Last week was a trying week for pretty much all investors—only if you were in all cash did you escape the severe losses of Thursday and Friday. I know my losses were pretty minimal on a relative basis much less than 1%–BUT what lies ahead is a total unknown. So I needed to put together of spots I might ‘shop’ depending what occurs in the coming week.

Below are all investment grade issues which have been somewhat beaten down. They are not yielding huge amounts–yet. If markets go into a tailspin and these get beaten down further I may buy–I can’t even define what that means on Sunday afternoon until we see markets open up and trade.

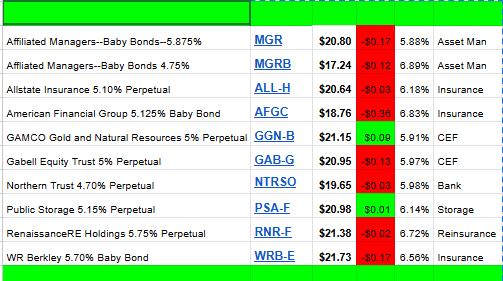

The purpose of this is to identify high quality issues that could have lots of capital gains potential if they get beaten down dramatically in the weeks ahead. This means if there IS panic selling these quality issues may bounce back nicely when the selling is over.

The spreadsheet below IS NOT LIVE—but go to this page for the live chart.