Making investment decisions even more difficult 3 month CD rates have now moved as high as 4.45% today (on Fidelity)–they had recently been at 4.40% after moving from 4.35% were they had been stuck for some time.

Will they move to 4.50% soon? No one knows for sure, but if congress can’t get a grip on the deficit we certainly could see 4.50% or even higher.

Below are press releases from companies with preferred stock and baby bonds outstanding. Additionally, news of a more macro economic importance may be posted.

Earnings season is over for now and not much news is being posted by company’s that are of interest so for the next 6-8 weeks postings will be relatively lite.

Last year in August I had sold a position in the business development company (BDC) Runway Growth Finance, based on performance concerns and while I still have some concerns the company has improved some metrics.

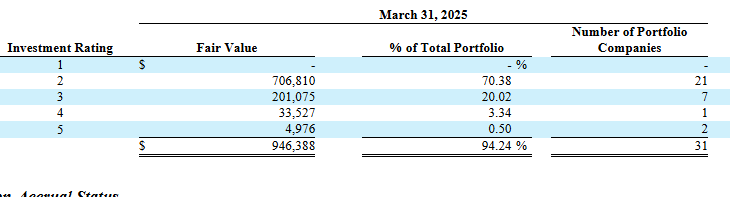

BDC’s almost always rate their investments 1-5 with 1 being the top of the heap with 5 being on non-accrual status. Here is a chart of the current ratings of their companies.

Since December 31, 2024 they have successfully nursed about $30 million in investment from Category 3 into Category 2–improving the overall quality of their investments somewhat. Of course I would like to see everything in Category 1 or 2–it’s all about risk/reward. They continue to have the same 2 investments on ‘non-accrual’ status that they had in December and have forgone about $5 million in interest thus far.

I will keep this on a shorter leash than my other BDC holdings–as well as keep my position small. It is critical that one monitor their BDC holdings. No reason to think there will be big issues–but in this environment of the unknown one can never be too careful.

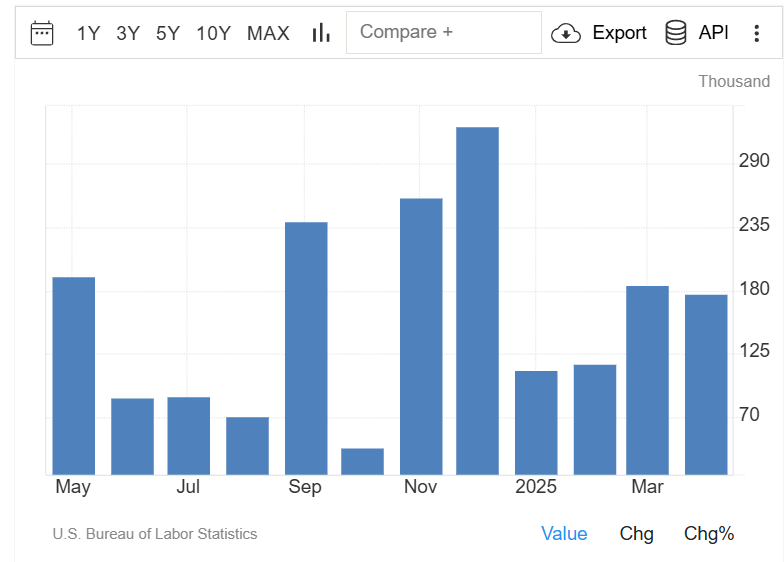

The job openings and labor turnover report (JOLTs) moved higher from last months report–and above forecast. It is interesting that with all the ‘gloom and doom’ talk we just are not seeing any major moves toward softening in the economy. Over the last year new jobs are hanging in there. Job creation is one of the most important numbers in my mind–with decent employment it will be tough to fall into recession.

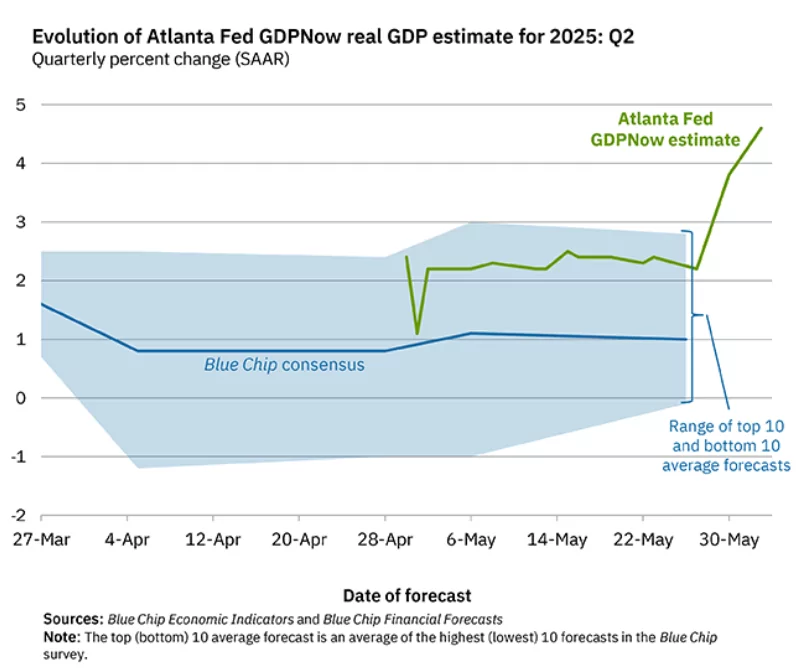

I did see that the Atlanta Fed moved their GDPNow forecast WAY UP.

The forecast for the 2nd quarter is now 4.6%—up from 2.x% just a week ago. Something looks a little fishy with that move.

At the same time the Dallas Fed’s Weekly Economic Index continues to move slowly lower–now at 1.9% which is down from 2.1% the previous week.

I think the level of attention these forecasts deserve is almost none—moving a forecast up over 2% in a week only leads me to believe that they have too many economist at these Fed branches that are cranking out near worthless reports. Certainly room for some cost savings through job elimination.

So this afternoon I am looking to do a little buying–not much, maybe 1 issue. Don’t know what yet, but obviously shorter duration for sure. We’ll see.