I know it is really, really tough–I want to blast bunches of the politicians–from both sides of the aisle, BUT we all know where these ‘conversations’ end up taking us.

I have removed a few comments this week–and pondered removing a few others (and may yet)–but my preference is to not ‘patrol’ politics. We have such a great group of people here with lots to contribute without politics.

As noted by 2whiteroses in the Reader Alert comments RILY has dropped 10% today on a short seller report.

I had noted many, many times that RILY held portfolios of real junk–and of course recently we have seen some of their investments go bad (cryto miners).

I invited folks to do a forensic dive into RILY way back in 2019 of course it took years to play out and one could have doubled or tripled there money if they were invested in RILY in the ensuing years–timing is everything. When markets are euphoric no one cares.

Well we had Fed Chair Powell in a Q&A at the Economic Club of Washington yesterday and I thought his answers were very balanced–some leaning dovish and some leaning hawkish–in the end my perception was that there was nothing new. This was one of the few times I actually watched the Q&A–normally I don’t bother, but I wanted ‘my’ take on what was said. This is one of those times that everyone has there own take on what was said–no one really agrees with what was said-some say dovish–some say hawkish–I say balanced.

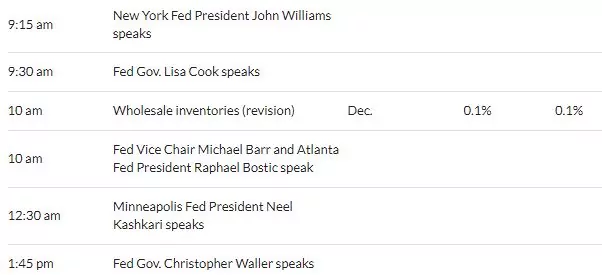

Today we have a bunch of federal reserve yakkers—5 of them on the schedule. I think (but no one knows) that after Chair Powell yesterday these should not move markets, but we all know that any one of them is capable of tossing a grenade—I hope at the end of the day we hear nothing of their speeches–who really needs their baloney.

Equity markets are looking a little soft–off about 1/3% on the S&P500. Interest rates are off maybe a basis point at 3.64%–just maybe a quiet day in interest rates.

Yesterday I did nothing. Personal accounts were basically flat on the day–as I mentioned recently I think we will need to depend on dividends and interest as we look ahead–the giant capital gains are behind us. Now we need to try to hold the January gains and depend on the interest and dividend payments–last time I calculated my yield on cost it was just over 7%–now probably less as I trimmed various gainers.

Did you notice the Prudential Financial (PRU) earnings yesterday–a loss of over a billion dollars for 2022. Assets under management fell $600 billion to $1.54 trillion. Like almost all insurance company earnings they took losses on investments over the last year as stocks and bonds tumbled. I suspect they will have some hefty gains in the current quarter as they benefit, as all of us have, from rising equity markets and lower interest rates. There earnings release is here.