Giant property and casualty insurer Allstate (ALL) has announced a new issue of preferred stock.

The issue will be a fixed rate issue and will join a number of issues already outstanding which can be seen here.

Thanks to EarlyBird for the heads up.

The issue is expected to be rated BBB/Baa2–investment grade. Coupon should be between 7.375-7.625%–pretty tasty. The issue will be non cumulative, but qualified.

Last week the S&P 500 barely moved closing the week at 4124 which was off just 12 points from the close the previous week–.2% loss on the week. The range for the week was incredibly tight as well at 4098 to 4154. The closer we get to June 1 the more likely this market takes a tumble (debt ceiling).

Interest rates closed at 3.46% (the 10 year treasury)–which was about 2 basis points higher than the close the previous Friday. The range of trading was a bit wider at 3.34% to 3.53%.

The Fed balance sheet fell by $60 billion last week as maturity runoffs and bank crisis funding repayments are driving the balance sheet back toward the early March level.

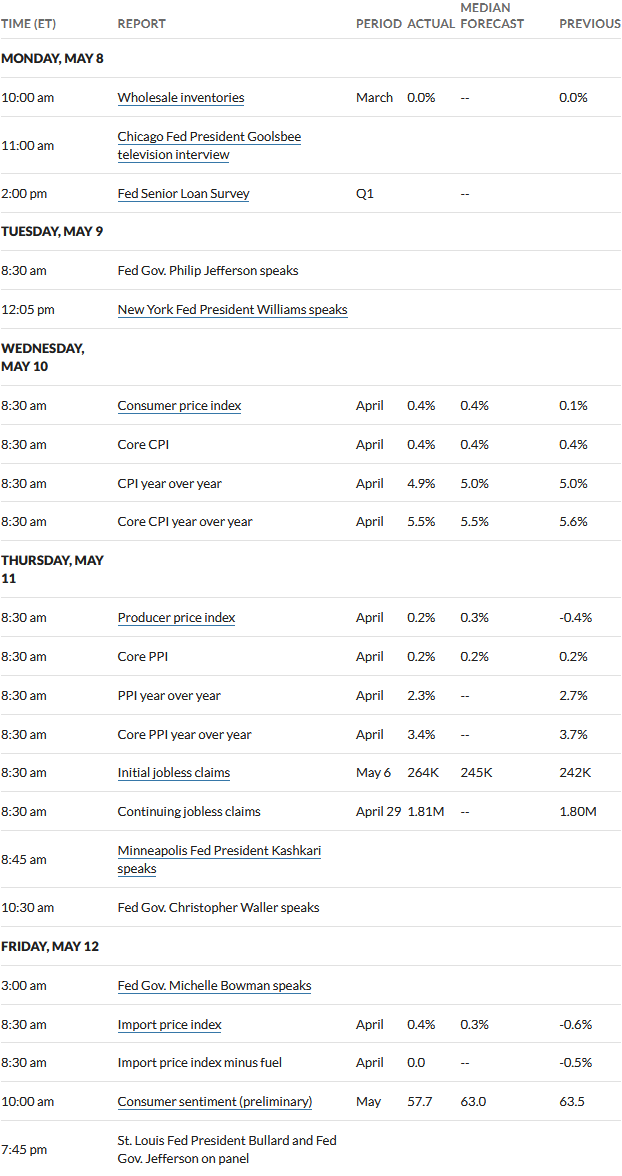

Last week we had the consumer price index (CPI) and the producer price index (PPI) released with both at or a little below forecast. This means a couple check marks in the ‘pause’ camp for a potential Fed Funds rate hike in June. Plenty of data remains to be seen in the next 3 weeks or so.

This week we do not have much in the way of major economic news – lots of secondary in importance items and lots of Fed yakkers so I suspect we may look back on this week and say it was a tight trading range once again.

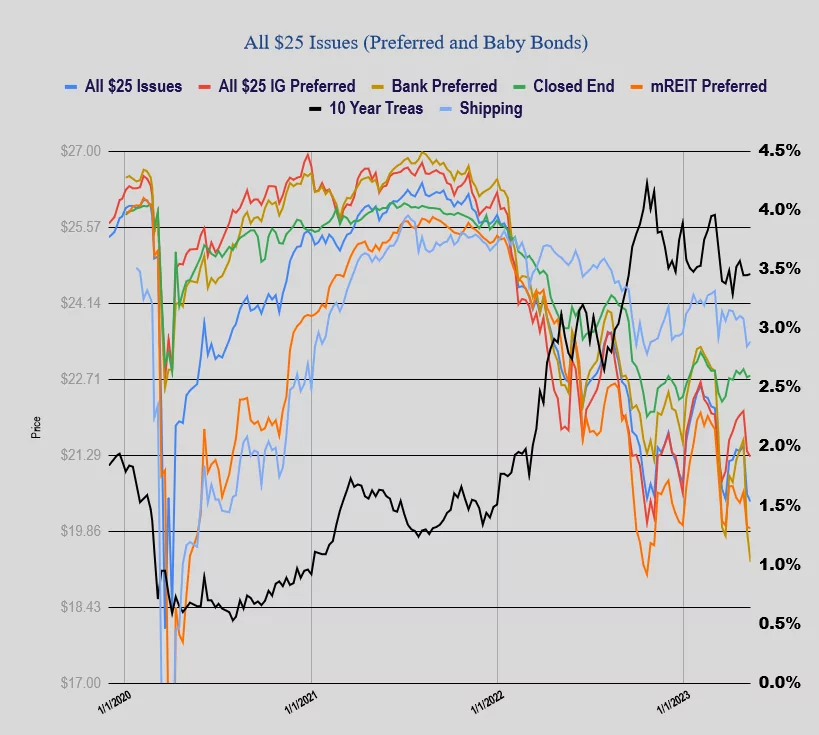

Last week the average $25/share preferred and baby bond stabilized (kind of) from the previous weeks drubbing – average share off 14 cents, investment grade off 11 cents, banks off 59 cents, mREITs off 3 cents and shippers up 9 cents.

As mentioned by a number of people today Wells Fargo has issued their information as to the transition from LIBOR (which is going away in June).

Like many issuers WFC has a number of outstanding fixed-to-floating rate preferreds so a clarification was needed as to what they would transition to when LIBOR (they were issued with 3 month LIBOR floating rates) goes away on 6/30/2023.

WFC WILL NOT use SOFR, but will use the the original fixed rate, plus the designated ‘spread’ from the prospectus. This method will result in sky high coupons, so one should expect these issues will be redeemed when 1st redeemable.

After a few days of respite we saw a rough day for banking preferreds – mostly red, but the red wasn’t as deep as we have seen in the past.

It is obviously too early to go ‘all in’ with the banking preferreds–but there should be no doubt that there is opportunity coming–unfortunately we don’t know when that opportunity will finally present itself.

I continue to watch those bankers I own for any new news–i.e. uninsured deposit level etc. so I don’t have to start my hunt later ‘from scratch’.

I see community bankers with current yields from 7.5% all the way up to almost 10% and most of these have presented solid earnings recently–but this story is not static and you see from a day like today that it looks like there is an ‘all clear’, but these things always take longer to play out than one would ever predict. Patience!