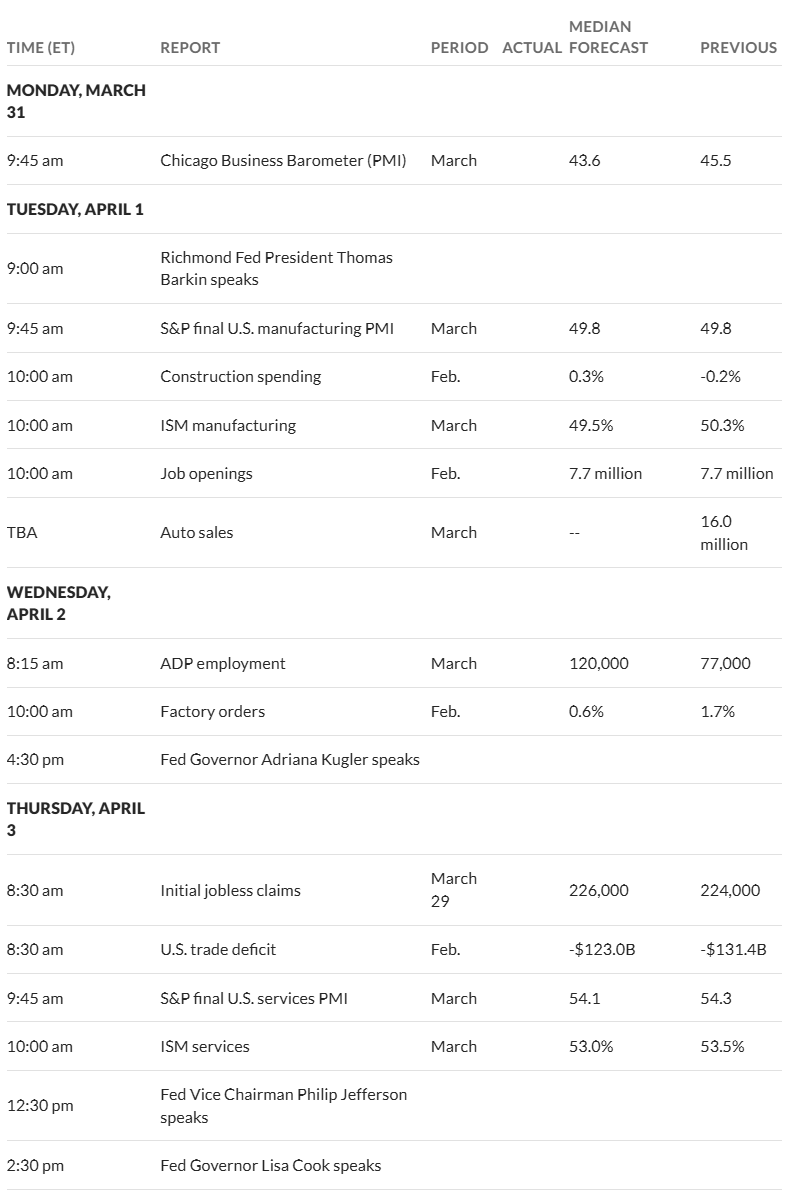

We got some economic news this morning which is likely being mostly ignored by investors. The JOLTs (job openings and labor turnover) report softened a tiny bit from last month–7.568 million jobs open compared to 7.762 million last month. I would have thought this would have softened more with all the tariff uncertainty. ISM Manufacturing softened, but didn’t fall off a cliff–49 versus 50.3 last month, although the price component of the report came in fairly hot.

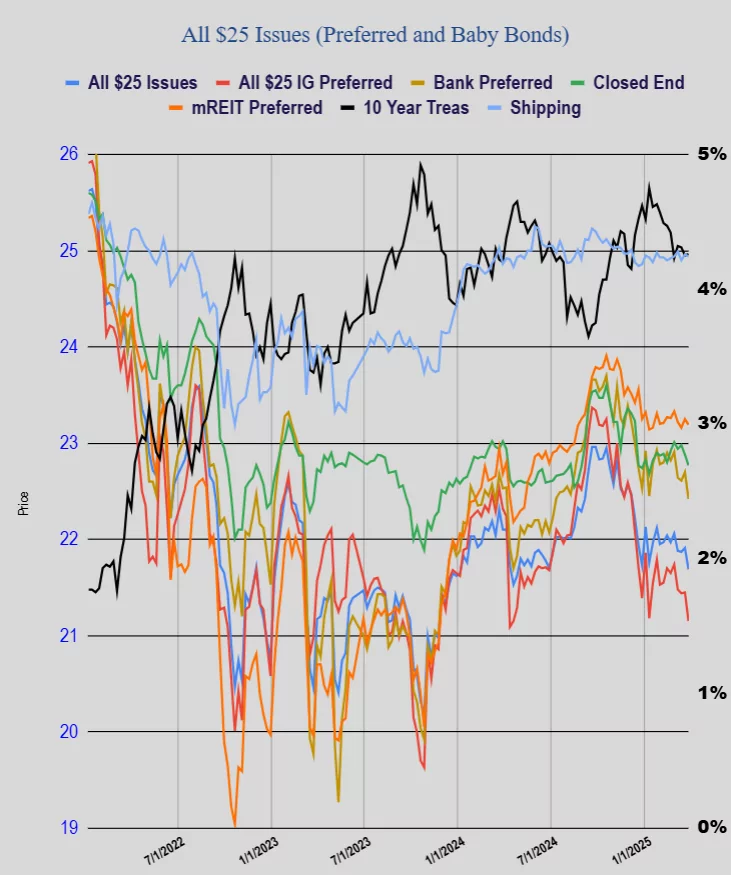

Regardless of the economic numbers the 10 year treasury yield has tumbled by 10 basis points all the way down to 4.14%. Is it a flight to safety or is it a recession being sniffed out? Maybe both.

Preferreds and baby bonds are not acting typical–where big falls in interest rates shove prices higher—looks to me like the green/red ratio is about 50%. Folks are exiting many preferreds in spite of lower interest rates. This tells me maybe I need to buy more high quality low coupon shares today with a potential capital gain coming at some point in time. No use hurrying–with the sour mood out there nothing is going to shoot straight up–unless it is caused by a surprise redemption.

Well now is the time that we start to wait for more tariff news—is the big ‘package’ of tariffs going to hit tomorrow? I suspect some will hit and some will be delayed as negotiating is taking place. Guess we just have to wait and see what happens.