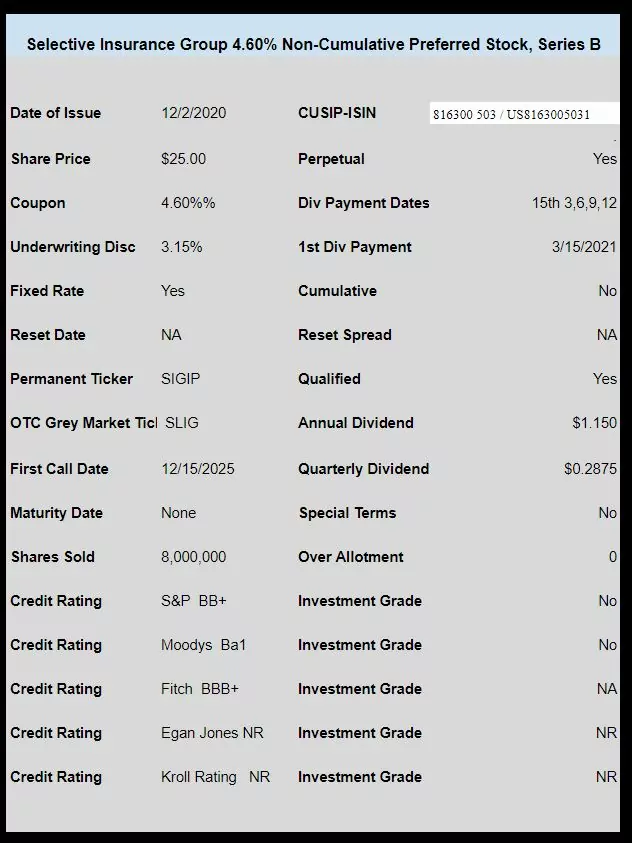

Below are the details of the new Selective Insurance Group (SIGI) preferred stock.

The issue will trade under OTC grey market ticker of SLIG today.

The pricing term sheet can be found here.

6/6/2025

Our site runs on donations to keep it running for free. Please consider donating if you enjoy your experience here!

Below are the details of the new Selective Insurance Group (SIGI) preferred stock.

The issue will trade under OTC grey market ticker of SLIG today.

The pricing term sheet can be found here.

I had too much of my nest egg in SCE PH and PL so I sold the PL yesterday at 24.05 I harvested my original investment and upcoming dividend.

3 months ago wildfires in Calif. would scare investors, now everyone is greedy for yield.

The markets have gotten ahead of themselves with the vaccine news. The economy has been slowly coming back, but what next ? States like Calif that shut down the economy in the spring showed a decline in sickness and death. This time states can’t afford or even be able to do a shutdown like the last time. But with the recent Thanksgiving holiday and Christmas coming up we will see a increase in the sickness and death. With the relentness drumbeat in the news, peoples fear of going out will slow the economy, that is except for internet sales. Of course if the delivery companies can get enough drivers.

I expect another leg down when reality hits.

We should all be concerned because every new preferred issue that comes to market is

already priced too high before we have an opportunity to purchase. The yields are low enough without having to pay $26 the first day the shares are available. That is what I am finding. Thanks

You could take that as a positive indicator for the company in general. I always say there’s a rating, and there’s where it’s trading. Not necessarily the same. I have some investment grade issues tied to a Bermuda based re insurance family…. Well rated trading poorly!

Then you get some BB paper that’s over 29 with sub 3 ytc. It’s almost like when a sports gambler says” What’s the spread telling you?” Over twenty years their commons have trended up. They look like a survivor.

No wait list orders were filled. Oh well.

Also, I was in error re ratings. Was told it was IG – and it isn’t (other than Fitch).

rb–I see it trading at 25.80

I don’t see why you’d be so bummed up on this issue. Just looked for $25 pfds w a ytc of 4.6 and b- or better . It’s a very small list. Like 11? I kept running it thinking that must be wrong, right?

If you Prefer—I’m bummed because the issue is junk rated–and my own expectations (obviously too high) of maybe 5.25%–plus I am ‘talking my book’, but you are correct on a ytc basis there isn’t much to choose from. ‘This too shall pass’.

Tim – Talked to a High-Yield manager today who was making the case that high-yield is STILL CHEAP. At a 4.10% credit spread he believes we go to a 3.10% spread, especially with Yellen and Powell willing to backstop any declines. I certainly don’t see much upside at 300-400bp spreads, but some do. Patience continues to be the individuals biggest advantage.

Just because yields might go lower, it doesn’t mean they’re cheap. It just means they might get even more expensive. Considering that European high yield is currently under 3% (https://fred.stlouisfed.org/series/BAMLHE00EHYIEY), it wouldn’t be a shock to see U.S. yields go lower. But is that a good compensation for the credit risk? The yields will blow out again during the next crisis – why not just stay conservative and wait for that opportunity to buy? You’re not missing a lot during the interim.

Karma I totally agree, patience is our friend.