Tex the 2nd posted some comments last week that made me think about how the ‘buy and hold’ person (of purely preferreds and baby bonds) would have faired over the course of the last 2 years. This would have been through the Fed interest rate hiking cycle.

We know that there are many factors that go into portfolio performance. Those that held lots of short maturity baby bonds or term preferreds would have seen less of a drawdown in capital than the ‘average’ $25 issue. Those that lightened up on preferreds and baby bonds as rate hikes began and moved to cash equivalents would of seen less downward pressure than the ‘average’. And of course folks hold diversified portfolios–i.e common stocks. Just lots of factors.

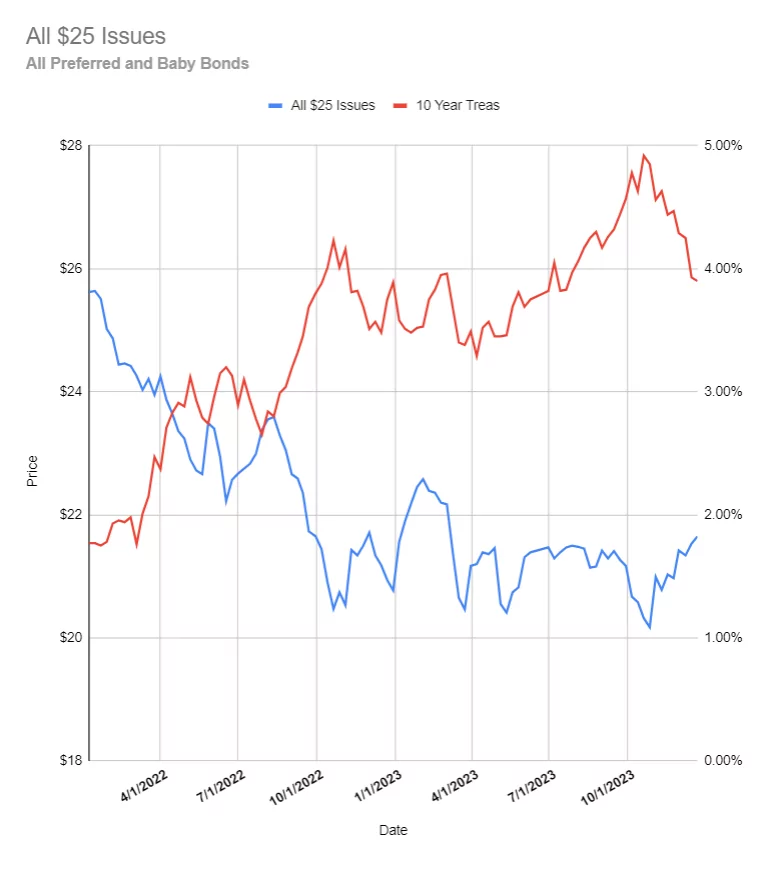

The chart below shows the ‘average’ $25/share issue (preferred and baby bond) price over the last 2 years. Obviously some issues have been called and new ones issued which would affect the averages–but all in all I don’t think these factors have been major factors to the big average.

I believe that most folks here — at least those that have been active on the messages boards have soundly trounced the ‘average’ issue since many of us are at or moving nicely above portfolio all time highs. Note that the ‘average’ price shown above does not account for any dividends or interest paid thus performance would have been better than depicted.

I know the 10 year treasury doesn’t track with local short term rates but local banks are still pushing 5.2-5.6% CD’s for up to 2 years.

I agree, Tim. My guess is that true bogleheads don’t visit this site much. Nothing wrong with buying and holding, just lots of inefficiencies to exploit if a name gets too cheap or expensive. IMO, much easier to do this with preferreds ( vs. common) given the high dividend and capped upside.

Thanks Tim. The chartist in me sees a $1-2 (5-10%) capital gain if/when the 10yr moves to around 3% (just -90 basis points) all while collecting div/int payments. This works for my purposes of collecting steady, mostly-safe income. There are still some deals to be had – I just picked up MGRB @ $18.40 for a 6.46% yield.

JoshM–exactly what I see. A 10-12% potential year (of course a year is a long, long time

I have bene wondering if an III Index would be worth creating and tracking.

August – I have pondered such a thing myself–maybe I can eventually figure something out.

Tim, that will be a toughie as you have to build in your bias’s to make an index. As term dated, 5 year newly issued 8% BDC bonds with 2 year call dates, love floaters, call anchored fixed, newly issued fixed, etc. etc. will tend to trade in different manners based on market volatility, yield credit spreads, and long end movement.

Of course you could just make a BS index fund like most do just based on market cap and new issuances.

Grid–yes I am very hesitant to get into something that is ongoing–takes a lot of maintenance and time. I could build something totally to the way I invest – anything else would be a BS index.

Tim, if my personal preferreds mirrored an actual preferred index, you would certainly get a kick out of that one.

Grid–no doubt the “Grid Fund’ would be a fun read.