Last week, once again we saw common stocks moved higher by 1.1% (the S&P500)–doesn’t matter whether the economic news is good or bad–there remains almost a never ending pot of cash available to buy common shares—because they only go higher (sarcasm intended). Well it is always better when common equities move higher (or remain flat).

The 10 year Treasury yield closed the week at 4.07% which was 11 basis points higher than the close the previous Friday. Inflation was slightly hotter than anticipated as measured by the CPI, but a bit cooler as measured by the PPI. Longer rates are continuing high regardless of Fed Funds rate cuts–simply the Fed can move very short term rates–but longer term rates will be determined by the marketplace. This week should be a bit quieter–the bond market is closed on Monday.

The Fed balance sheet was virtually unchanged last week. There has been no change in the monthly runoff target–it remains at $60 or $65 billion (forgot which it is) a month. If the Fed wan’t to take some pressure interest rates they could consider reducing this runoff.

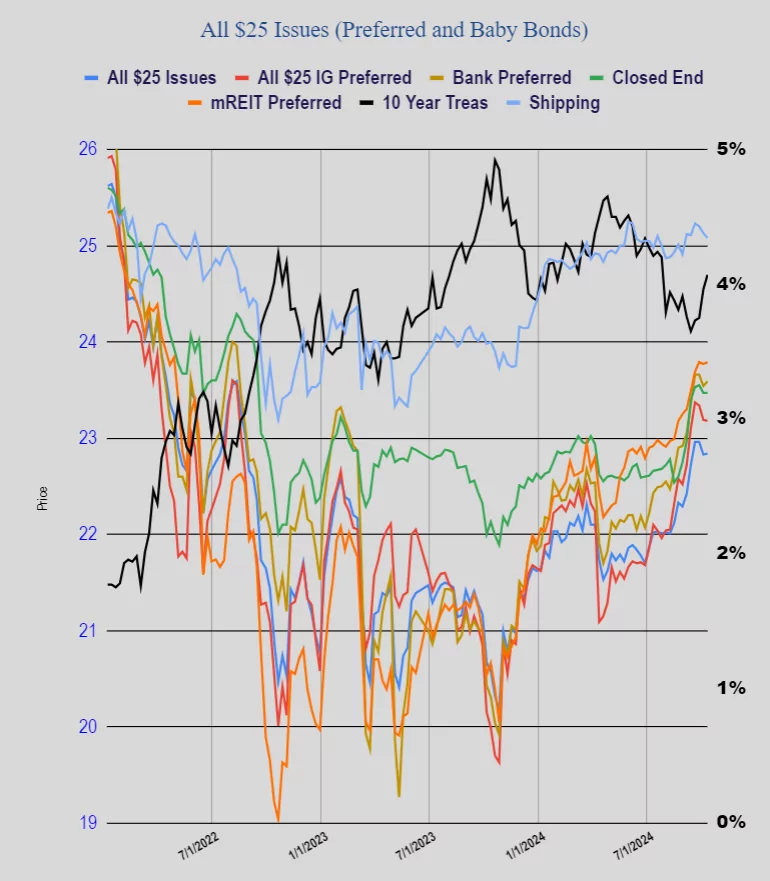

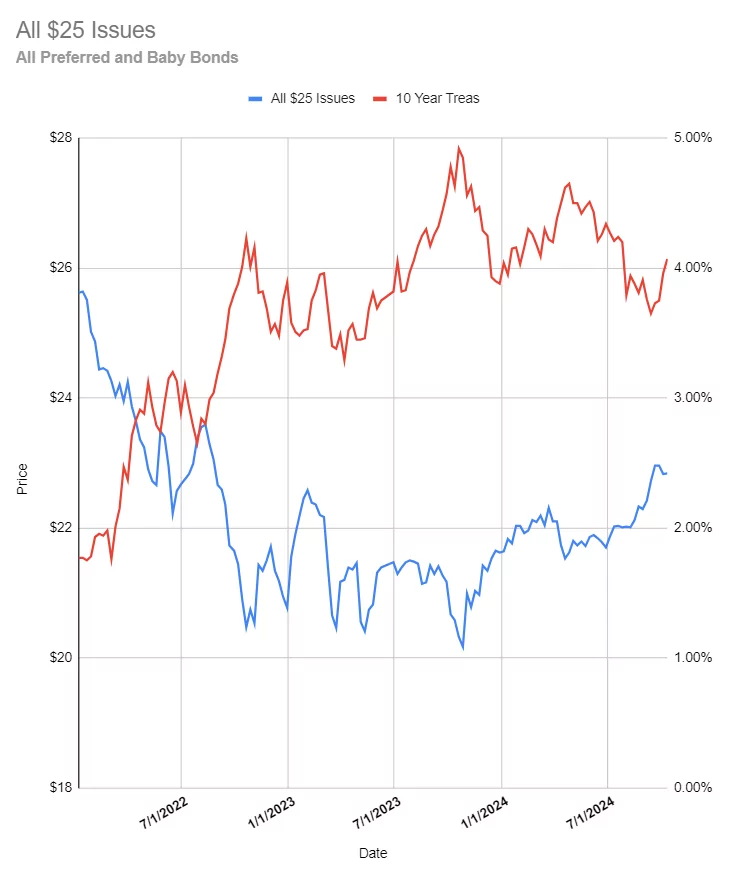

Once again we had a preferred stock and baby bond market remained fairly flat with the average $25 shares moving 1 cent higher. Investment grade issues moved 1 cent lower, banks moved 5 cents higher, CEF preferreds were flat, mREIT preferreds moved 2 cents higher while shippers were 5 cents lower. All in all for a week that saw the 10 year Treasury moving 11 basis points higher a break even week was just fine with me.

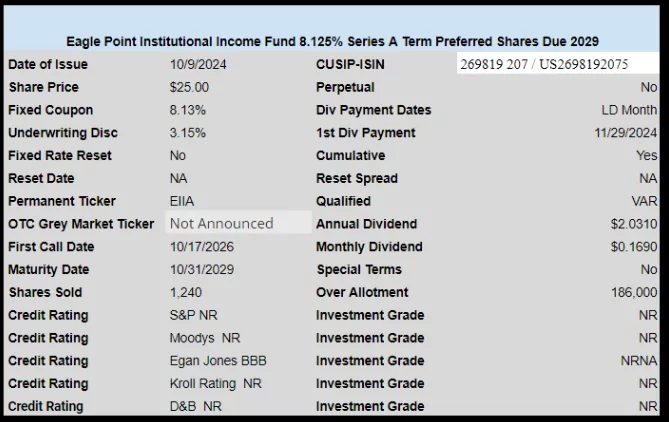

Last week we had one new income issues price. Eagle Point Institutional Income Fund (untraded) sold a new term preferred with a coupon of 8.125%.