Well the equity markets were higher last week, but only by just under 1% in the S&P500. The NASDAQ was off just a bit and the tech issues in the NASDAQ drive the bus when it comes to the S&P500. All equity indexes are up quite a bit this morning – by around 1/2%.

The 10 year treasury yield fell by 17 basis points last week to close at 4.19%, although right at this moment the yield is up 3 basis points to 4.22%. Of course last week we had new consumer price index and producer price index numbers released with the CPI coming in favorable, but the PPI number coming in slightly hotter than forecast.

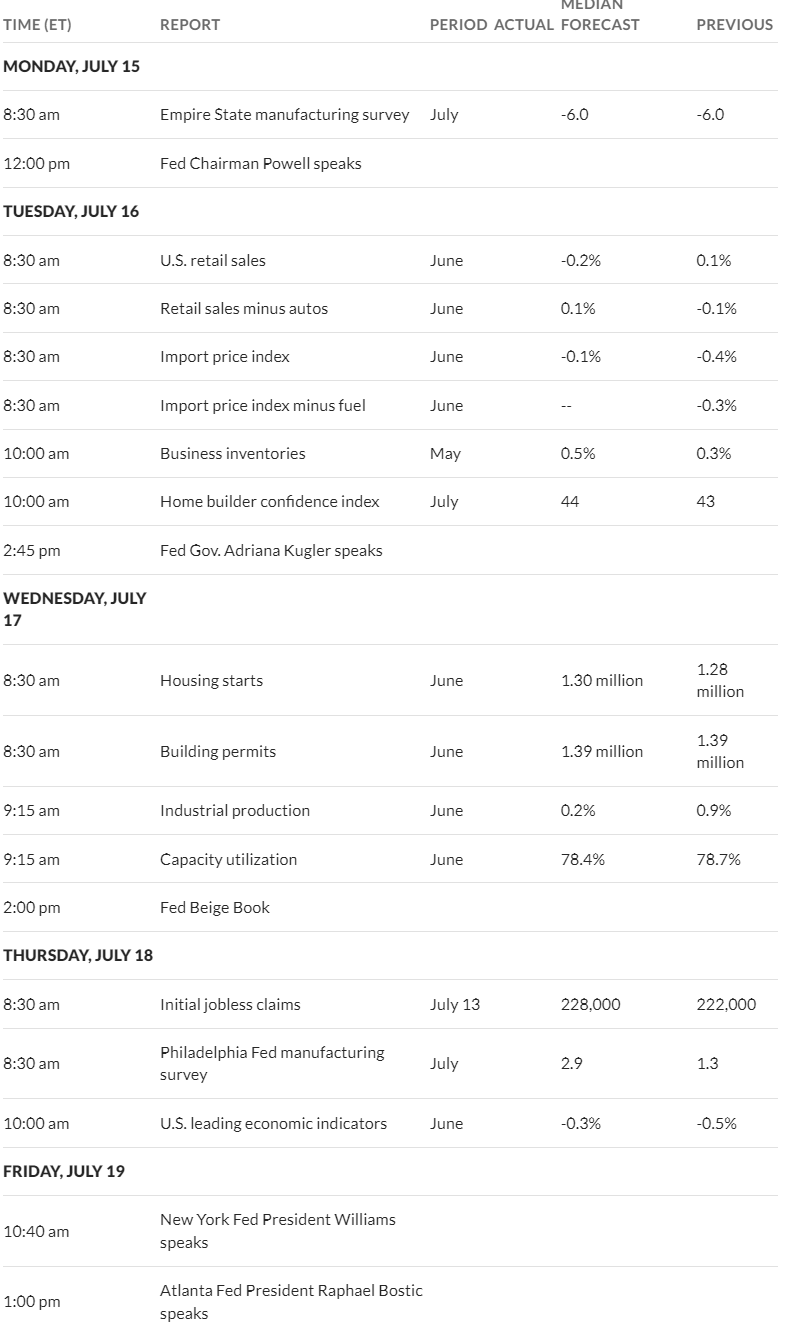

This week we have quite a bunch of more minor economic news being released as well as a decent number of Fed yakkers. I am not certain we will see big movements in rates this week–or if we will be kind of quiet until we get big numbers next week in the personal consumption expenditures (PCE) numbers.

The Fed Reserve balance sheet assets rose by $3 billion last week as we continue on the path down on a $65 billion monthly runoff.

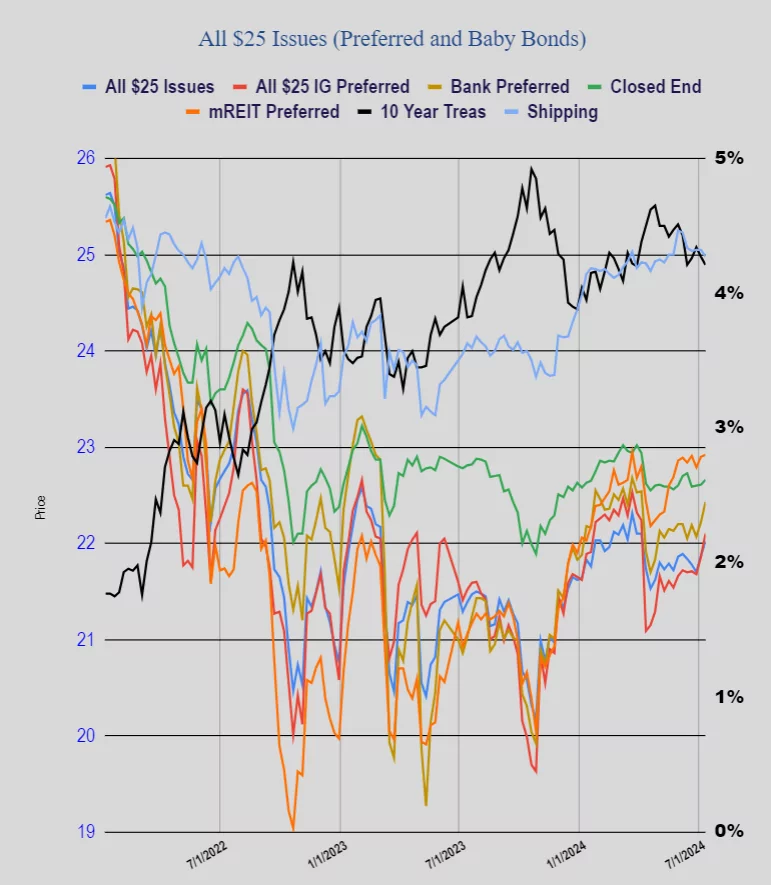

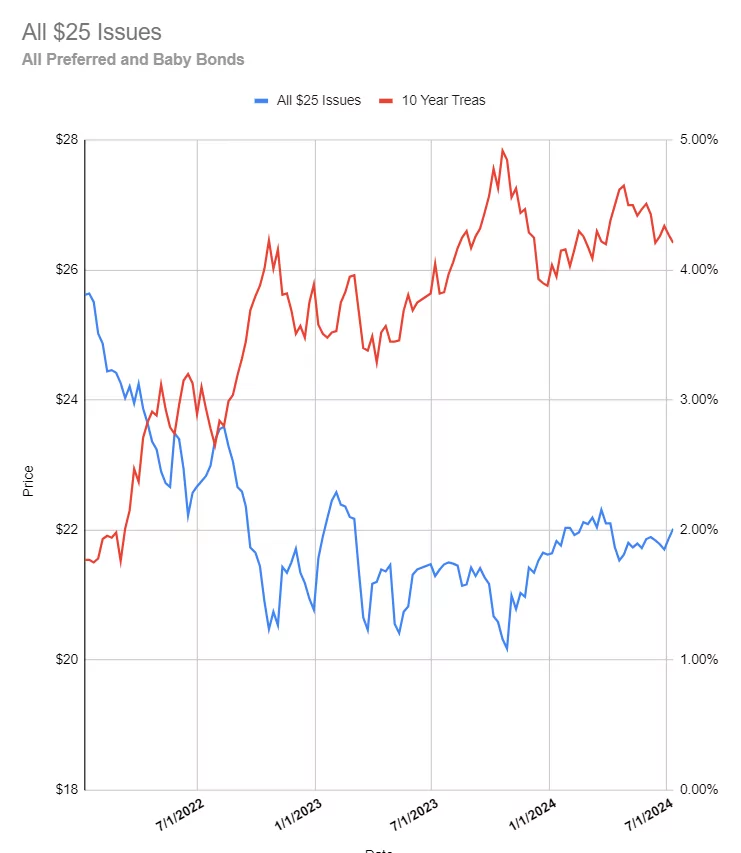

Once again we got a modest bounce higher in $25/share preferreds and baby bond prices. The price movements the last 2 weeks have been very modest, but at least they are moving higher in tandem with falling interest rates. The average share price was up 15 cents with investment grade up by 24 cents, banks up by 21, CEF preferreds up 6 cents and mREIT preferreds up 2 cents. The shipping issues were down by 6 cents, although they remain the highest priced preferreds sticking around the $25/share area.

Last week we had no new income issues priced–guess everyone is waiting for lower rates.

Good morning and happy trading!