Are you ready for the week?? I don’t know if I am–but I guess it starts today so ready or not here we go.

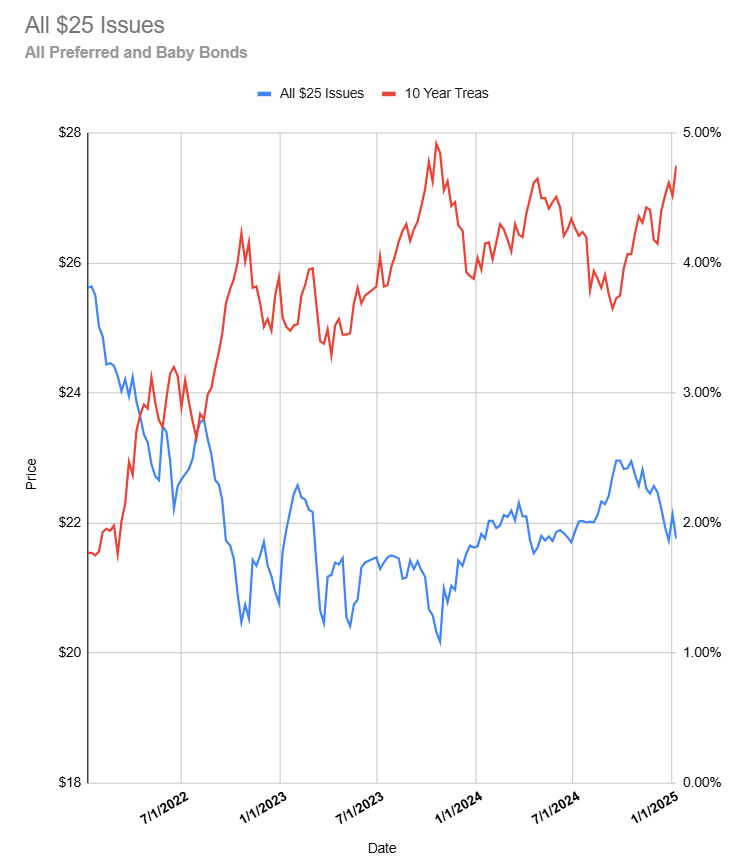

Last week we saw the S&P500 setback by around 2%–precipitated by strong employment numbers released on Friday. Interest rates were already elevated from the previous week by about 10 basis points–but then the employment numbers sent the 10 year Treasury up another 10 basis points to the 4.80% area.

The 10 year treasury closed up 18 basis points from the previous Friday at 4.78% although the yield hit 4.80% earlier in the day. Quite obviously investors are concerned with strong employment which is coupled with $113 billion in new Treasury money being raised and now they want to be paid more to fund the debt of a deteriorating situation.

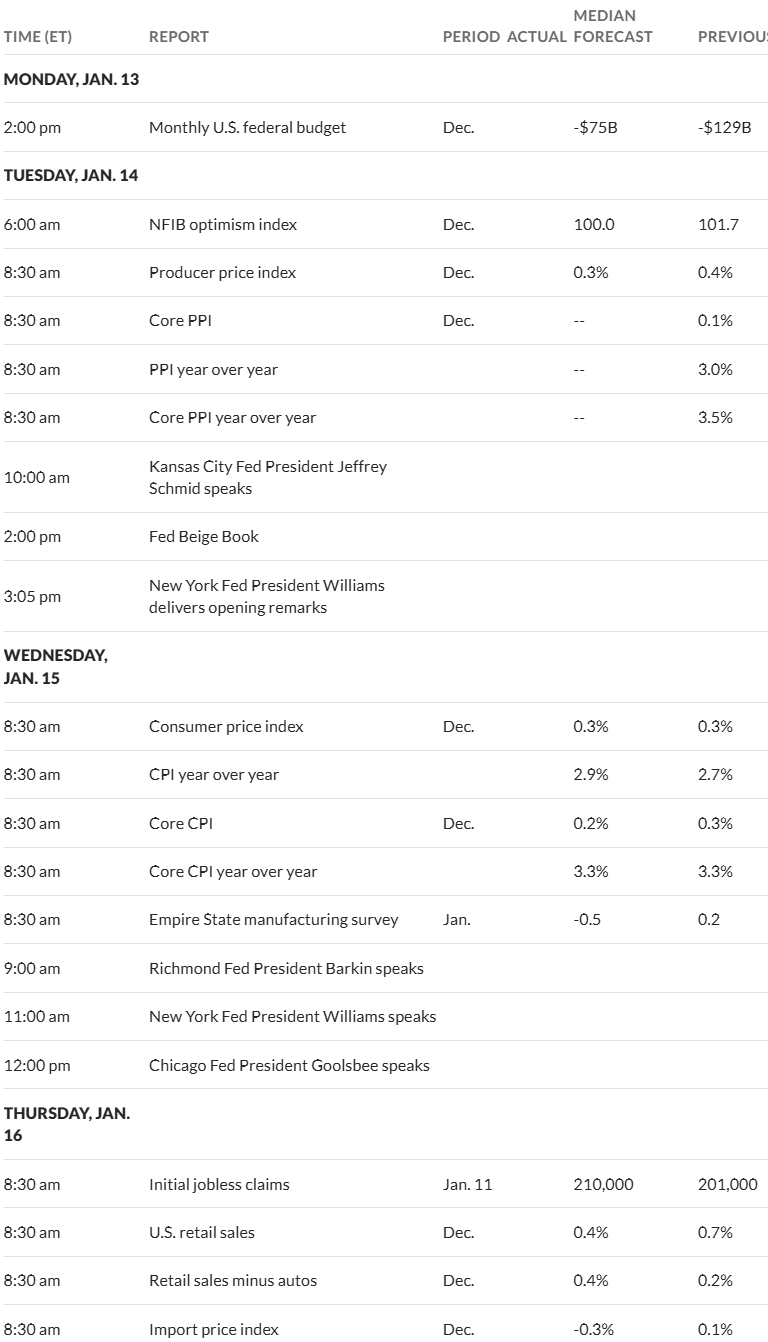

Of course there is never a let up in this tense economy in data. The coming week we will see little economic news on Monday, BUT then we have producer prices (PPI) and the Beige Book on Tuesday and then consumer prices (CPI) on Wednesday. Retail sales get added to the mix on Thursday which will give us another read on economy. Looks like the making of another potentially wild week. We’ll see soon enough.

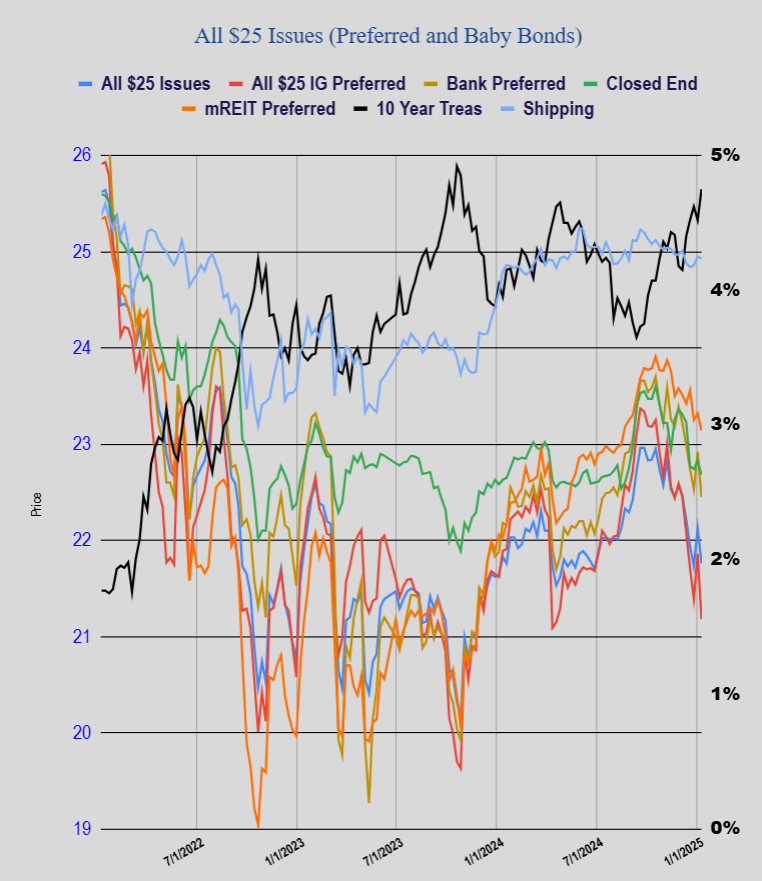

As one might expect the average $25/share preferred and baby bond fell in price. The overall average fell by 41 cents with investment grade issues falling hard by 68 cents. Bankers fell by 47 cents. Closed end fund issues fell by 17 cents, mREIT issues fell 18 cents with shippers moving 2 cents lower.

Note that lower quality, higher coupon issues fell the least. Additionally CEF issues were reletively stable because a large percentage of the issues are short duration baby bonds or term preferred.

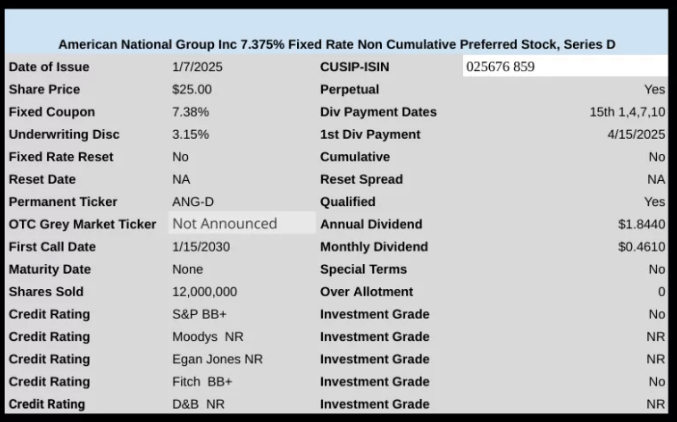

Last week was a relatively busy week in new issuance in income issues. None of the issues below are investment grade, but the 2 insurance companies are just a notch or so below investment grade–in a stable market the 2 insurance issues would be excellent buys for most investors with coupons that pay nicely. Obviously with interest rates threatening to go higher it is anyone’s guess whether they go up or down in share price.

CA insurance is in turmoil.

Governor and his cronies just put through a plan to allow home insurers jack up prices (just before the fires), and we are hearing about more coming. Insurers are dumping policy holders like crazy. One of my kids is trying to change houses (moving about 10 blocks into a bigger house). His current company (state farm) refuses to insure the new house. “no new policies” – even though it is in a pretty low risk suburban community. Farmers will insure it, but the price is almost double – and they want to do a home inspection if the house was repiped to copper more than 10 years ago, of if the roof is more than 10 years old (and they may not cover the roof or the plumbing). He can’t even get a call back from Mercury.

With the wildfires, some of the CA utility preferreds are getting hammered, including some from companies that don’t supply LA.

Baby with the bathwater?

Some good opportunities? Of course, I don’t make recommendations, but might be worth a look.

10 yr high so far today 4.805%

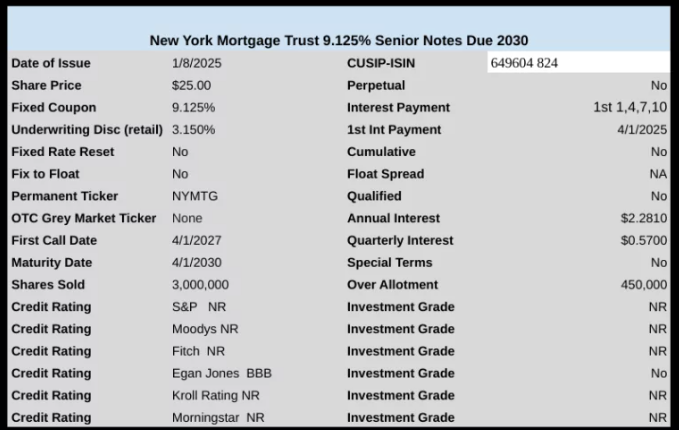

Has anyone found out what the ticker symbol is on the new Southern Company 6.5% ?? I have the cusip # but still needing the actual ticker symbol.

Not an expert either but I do look at bonds and all of a sudden noted Mercury’s (MCY) yield up- they are insurer in California, hmmm. To tell you the truth I generally have avoided most housing related investments e.g. REITS, that are based in California, especially southern CA.

I’m sure no insurance specialist but who will be the main players in paying for all the billions in damage in California? Will the big players have there credit ratings downgraded? Will there be preferreds and baby bonds affected?

I googled & also used Microsofts Co-Pilot and they both mentioned that FEMA has a “50% Fema Rule” implying that Fema would pay 50% of the cost to rebuild a home but would certainly not cover the full cost. According to many reports out there they are saying many people did not have fire insurance so they are going to be in serious trouble. I also read that the “average home” price in Palisades, Calif. is between $3.5 & $3.7 million.

FEMA covers floods. If you bought a flood policy. This is a fire. Fire loss costs are covered by private home insurance policies. In CA market: mutual companies, the state high risk plan, publicly traded insurers. See PickleNicks list. The retail insurers often backstop their excess risk with reinsurance or cat bonds. The giant “economic loss” headline numbers include soft losses (lost wages, lost sales) and are clickbait, As a rule of thumb divide AccuWeather etc’s latest headline number by 4 or 5 to get closer to insurance industry “hard losses.” ie value of homes destroyed.

Tip: not a bad time to pull out your homeowner policy and read it. A lot of people will soon find there is a big difference between Actual Cash Value and Replacement Cost. Also, make sure the RC number is realistic. (Sometimes called the 80% rule.) Just my opinion. DYODD.

Don’t worry about the alarmingly big numbers until the carrier-by-carrier impacts get clearer. Risk is the insurers business. Excess risk beyond projections is the problem.

From Copilot AI:

Some of the major insurance companies operating in California include:

State Farm

Allstate

Farmers Insurance Group

USAA

Travelers

Nationwide

Chubb

I own an Allstate issue. I expect a credit down grade, it’s not the best run company.

In my opinion it will be a good 6 months before we have any idea as to the answers to your other questions. But I’m sure they are lining up liquidity and lawyers to deal with the state regulators.

The 1991 Oakland hills fires saw both All State and Farmers delay payments.

They faced numerous lawsuits for non payments and fines even 20 yrs after the firestorm. I guess if you delay and invest you can earn enough to pay what you owe.

If anyone here has a subscription to the LA times if they could copy and paste it.

https://www.latimes.com/business/la-xpm-2011-nov-01-la-fi-oakland-fire-20111101-story.html