As I have mentioned too many times I have been carefully reviewing our holdings and trying to find the best balance of safety and yield–so many options all dependent on each individual investor. It has NOT been helpful that politics has become such a large part of investing decisions. While politics has always been part of investing it is now on steroids.

Regardless of anything that occurs in politics we as investors have to simply ‘deal with it’.

There are a plethora of both term preferred and baby bonds available from company’s that are collateralized loan obligation (CLO) owning companies–Carlyle Credit Income (CCIF), Eagle Point Credit (ECC), Eagle Point Income (EIC), Eagle Point Institutional (EII), OFS Credit (OCCI), Oxford Lane Capital (OXLC), Oxford Square Capital (OSXQ), Pearl Diver Credit (PDCC), Priority Income Fund (PRIF–unlisted) and Sound Point Meridian (SPMC). Every one of these companies have either term preferreds and/or baby bonds currently outstanding.

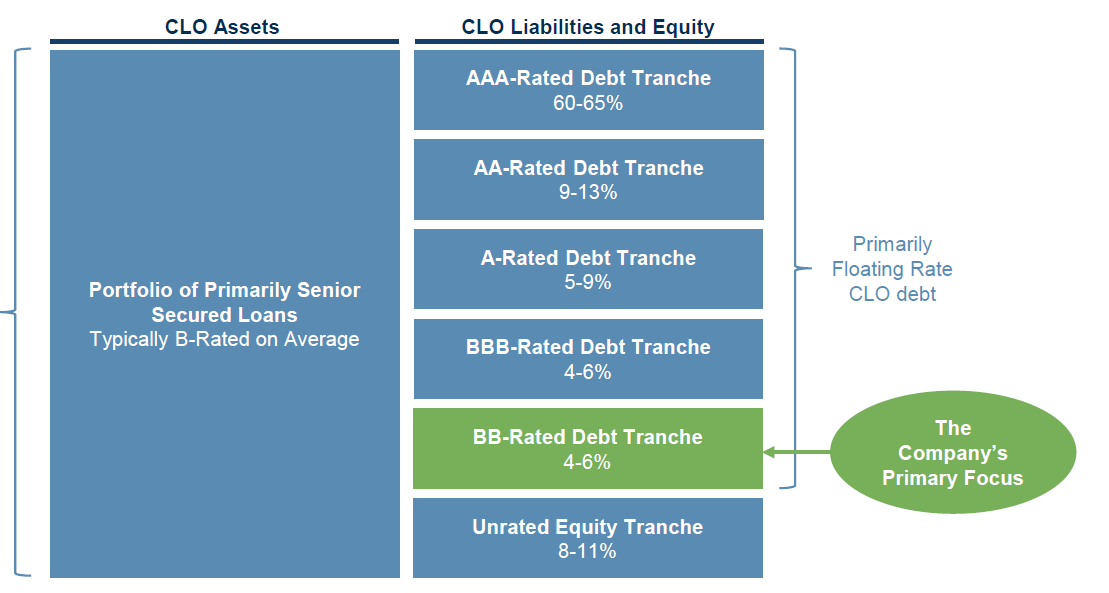

The common theme of all these companies is that they invest most all of their funds in the equity tranches of the CLO—EXCEPT Eagle Point Income (EIC) which invests exactly 75% of their funds in CLO debt. Instantly they climbed above the equity tranche in quality. Their investments are almost all in the BB tranche which is just 1 step above the equity tranche–but it has been a significant difference in the last year as equity issues have fallen substantially in net asset value while debt tranches have fallen much less. It should be noted that EIC took their equity tranche higher a few years ago–at the fund IPO they were 88% in debt tranches.

For instance Eagle Point Income (EIC) has a net asset value of about $13.80 (April 30th) as compared to $15.20 a year ago. Eagle Point Credit Company (ECC) a company holding all equity tranches of CLOs has a net asset value of $6.75 (April 30th) as compared to $9.00/share a year ago. So the EIC net asset value has dropped by 9% over the course of the last year while ECC has dropped a eye popping 25%.

I don’t look at investing in the BB tranche as providing a massive level of safety above the equity tranche–BUT it is safer and EIC has out performed the equity holding companies by a long ways. You can see the difference in quality below–safer, but not the safest certainly.

Now as we look at the term preferreds offered (although many baby bonds are outstanding) by some of these companies we can see that the safest issues (EIC) are yielding the highest current yields (at least in 2 of the 3 issues)–in my mind EICB and EICC are the best current buys. I am looking at it as the best current yield with the best quality investments–NOT by yield to maturity. If one was to look at the yield to maturity of each of these issues you would see that many times the EIC issues have the lowest yield to maturity–BUT just by a tiny bit.

So it comes down to do you want the best current yield with the highest level of safety (in CLO company’s) or are you willing to take on a bit more risk for a tiny bit of reward?

As I review my current holdings I am way (I mean way) overweight in the CLO equity section—but my risk tolerance is really much lower than the way I am positioned.

Since I want maximum safety with minimal volatility – but at the same time I want high yield I will be doing some portfolio rearranging this coming week in our CEF CLO sector–not a total wholesale change, but certainly a rebalancing so my investments reflect my risk tolerance.

Above I am not implying that holdings in any of the CLO companys are bad investments–or that any company is in trouble. Simply I am looking at them in the light of what best reflects my personal risk/reward situation. As long as the asset coverage ratio remains strong and the company has the ability to sell common shares continually preferreds and baby bonds remain safe.

EIC cuts dividend from .20 to .13 if I am reading correctly.

link?

Yep. I was going to buy this yesterday but got suspicious when they announced results to be reported 05/28. They have usually reported around the 12th. Link: https://finance.yahoo.com/news/eagle-point-income-company-inc-120000338.html. Hope you didn’t buy too much, Tim.

Seems to be an over reaction as EIC is now trading at a discount and still has a cushion to support the preferred shares.

Randy, Holding about 3% of several EIC baby bonds. Wonder about the lag time when Thomas P. Majewski talks about deploying funds at discounted prices 1st qtr. At the time we were seeing a decline in rates and now expectations are for higher rates for longer. He talks about how markets are recovering, yes recovering after the April swoon to basically where markets were at before. Now I wonder where we will go from here?

RandyK–I never touch the common shares–only preferreds and a dividend cut is great in my opinion.

furcal—good for them. Most of these CLO common shares just keep paying too high of a dividend regardless of whether they cover them.

Delete

I sold all my exposure to bank loans earlier this year and staying away. IMO the debt and preferred stock of these companies can’t be less risky than the underlying holdings (which are very risky) and you can get similiar yields with much better underlying businesses.

ECC is the canary. Just about the riskiest part of the whole leveraged loan/PE/BDC/CLO space.

I am seeing people here thinking along the same lines I have been thinking. Instead of buying individual BDC’s and CEF’s going with ETF’s to spread the risk round.

I have never used options and don’t intend to start learning how to play that game at my age. But maybe finding an ETF to buy as insurance against a market fall?

One thing to look at is the size and AUM ( assets under management) of some of these ETF’s people here have mentioned. Another thing to look at is their charts. JAAA is a respected name and has 20.9 billion AUM but looking at the chart it is a relatively new fund (started in 2020 after the COVID scare and yet in 2022 it cratered and took a long time to recover, I don’t remember 2022 being all that bad but it definitely affected JAAA. It also plunged in the April panic but recovered quicker. Looking at CLOX & CLOZ I see the same thing, both relatively new and both plunged in April but quickly recovered. I also would call them a micro cap ETF with AUM at around 500 million. What could happen in a major market panic?

On a regular panic in the market I have just ridden it out and tried to avoid being invested in higher risk BB and preferred. But what do you do in a major market melt down? What I mean is something that may take years to recover from. Why do I mention this? I just feel the odds have become greater of this happening from what has been going on.

Another person I listen to has suggested WIA and WIP again these are what I call micro ETF’s although they have a longer history than others mentioned here. They also have fallen in market panics so what other insurance can people suggest?

Remember I mentioned I had talked to a younger duo of asset managers who offered something similar by spreading out the risk over say 10 ETF’s with several being leveraged defensive. My unease at the time was due to similar questions about size of the AUM and longevity of them.

I have to assume in a major market panic these smaller ETF’s may have to liquidate even if set up to protect against such an event.

There is also CLOX and CLOZ.

https://cloxfund.com/

https://clozfund.com/

https://www.youtube.com/watch?v=I0kvufnFwvo

We throw the word “safety” around without defining it. I’m pretty sure it means different things to different investors.

There is a lot of common distribution to cut. And they buyback under nav.

default risk isn’t the only risk by a long shot.

lots of interest rate and spread risk …. I bought 10k worth of oxlc at 4.4 and sold at near five for a laugh. might buy it again … (20% distro is all the nav destruction … i.e. total return is nada, but its fun to trade it).

Good point jb.

Looking at the preferred is just part of the picture, you also need to look at the common. OXLC has such a low stock value what is the risk it will have trouble selling more common and then it still has to be able to invest the money to generate income to feed all the extra hungry mouths it created? EIC has a little more room to maneuver with a 14.40 common stock price.

My personal issue is I don’t want more concentration in just one or two names.

Could be Tim is on an impossible mission to have yield and protect capital. Trying to do both might increase the risk. Kinda like owning your cake and getting to enjoy eating it but then you don’t have the cake.

An early recording of the phrase is in a letter on 14 March 1538 from Thomas, Duke of Norfolk, to Thomas Cromwell, as “a man can not have his cake and eat his cake”

Maybe a safer medium is to take less yield and greater safety. What sectors come to mind?

cef wrapper helps. share price craters, nav does whatever. no redemptions need be paid, just a wonky premium/discount. distro in hands of management. management can absorb small share price fund into other fund when they wish.

the pffa fund manager did an interview, said he found that facts that preferreds plummet and swoon reassuring…the volatility justifies the excess return… they’re pretty well incentivized to keep paying.

How much extra safety do you think that the CEF structure of PRIF provides? Unlike EIC it invests primarily in CLO equity, but historically CEF preferreds have a really impressive no-default record.

My calculations have EICC at 7.94% YTM and PRIF-J at 8.87% YTM, both assuming the same 6% reinvestment rate. I’d probably give the slight edge to PRIF-J at this difference, but I wonder what other people think.

Nathan,

I’ve really tried to figure out the answer to this question…. what is the value of the 40 Act protections. I’ve seen a couple people talk about this, including one manager that specializes in buying this specific type of asset, but can’t find a published study with hard data. However, I’ve heard these people say that no 40 Act paper holder has ever lost money and I’ve not been able to prove that wrong. There has been at least one default, but the preferred holders didn’t lose principal. There have been many equity holders that have suffered losses. I would seriously love for someone to be able to prove me wrong because I want the data.

With all that said, I am significantly overweight the EIC preferreds (nearly 8% position) and they’re the largest position in my portfolio by far. 8% is a historically “equity like” return and I believe I am taking substantially less risk. Feels like I’m getting paid single B return for AA risk.

Case in point… EIC lowered the dividend for the common for Q3. Good move on their part… but the common will get killed today and I’m smiling because it makes my investment more secure.

Have you considered a 70/30 blend of JAAA (or PAAA) & JBBB as a portfolio holding/position?

Quite a moniker. From Brain Damage (Pink Floyd’s Dark Side of the Moon)

I was thinking along a similar line- that adding JAAA & / or JBBB while lowering the divs, using some portion could lower some of the ‘risk’.

JAAA is rather quiet about their tranche(s), but they do mention that the portfolio is Debt: 394 (positions).