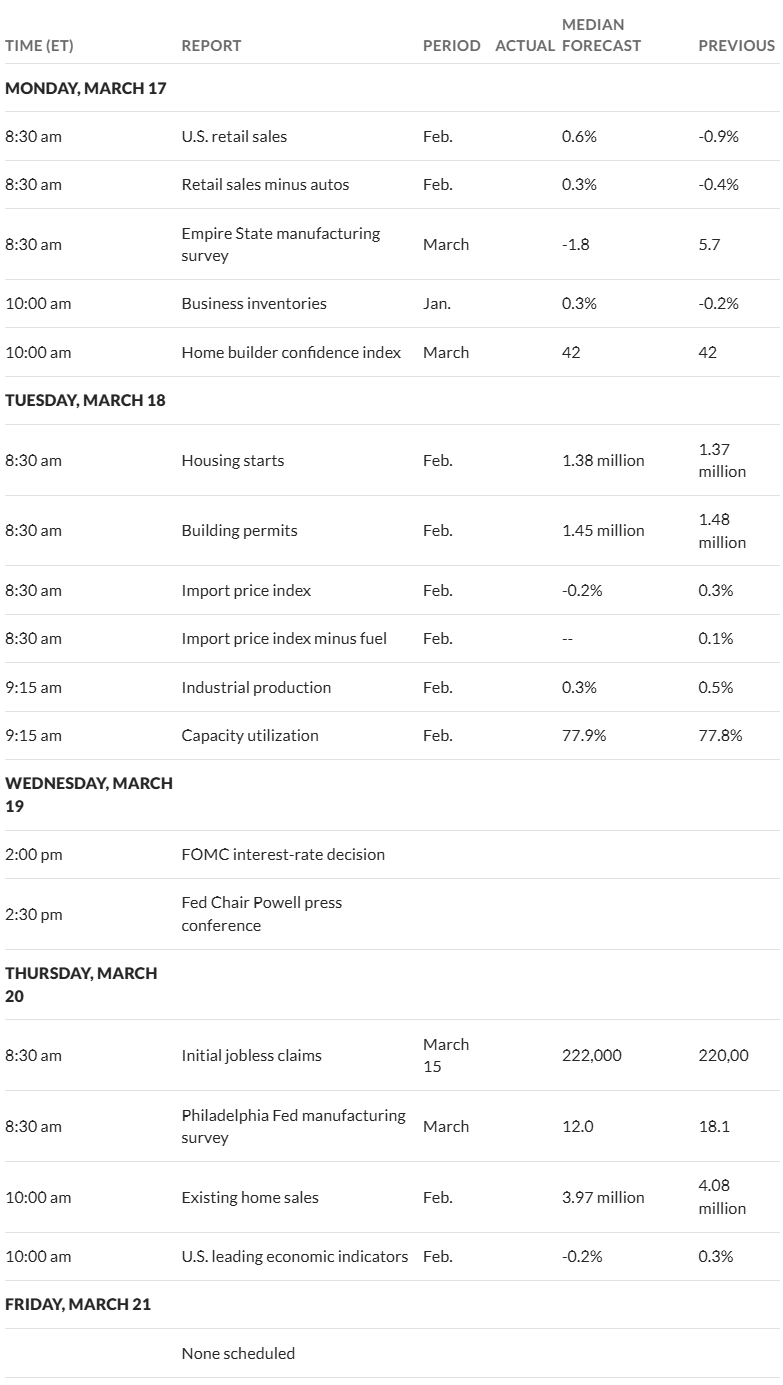

Another week is about to start and like almost every week there could be fireworks in the marketplaces. If it isn’t current economic data being released it is speculation on the future based on tariff policies etc. It is always something.

Last week we saw the S&P500 move lower by just over 2.2%–although without the nice 2% bounce in the index on Friday it would have been a much more negative week. It is not hard to imagine that this coming week will be relative wild as well with the FOMC meeting stating on Tuesday and then making an interest rate decision announcement on Wednesday.

The 10 year treasury yield ended last week about flat on the week–although on Monday it did trade down to the 4.20% area. Economic news during the week–in particular the consumer price index (CPI) should have been friendly to interest rates–but not so as bond investors wanted to be paid more for the risk they were taking. Lots and lots of talk everywhere about the government debt levels and it is making investors pretty nervous. Moods could improve it the Trump administration could show some actual savings from all of DOGE chaos.

Important data this week includes retail sales on Monday–is the consumer still buying and if not how sharply are they pulling back? Then of course the FROMC meeting on Tuesday/Wednesday–where no action is expected, but one never knows for sure.

The Fed balance sheet assets rose by $3 billion last week—expected. The balance sheet has fallen by around $60 billion in the last month–pretty near on target. If the Fed decided to help out interest rates they could readily chop the balance sheet runoff in 1/2 to $30 billion per month or so. I believe that if the economy continues to show softness they may well trim the run off prior to making the next interest rate cut–but who knows.

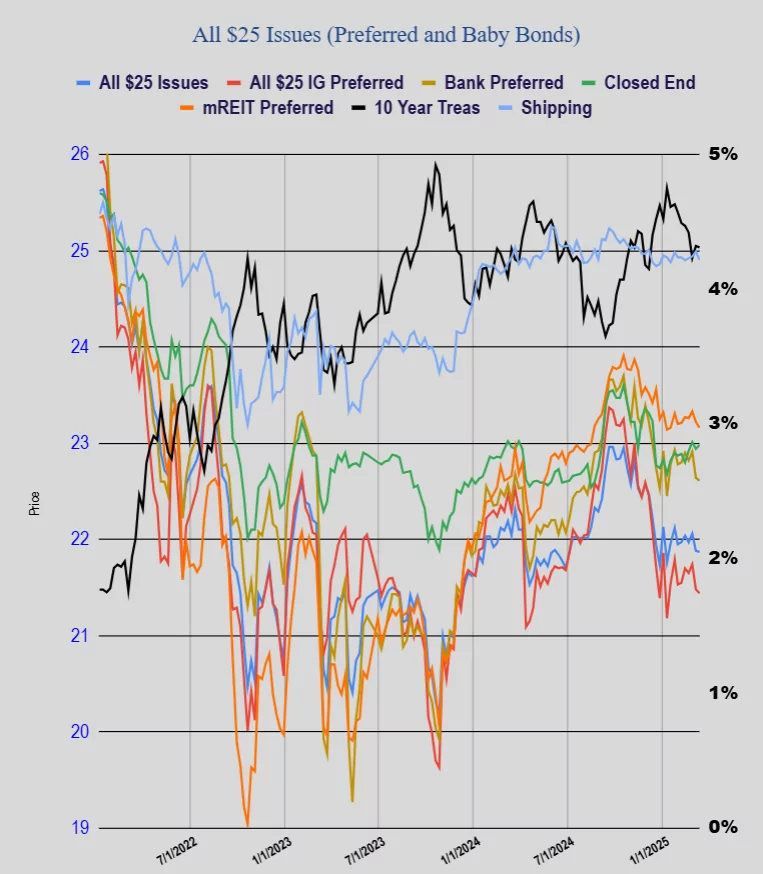

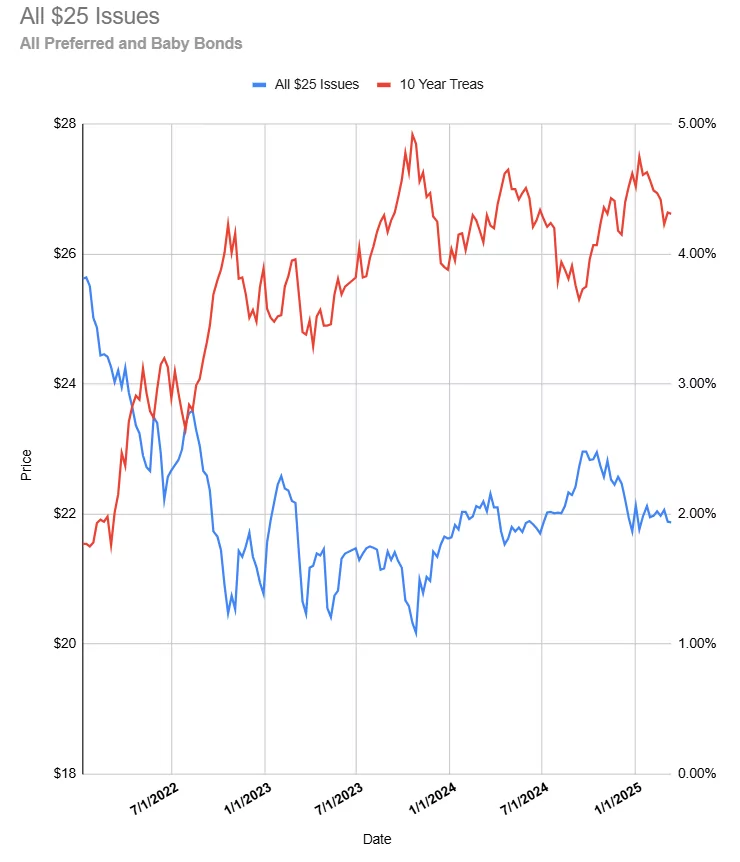

The average $25 preferred and baby bonds was down a measly 1 penny. The past 6 weeks we have seen prices trade in about a 20 cent range (on average). Investment grade issues traded off 3 cents, banking preferreds were off 2 cents, CEF preferreds moved 4 cents higher, while mREITs were down 6 cents. All in all a quiet week. The way I am looking at prices they should be 25 cents/share higher—but investors leaving the market are keeping prices under pressure.

Does anyone have some favorite sock drawer bank preferreds?