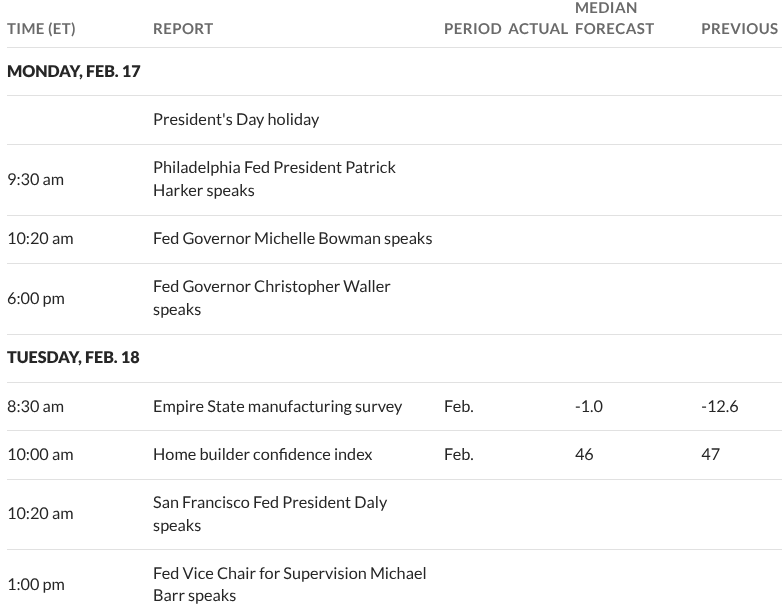

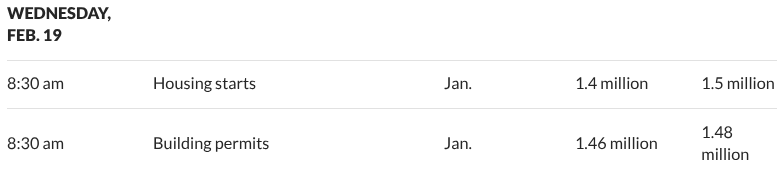

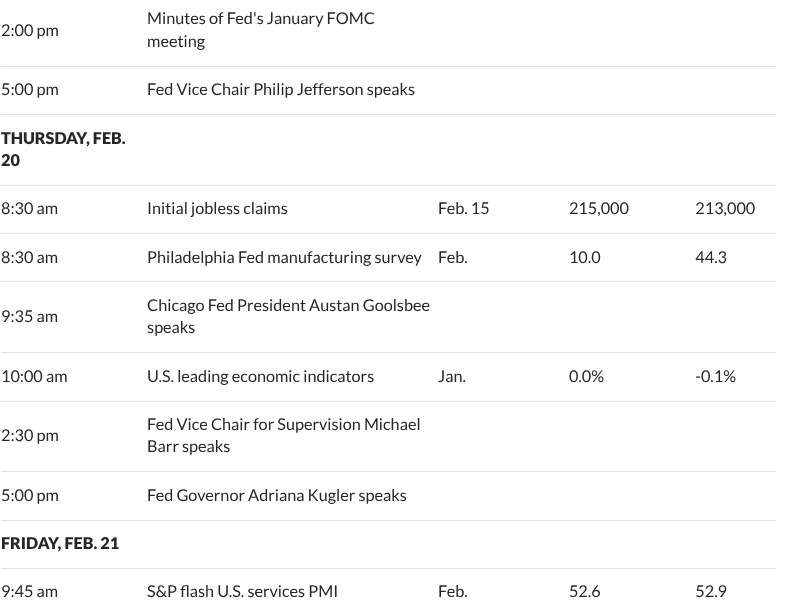

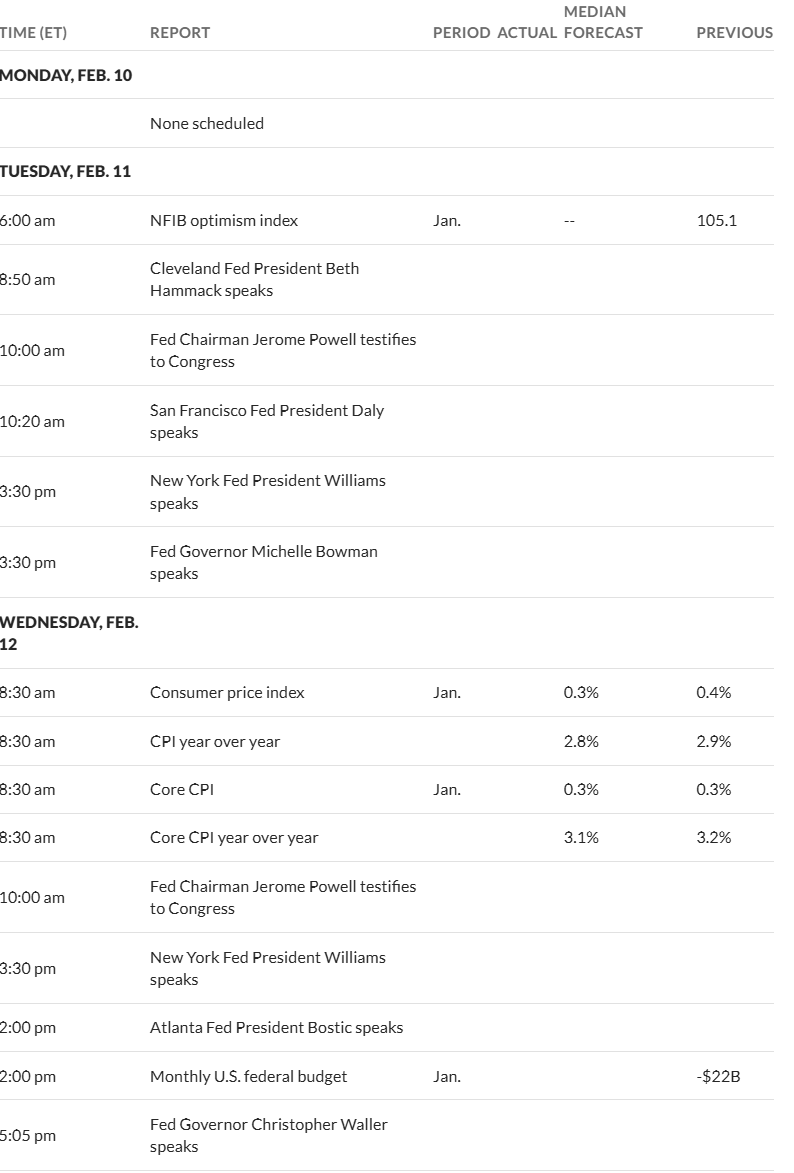

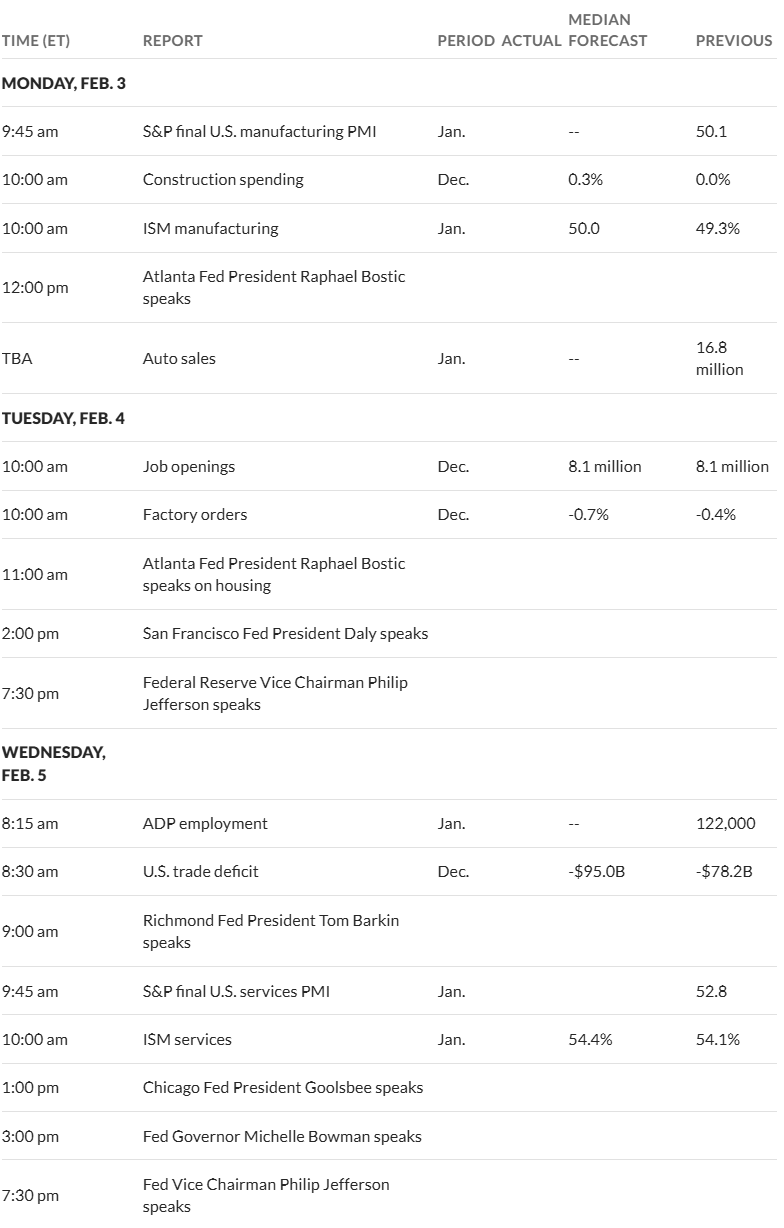

Here we go again—it could be a relatively quiet week, although we do have FOMC minutes being released on Wednesday and this can always set off fireworks-one never knows.

The S&P500 moved higher last week by 3/4% and now just a tiny amount below a record level. This week is starting off looking some higher, but the future market gains can evaporate quickly.

The 10 year Treasury closed last week at 4.47% (down 2 basis points from the previous Friday). At this moment (5:30 central) the 10 year is at 4.52%–up 5 basis points. As noted the economic news is somewhat light this week, but we don’t know what kind of curve balls that the new administration will throw at the market. My thoughts are that the 10 year will continue in the relatively modest range until we get to next week when we have the PCE being released–we’ll see which way rates get pushed.

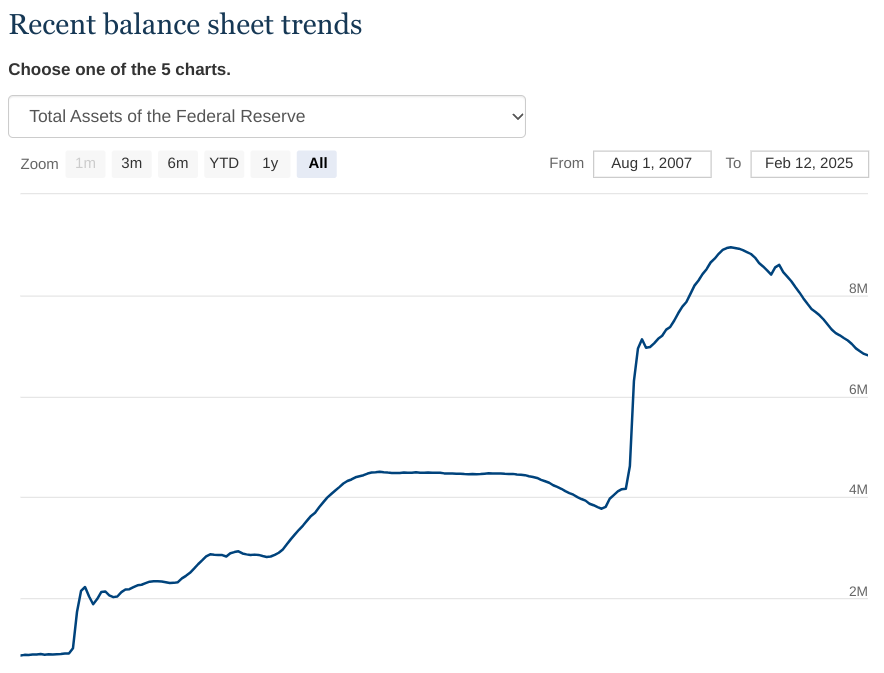

The Fed balance sheet grew by $3 billion last week–a rare increase which will be offset by falls in the weeks ahead no doubt. The chart of the balance sheet levels is an interesting chart–falling back front the highs quite dramatically.

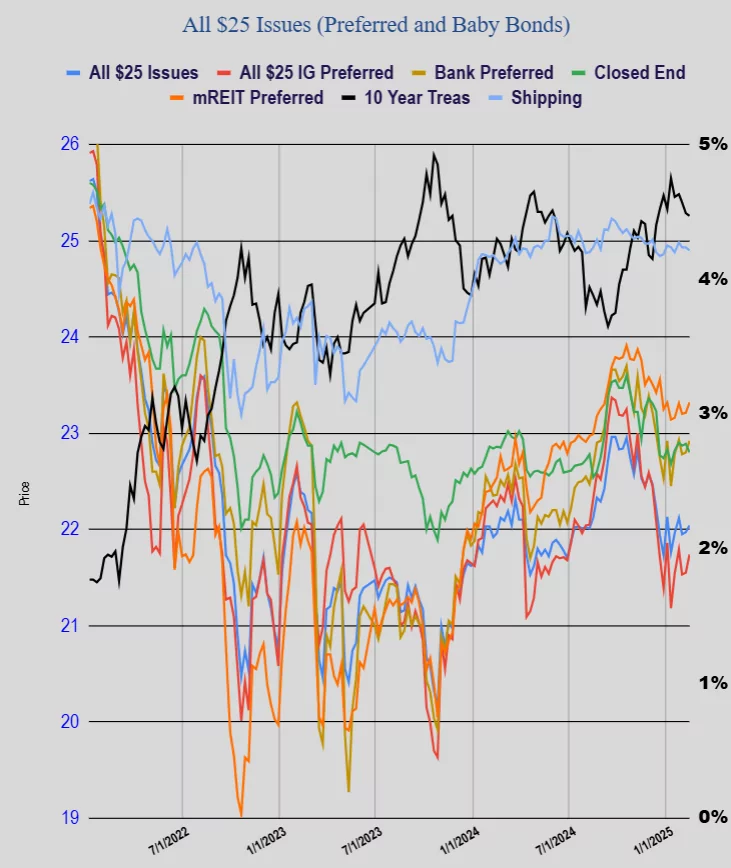

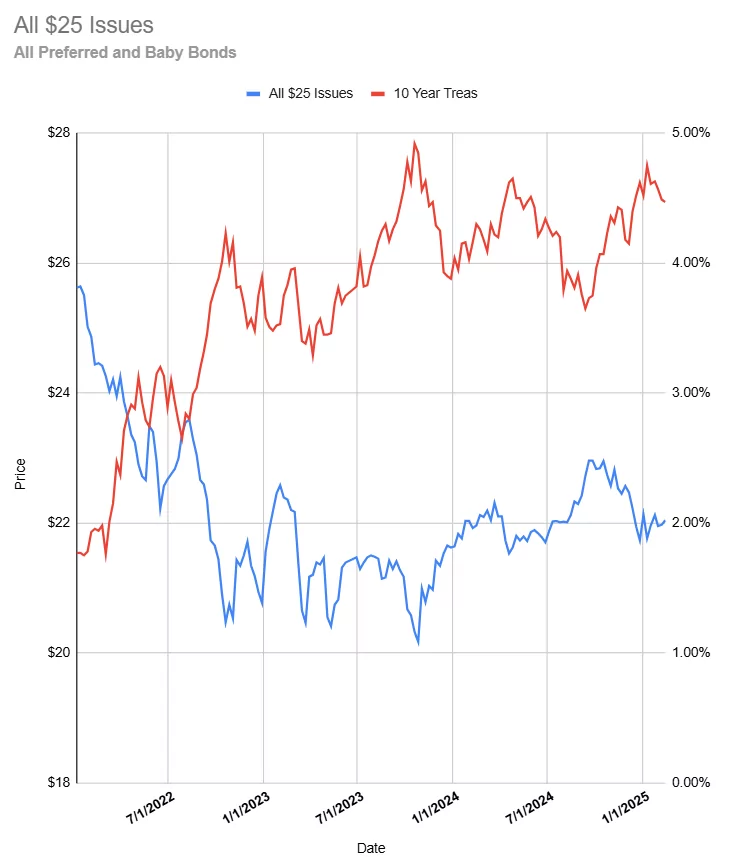

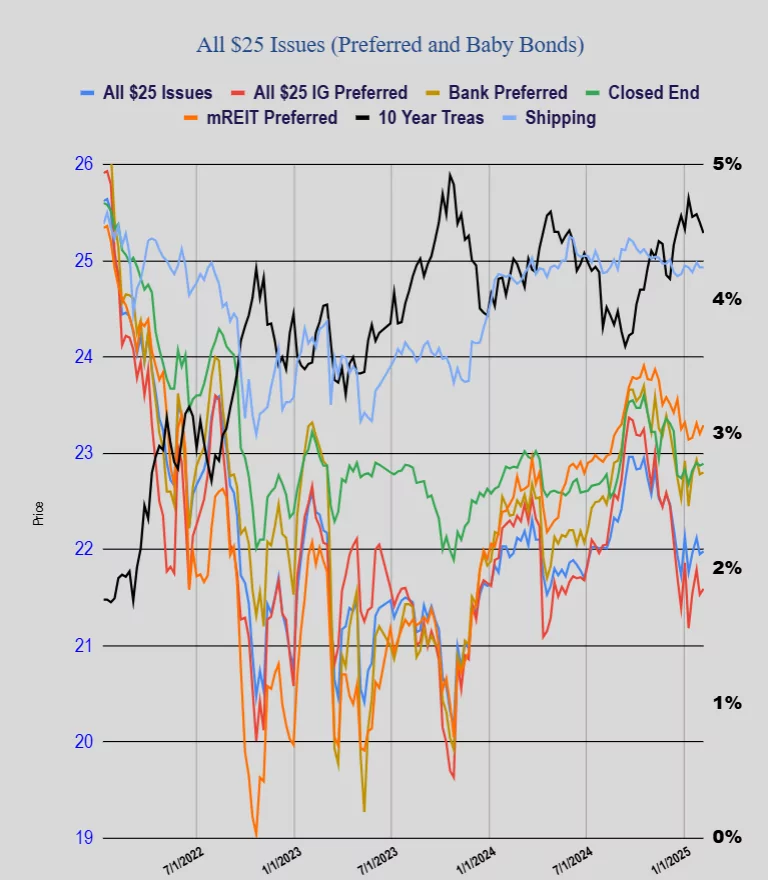

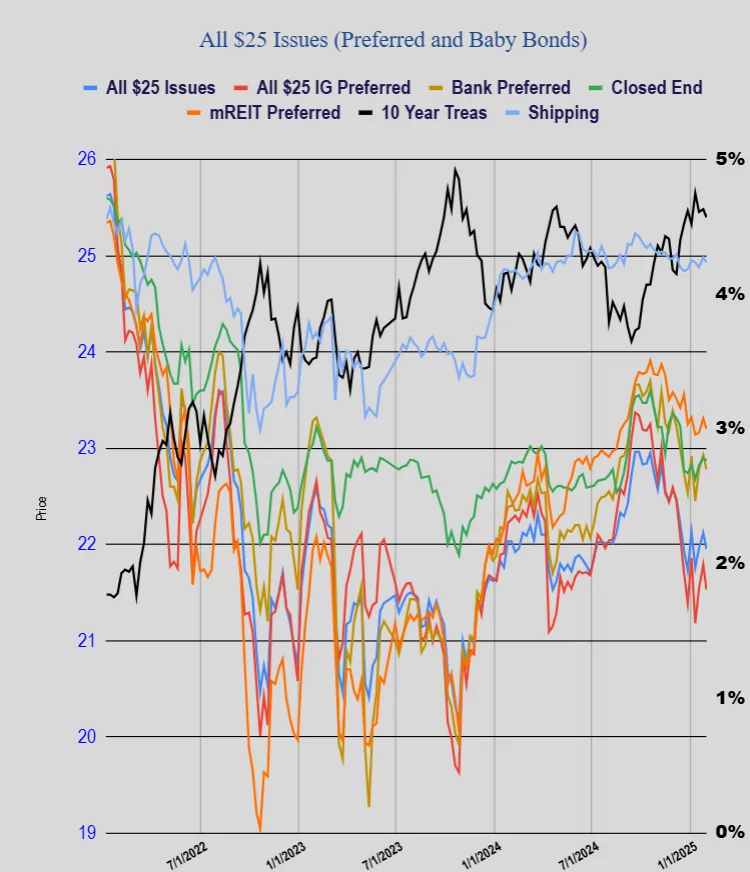

The average $25 preferred and baby bond rose by 7 cents. Investment grade issues moved 15 cents higher with banks up a dime, mREIT issues up 6 cents and shippers continue to hover around the $25 area and down 3 cents.

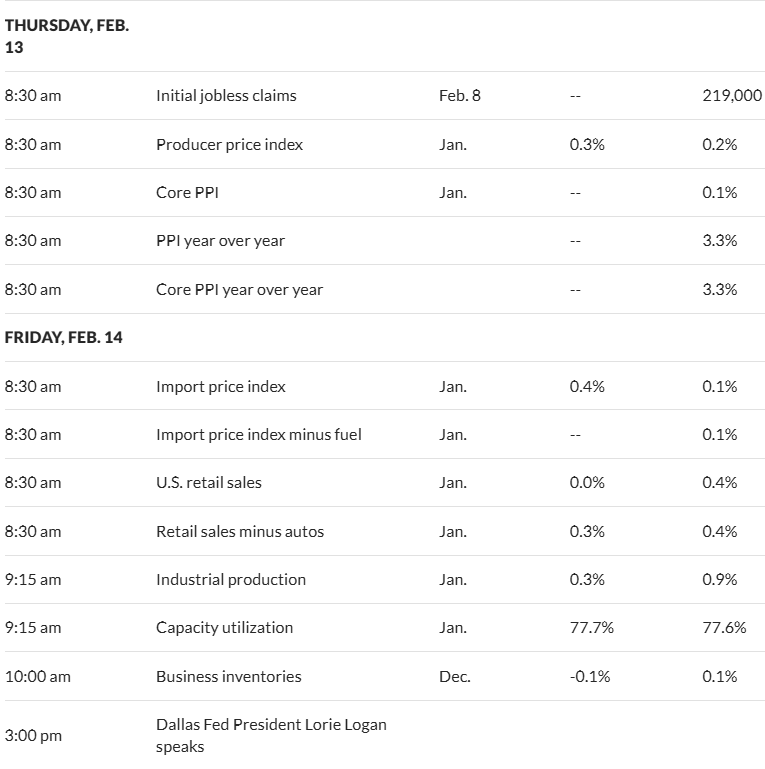

Well we almost certainly have another exciting week to look forward to –up or down who knows, but likely in both directions. Last week the S&P500 moved up just 1/2%, but moved in about a 2% range. This week we have the consumer price index (CPI) and the producer price index (PPI) being released on Wednesday and Thursday respectively and additionally we have Powell testifying before the senate and house on Tuesday and Wednesday. Lots of excitement will be created.

The 10 year Treasury yield closed the week 4.49% which was down 8 basis points on the week. The yield moved in a range of 4.41% to 4.60% for the week. Economic data continues to push rates around–most data has been a bit mixed–some better than expected with some worse than expected.

The Fed balance sheet fell by$8 billion last week as the balance sheet runoff continues.

Last week in spite of interest rates falling 8 basis points for preferreds and baby bonds didn’t respond as the average share price fell by 2 cents. Investment grade issues rose 3 cents, banks rose 1 cents, CEF issues rose 2 cents, mREIT issues rose 3 cents.

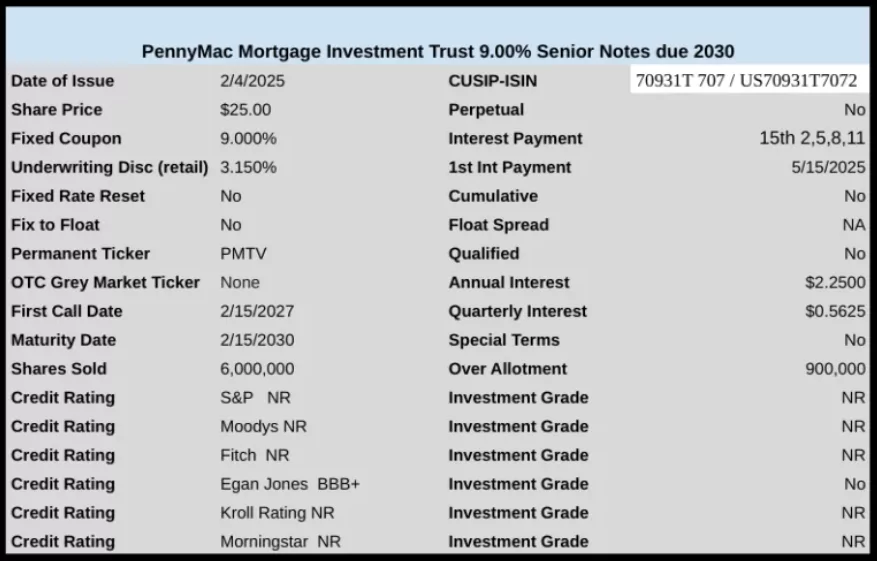

We had one new income issue launched last week as mREIT PennyMac Mortgage Investment sold a baby bond with a coupon of a tasty 9%.

Well last week was another record breaking week for equities with the S&P500 trading at record highs by 11 a.m. Friday–then the selloff began which sent the index down almost 2% where it closed. For the week the index ended up down 1% from the previous Friday–Monday was a wild ride for tech stocks as AI indigestion hit–but unless you owned the tech issues you probably did ok.

The 10 year treasury yield ended up down about 5 basis points from the previous Friday close. The yield was trading right down in the 4.50% area until midday and a serious realization of the ‘tariff’ issue and then rates headed higher closing the day at 4.57%. There was economic news during the week (GDP, FOMC rate news etc) which were not huge factors as the news generally met forecast.

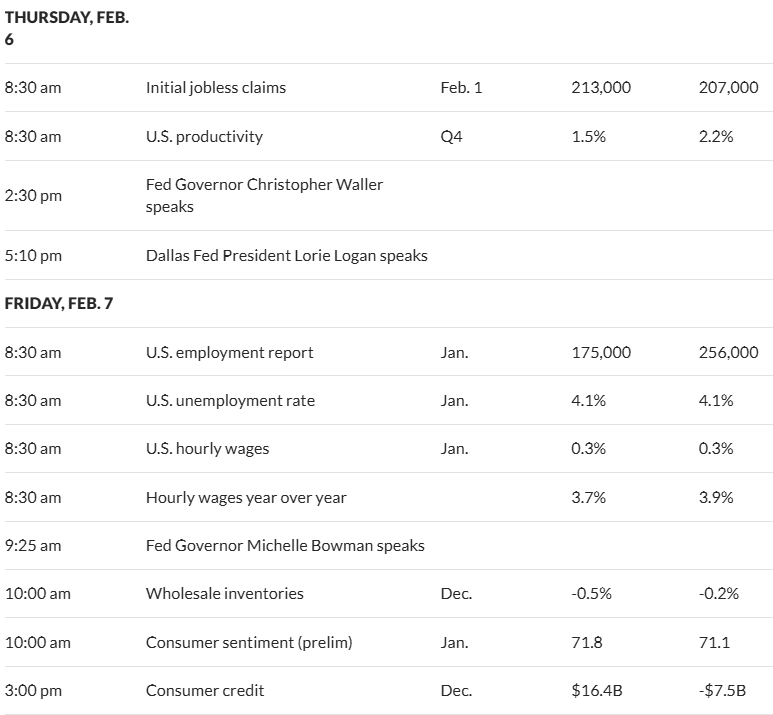

This week the economic news is generally mild until we get to Friday when we have the December employment news being released.

The Federal reserve balances sheet fell by $14 billion last week–continuing as expected as the Fed has not changed their policies on balance sheet runoff.

Last week, in spite of interest rates falling on the week the down draft Friday afternoon sent prices down, The average $25/share preferred and baby bond fell by 17 cents. Investment grade issues fell 26 cents, banks were off 15 cents, mREITs fell 11 cents and shippers were off a nickel.

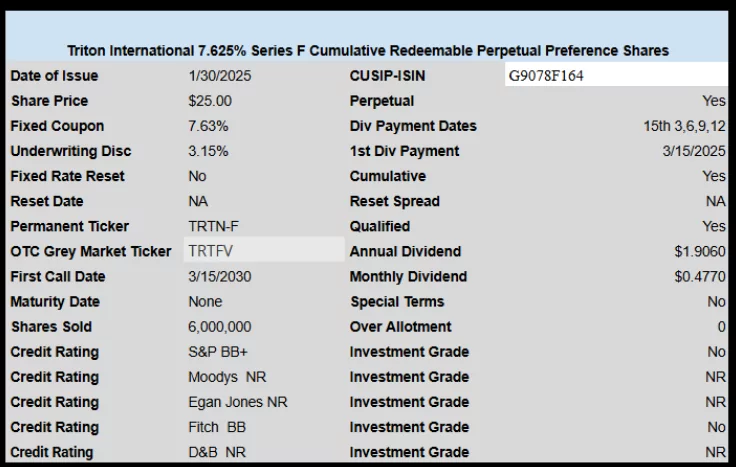

There was one new issue priced last week as Triton International priced a new perpetual preferred with a coupon of 7.625%. The container leasing company has 5 other outstanding preferred issues.

One can’t really predict with any level of certainty to whether equity markets are going to move into a ‘melt up’ with all the cash that continues to be available in fixed income–OR whether markets will ‘melt down’ as folks decide it is time to bail out and move MORE to money market funds. I see everyone and their dog on CNBC, Fox Business and Seeking Alpha have an opinion as to which way markets will move. NONE of them know squat–but likely maybe 1/2 will be correct. Does that mean I know? Of course not, but I just say ‘I have no earthly idea’. I have no newletters to ‘push’ or special ‘morning calls’ to sell—everyone of these folks is ‘talking their book’. Very honestly these ‘gurus’ are kind of dangerous to the non thinkers–and I have concluded the number of non thinking investors out there is pretty massive–seems like most folks want to let others do the thinking–then they have someone to blame when their ‘stash’ goes south. I like the thinking of folks on this website–plenty of info to educate oneself and then make your own decision.

Last week the S&P500 moved higher by about 1.7%—not quite a record weekly close, but the close on Thursday was a record high close. There wasn’t really any economic news to push markets higher. Jobless claims were 223,000-about on forecast and historically fairly low–if folks are employed the economy marches on. Existing home sales are pretty quiet–they say the slowest since 1995–obviously the high prices and the somewhat normal mortgage rates (apparently not normal for anyone under 40 who is waiting for 3% to return) have stymied most folks. 2 high income families and old folks with cash in their pockets can do what they want–but that leaves a lot of folks on the sideline.

The 10 year treasury closed the week at 4.63% which was 2-3 basis points up on the week. Without consequential news movements were minimal. This week we do have economic news of meaning. We have the federal open market commitee (FOMC) meeting starting on Tuesday afternoon–then the ‘announcement’ and Jay Powell presser on Wednesday afternoon. Prior to the interest rate decision we have the advance estimate of GDP for Q4 on Wednesday morning. Lastly we have inflation numbers from the personal consumption expenditures (PCE) on Friday. If all that news doesn’t cause some market movements I would be surprised.

So are rates going up or down–or staying the same. For now I think they remain unchanged. There is no labor stress and inflation is kind of flattish–not at target yet–but just treading water. Almost without doubt Jay Powell wants to see more data.

The Federal Reserved Balance Sheet fell by a piddly $3 billion last week–now the balance is $6.832 trillion. Already the Fed has run off more of the balance sheet that I thought they could accomplish–the high point was right around $9 trillion. Certainly sometime in the next couple of years we will need to utilize the balance sheet for quantitative easing–so at least we have built a $2 trillion buffer (as compared to the high) of buying power.

Last week the average $25/share preferred and baby bond bounced back a bit. The overall average share was up 16 cents with investment grade issues moving 25 cents higher, banks up 18 cents with CEF preferreds up 8 cents and mREIT preferreds up 15 cents. All in all not a big up week, but at this stage anything green is good.

Last week we had stocks move back into ‘party’ mode as the S&P500 moved higher by a giant sizes 2.9%. This appears to be related to the CPI and PPI info which came in slightly softer than expected earlier in the week which sent interest rates tumbling.

As mentioned above the yield on the 10 year treasury to a good sized tumble last week falling from 4.78% from the previous Friday all the way down to close at 4.61% on Friday.

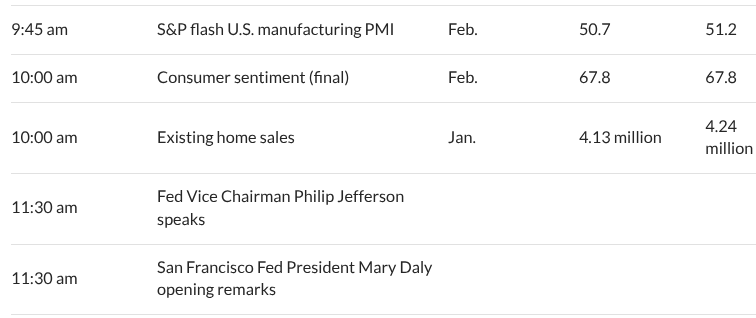

For the coming week economic news is relatively light, and while we could be surprised none of the data should send markets plunging or flying. Of course now have the Trump administration in charge so there is no telling what sort of news could move markets. We had no news released Monday since it was a holiday and there is none scheduled for Tuesday. Leading economic indicators are released Wednesday, but this has been a market mover over the last year or two. Existing home sales and PMI (purchasing managers index) are released on Friday and typically these will not move markets.

The Federal Reserve balance sheet fell by about $20 billion last week.

The average $25/share preferred and/or baby bonds took a jump last week as one would expect given that the 10 year Treasury yield fell substantially during the week.

The average share rose by 20 cents last week, with investment grade issues jumping a huge 36 cents, banking issues jumping 33 cents, CEF preferreds were up 14 cents, mREIT issues were up 2 cents but the shippers fell by 6 cents.

Last week we had 1 new income issue sold–mortgage REIT Redwood Trust (RWT) sold a new issues of senior notes with a coupon of 9.125%. RWT has other notes and preferreds outstanding and these can be seen here. It is always best to check outstanding issues because there may be outstanding issues that are superior in some regard (i.e. yield to maturity etc).