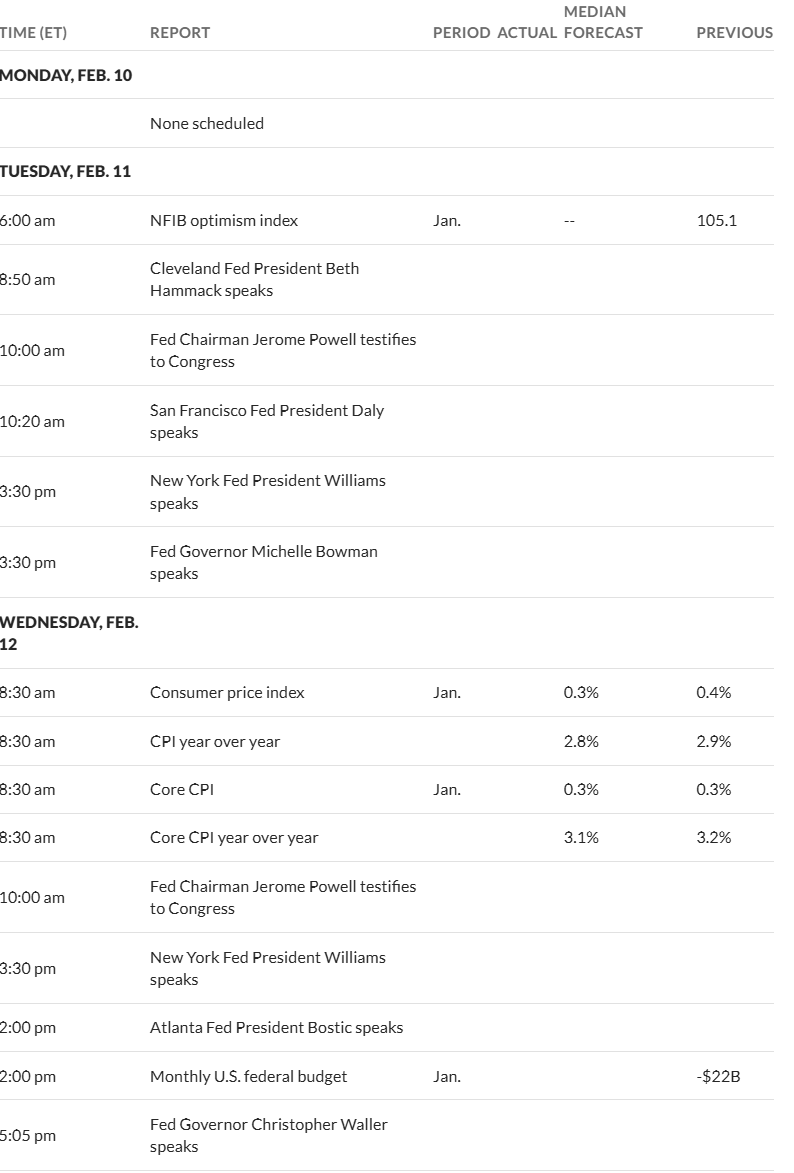

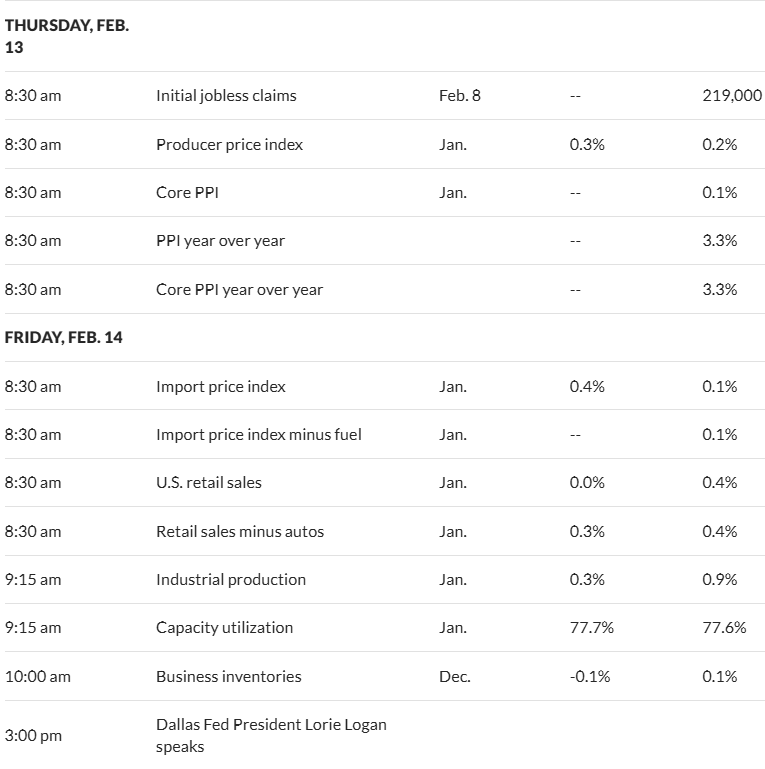

Well we almost certainly have another exciting week to look forward to –up or down who knows, but likely in both directions. Last week the S&P500 moved up just 1/2%, but moved in about a 2% range. This week we have the consumer price index (CPI) and the producer price index (PPI) being released on Wednesday and Thursday respectively and additionally we have Powell testifying before the senate and house on Tuesday and Wednesday. Lots of excitement will be created.

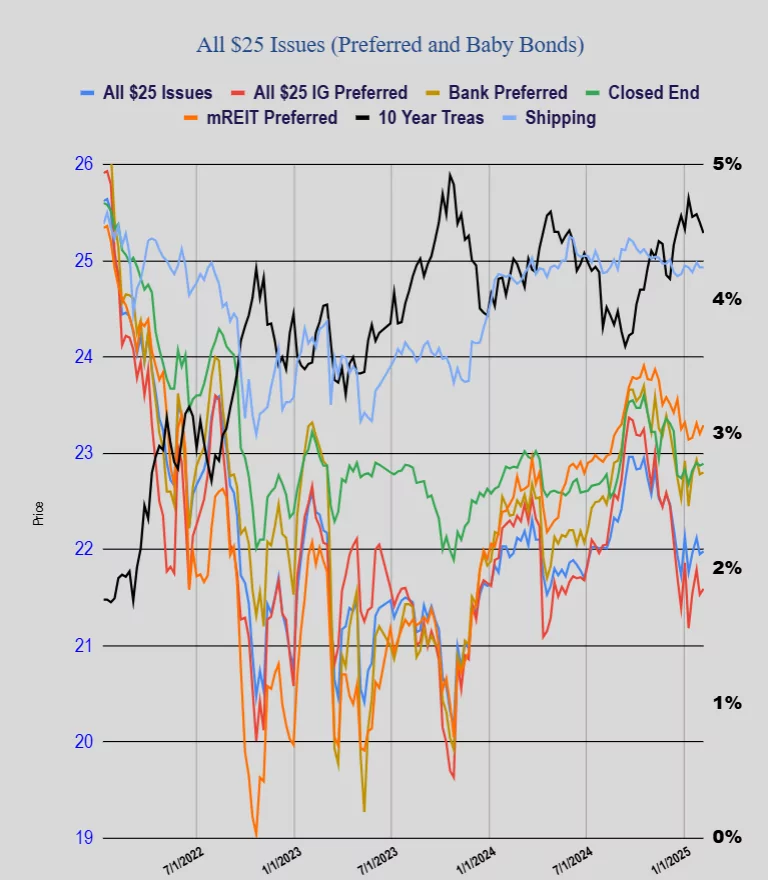

The 10 year Treasury yield closed the week 4.49% which was down 8 basis points on the week. The yield moved in a range of 4.41% to 4.60% for the week. Economic data continues to push rates around–most data has been a bit mixed–some better than expected with some worse than expected.

The Fed balance sheet fell by$8 billion last week as the balance sheet runoff continues.

Last week in spite of interest rates falling 8 basis points for preferreds and baby bonds didn’t respond as the average share price fell by 2 cents. Investment grade issues rose 3 cents, banks rose 1 cents, CEF issues rose 2 cents, mREIT issues rose 3 cents.

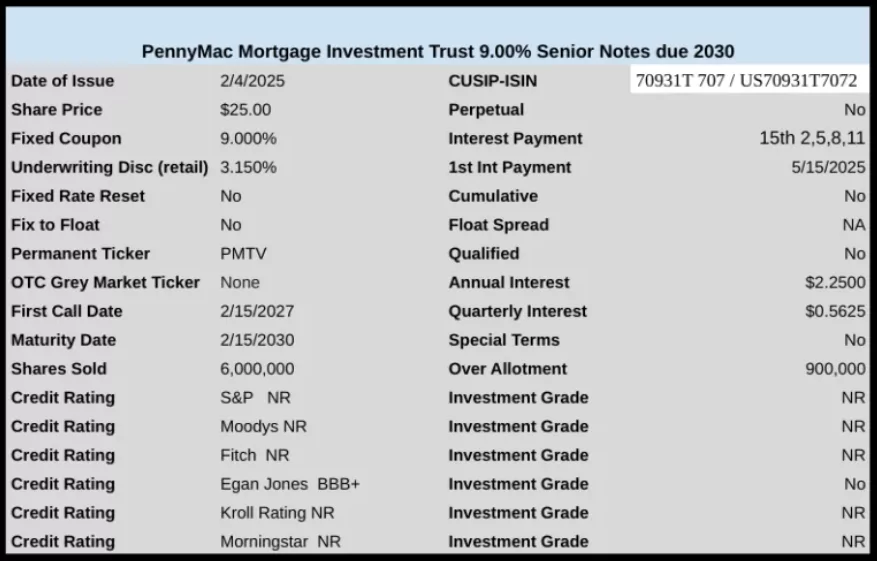

We had one new income issue launched last week as mREIT PennyMac Mortgage Investment sold a baby bond with a coupon of a tasty 9%.

25% tariffs on steel and aluminum imports were announced this morning. Canada, China, and Mexico are all big exporters of steel and aluminum products to the Unites States, but there are other countries in Europe and Asia impacted. This is positive for US steel and aluminum producers, but can they fill the gap created by higher imported metal costs?

Yes, if it is profitable other US steel producers will surely fill the gap, imo. E.g. U. S. Steel itself was once the largest steel producer and most valuable company in the world. Steel and energy independence are apparent goals. Hope to hear something about more refineries soon.

Tacitus,

We would have to go look at the US producers’ production capacity. A lot has been dismantled since US Steel was the biggest producer.

US producers can ramp up the capacity they have, but I suspect they won’t be adding new plants. If they started bringing up new capacity today, Trump would be out of office before it got into full production. Too much risk that the tariffs would end and the new capacity would become unprofitable.

A tif-for-tat there will be reprisals, so prices will go up? That is good for bonds NOT! If this continues the Fed will see inflation creep and raise rates. Nobody wins..

That would be true only if both sides began equal imo and no other variables. Many possible current outcomes in which initially one side tariffs/taxes (VAT) and other side does not. Possible outcomes may be that the side that initially taxed (via tariff/vat) reduces or removes their tariff/tax. Other outcomes are that other non tariff countries or even companies within US borders fill their void. Foreign companies may even move within US to avoid tariff. Another possibility is that the foreign entity’s govt. subsidizes prices so that even after US tariff, prices about same and so they do not lose market share (didn’t China do that before?). Or possibly the consumer buys less of the foreign now higher priced product (e.g. lots of beer prdduced outside Mexico), etc. etc. etc. It is not necessarily simply a static situation in which importer pays more, passes price to consumer, and prices rise. FWIW just looked at bonds, not much happening most yields even bit down. Anyhow gotta go, but must be a some better scenario than US exporters unilaterally paying tariffs/taxes to a foreign country vs. that foreign entity paying none to export here. We will see what happens but as recall inflation fairly low first time around 2016-2020 when this occurred.

Moving on.

Not sure how much of an immediate impact there will be. I believe that with the exception of Mexico and Canada, there were already tariffs at that level or, alternatively, quotas that restricted imports: https://www.yahoo.com/news/biden-announces-tariffs-chinese-steel-145242150.html And the story in the NY Times this morning says “it remained to be seen if there would be any exceptions, for example for Canada and Mexico.” So that may be a subject of future negotiation. So the markets may be correct in assessing this action as one that will not, standing alone, create a major shock to the economy.

Roger,

Biden’s tariffs last summer were to try to close off a loophole in the prior Trump/Biden tariffs that China was exploiting (transshipping Chinese metal through Mexico).

Tariffs of Chinese steel have a long and storied history. The Chinese have built huge capacity and are happy to sell below cost (i.e. gov. subsidy) to help prop up their economy.

On the one hand, the US should be happy to buy cheap steel (reduces prices of goods), but on the other hand, too much cheap steel hurts the US steel industry. Finding that balance point via tariffs is tough, especially when presidents use tariffs/tariff announcements as political tools.

We haven’t crawled through the details of US/China metal trade in a LOT of years, but at one point the US was much smarter about targeting specific grades/types of metals and letting lower grades others come in cheap as a way of striking the balance.

From what I remember, the US industry shut down most of its capacity to produce those lower grade metals, so all tariffs will do is raise costs to us buyers (i.e. the US producers can’t fill the gap). Better to take advantage of the Chinese subsidies for those kinds of metals.

I am kinda hoping Trump’s announcement will turn out to be more nuanced that just the “blunt instrument” he mentioned, but time will tell.