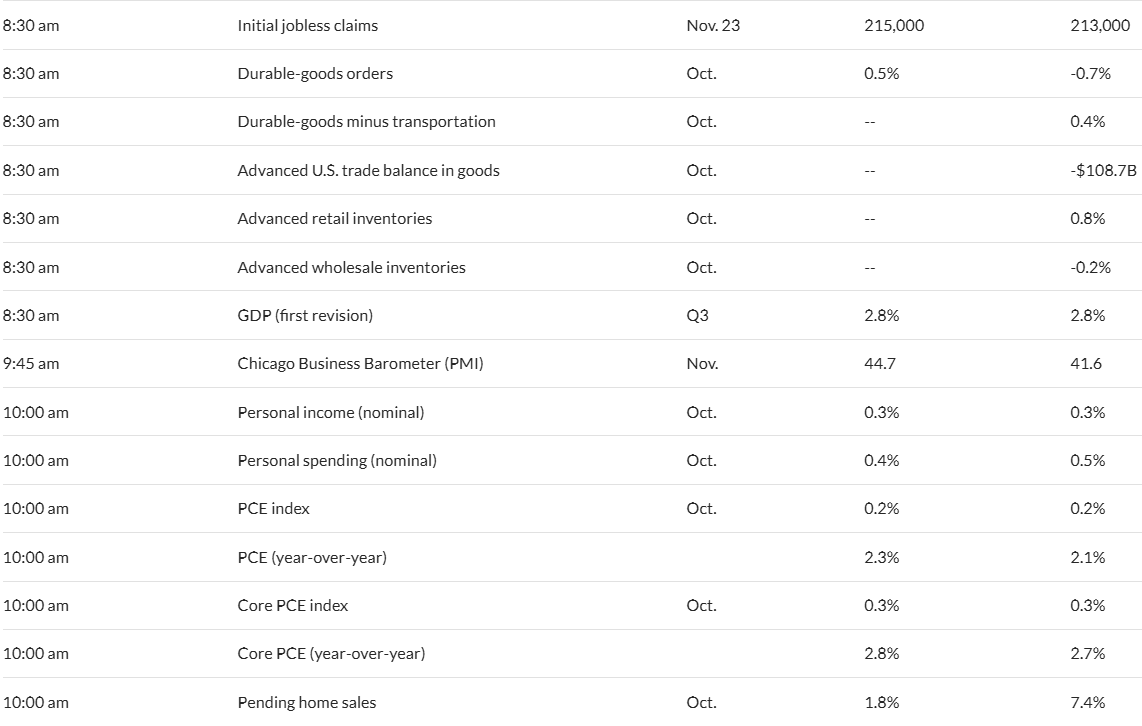

We have lots of economic data being released today with the big news on inflation being released at 9 a.m. (central) within the personal consumption expenditures (PCE) report. But we also have lots of more minor news pieces being released as shown below.

Interest rates have held firm in the 4.27% area after the rally on Monday so for now it appears the upside pressure on rates has been lessened. We will see what the future holds–the Treasury still has to sell mounds of debt–but maybe less than originally forecast. The bigger question is whether we move closer to recession–or fall into a recession. Cuts in government spending will have consequences–what they will be or more importantly the timing of the cuts are less certain. It should be an interesting year ahead.

Yesterday I did double up my position in the Priority Income Fund 6% term preferred (PRIF-H). As I wrote yesterday (and we all know) making a buy or sell with relatively illiquid shares can be a challenge and while I hoped to pay around $24.10 I ended up with an average price of $24.20. The yield to maturity still remains favorable in the 8% (+/-) area.

Yesterday I updated my laundry list of holdings with the sector weightings of holdings. It’s all about CEF preferreds and insurance issues at 29% and 20% respectively. While I would would prefer to have a more balanced sector portfolio it isn’t going to happen right now-maybe in the future other sectors will present some bargains–but that time isn’t now.