Well finally the S&P500 setback by a fair amount last week–down by near 2%. We haven’t seen this type of loss for quite a while. It is meaningful? I doubt it, but obviously no one knows. My concerns always are that steep losses in common shares can drag down income issues, but that was not the case last week. Once again it was the tech shares driving the bus as NASDAQ moved sharply lower. This morning NASDAQ is bouncing nicely as is the S&P500.

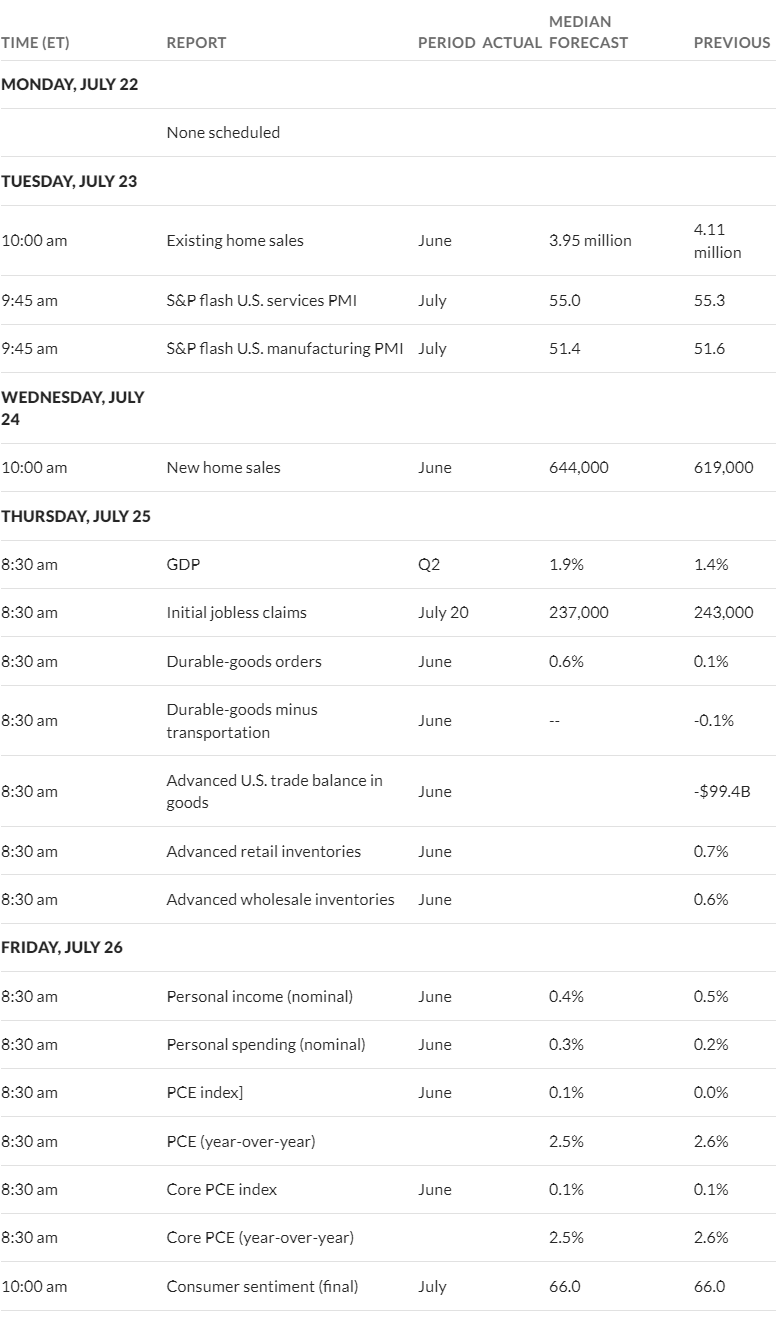

Interest rates moved around in a somewhat narrow range last week and ended the week flattish on the week. The 10 year treasury yield moved in a range of 4.14 to 4.25% before closing at 4.24% which was up 5 basis points on the week. Strong retail sales announced last week was the biggest fly in the ointment relative to a Fed Funds rate cut. Jobless claims came in higher than forecast and 20,000 higher than the previous week.

This week we have 1 super important number in the personal consumption expenditures (PCE) inflation numbers. While we have a FOMC meeting at the end of this month I think the case for a rate cut (or not) in September is being built now. Stronger inflation reports, whether it be in PCE numbers or in coming CPI numbers must be built starting now or the anticipated September rate cut will be ‘off the table’. This week we have 2nd quarter GDP released on Thursday and then PCE on Friday.

The Federal Reserve balance sheet fell by $26 billion as it works its way down to $7 trillion–as always building the ability for future quantitative easing which undoubtedly will be needed at some point in the future.

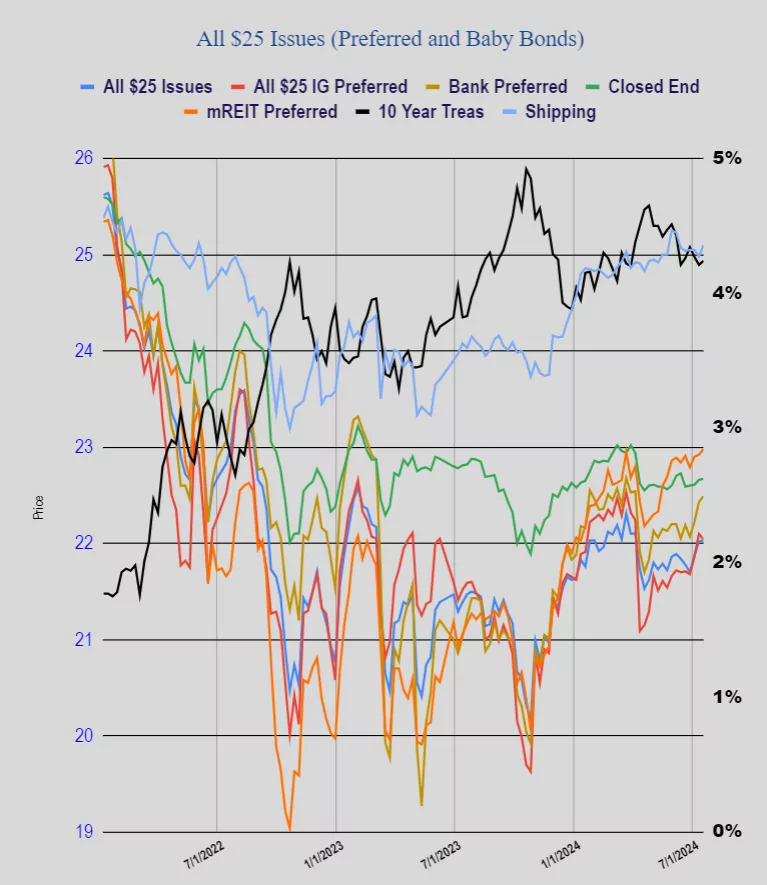

Last week we had nearly flat prices in the $25/share preferred stock and baby bonds as the average share moved a single penny higher. Investment grade issues moved 6 cents lower with banks up 6 cents and mREIT issues up 6 cents as well.

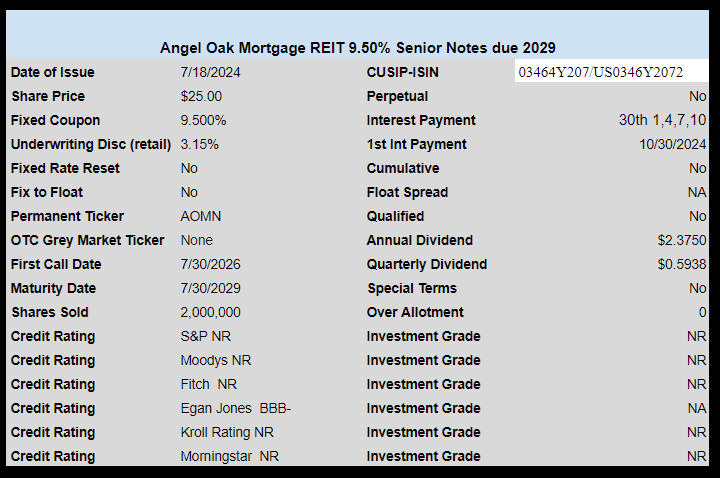

Last week we had 1 new exchanged traded baby bond priced. Tiny Angel Oak Mortgage REIT (AOMR) priced a new baby bond at 9.50%.