Last week was a winner for the S&P500–not by a giant amount but by 1.6% which was essentially the amount of loss in the previous week. Daily we had moves of this size, but we had a couple days last week that started with really big losses, but each time traders drove the index back higher. The index is much higher on the futures market this morning–so looks like we will party for at least a few hours.

The 10 year treasury yield was off by 2 basis points for the week–closing at 4.41%. During the week was saw the yield as low as 4.34% and as high as 4.49%. This morning rates are lower–it at the 4.37% level–but all know that this is pretty meaningless as to where the yield will go during the day and where the day ends. This week we have a key piece of data in the personal consumption expenditures inflation released on Wednesday –the is the big piece of data on he week. We have the FOMC minutes from the last meeting released on Tuesday. Of course on the Thursday we have the Thanksgiving holiday and so there is no economic news being released Thursday and again on Friday.

The Fed balance sheet took a giant sized move lower last week–down by $47 billion.

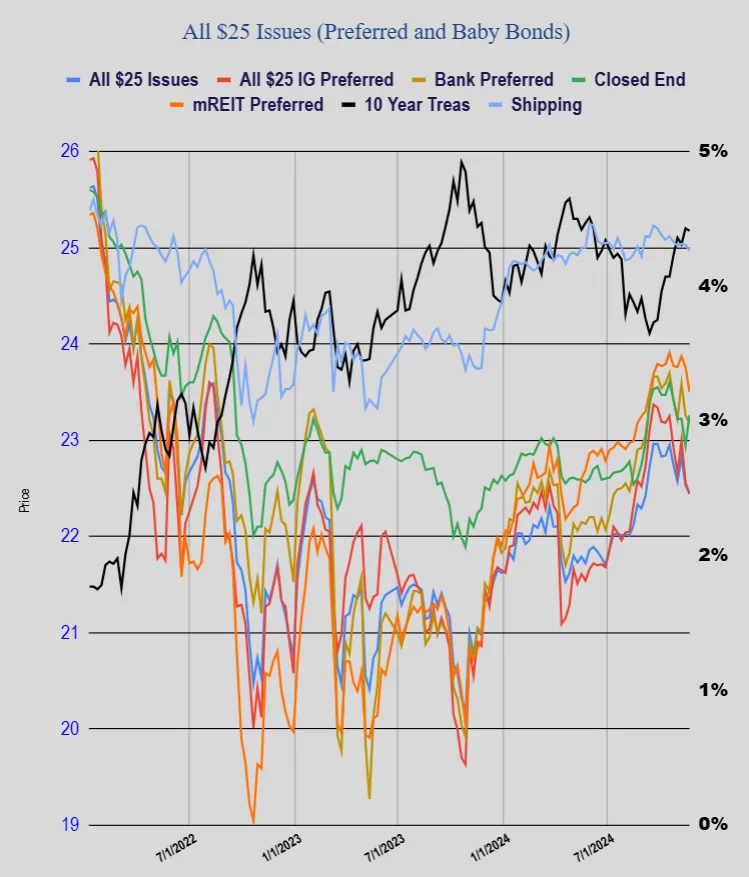

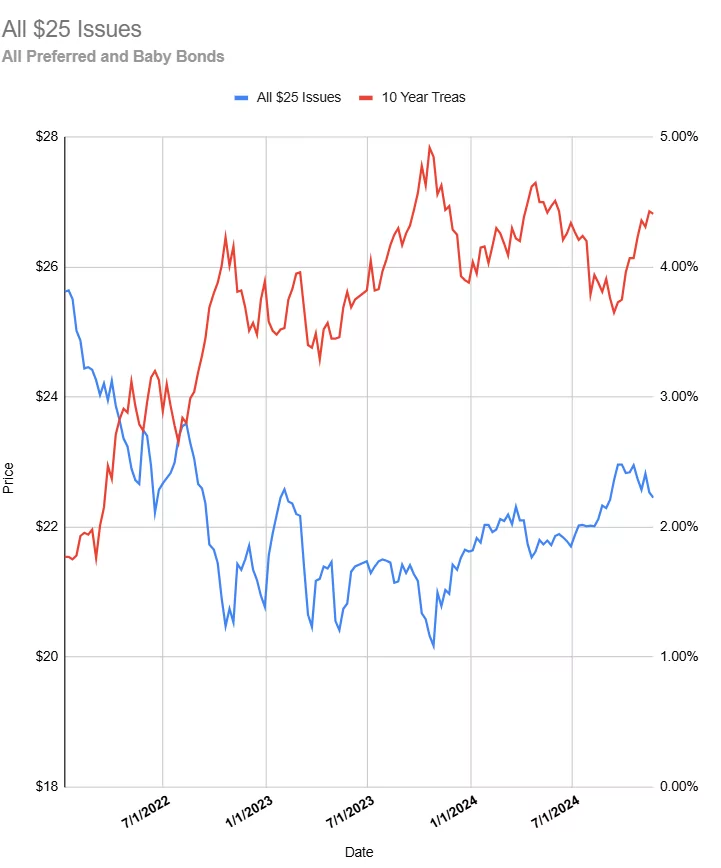

The average $25 preferred and baby bond fell by 7 cents last week. Investment grade issues fell by 12 cents, banks fell by 9 cents, mREIT preferreds fell hard by 26 cents and shippers were off by 6 cents. The big winner on the week were CEF preferreds took a 32 cent jump as the surprise call from Priority Income Fund took all of the PRIF preferreds higher.

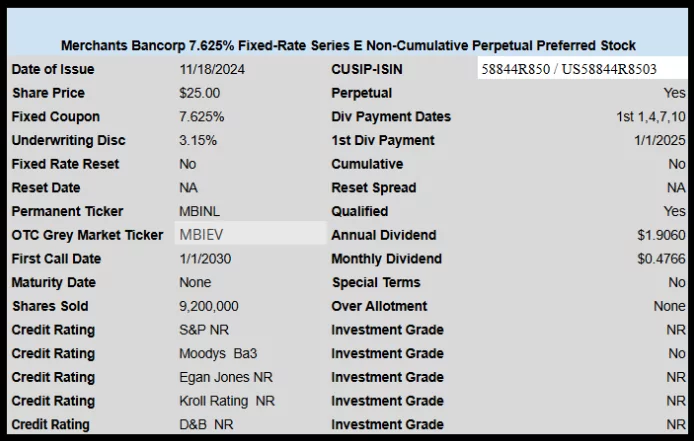

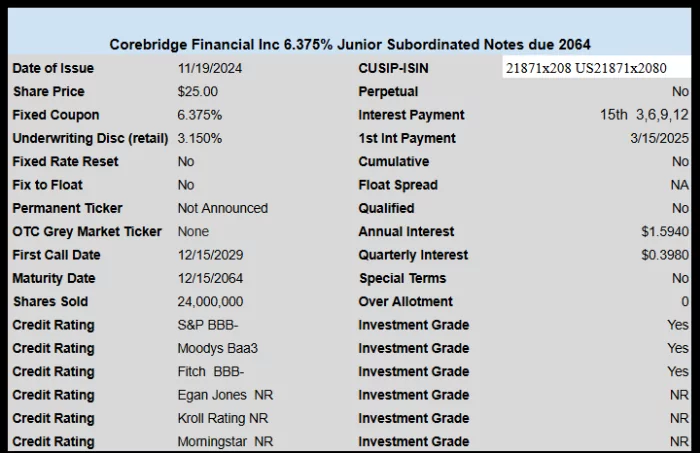

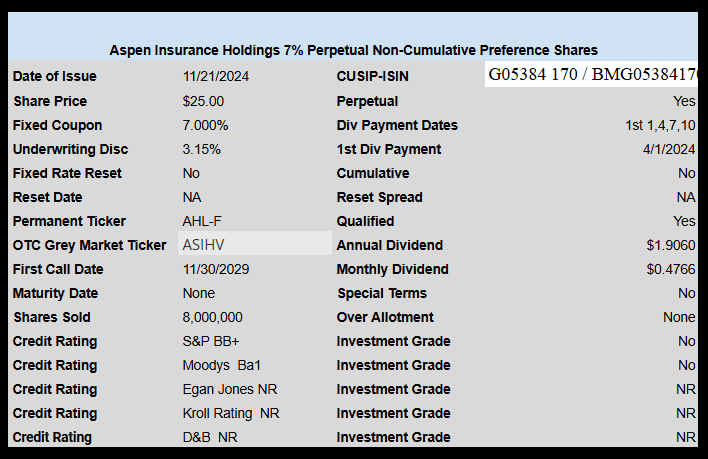

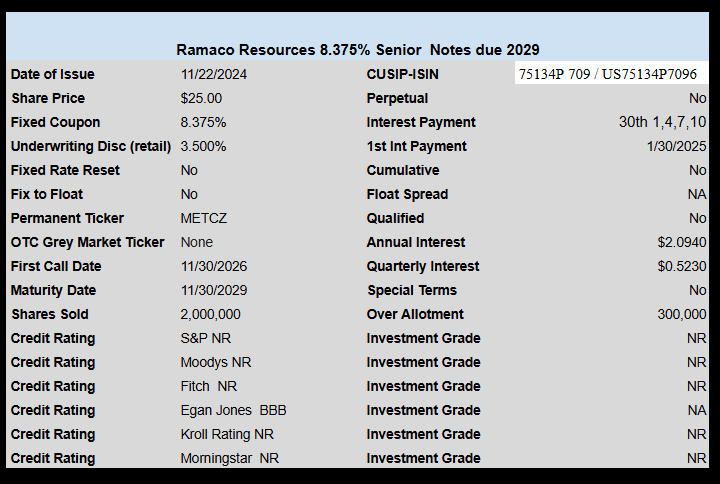

Last week we had 4 new income issues price. This is the busiest week for new issues in the last year or so.

The pricing term sheet can be found here.

The pricing term sheet can be found here.

The pricing term sheet can be found here

The pricing term sheet can be read here.

Good morning, Tim and all us III’ers.

Tim – I hope all went well the the medical visit.

mbg–actually just had to take my wife in for some testing–fortunately all went well.