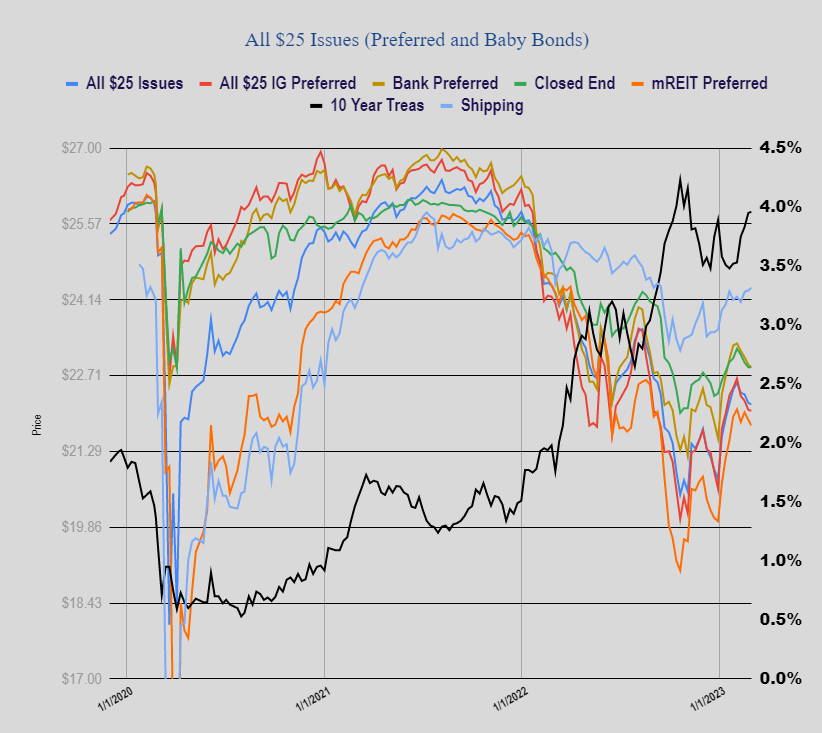

The 10 year treasury backed off from the 4.09% level of Thursday (the high of that day) to close at 3.96% on Friday. No reason to think this level will hold–but if we all knew where rates were going we’d all be billionaires.

As mentioned above the Fed Chair will testify to congress on Tuesday and Wednesday. Then we have the JOLTS (job openings and labor turnover) report on Wednesday. We have ADP employment numbers Wednesday–honestly a worthless report that is mainly ignored. Then the big report for the week–the ‘official’ employment report on Friday. The forecast is for 225,000 new jobs with the unemployment rate holding at the 3.4%. I have an expectation that the 517,000 new jobs supposedly created in January will be revised–lower?

Last week the average $25/share preferred or baby bonds barely moved–lower by 3 cents. Investment grade issues were off 2 cents, banking issues 5 cents lower, mREIT preferreds off 11 cents, CEF preferreds were dead flat and shippers gained a nickel. It really can’t be any quieter than that!!

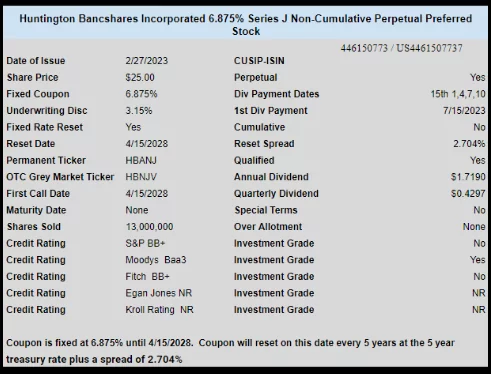

Last week we had one new income issue priced–a split investment grade issue from Huntington Bancorp. The issue was trading on the OTC and closed at $25 on Friday.

Any time I post ‘quiet day’ you can be certain it won’t be that quiet.

Today equities are up over 1% and the yield on the 10 year treasury is back down just under 4%. Why?? Who really knows. I see that the ‘services’ indexes were adjusted higher this morning–not showing moderation in this sector.

The Federal Reserve posted a monetary report to congress stressing the need for more rate hikes–Fed chair Powell will testify to congress next week on this report and of course take questions.

This morning I went ahead and locked down CD’s for $10,000 @ 5.15%–seems reasonable for a year. Plenty of cash in my accounts and so maybe out of boredom I bought these–but we will get better rates ahead–I think.