Below are press releases from companies with preferred stock and baby bonds outstanding. Additionally, news of a more macro economic importance may be posted.

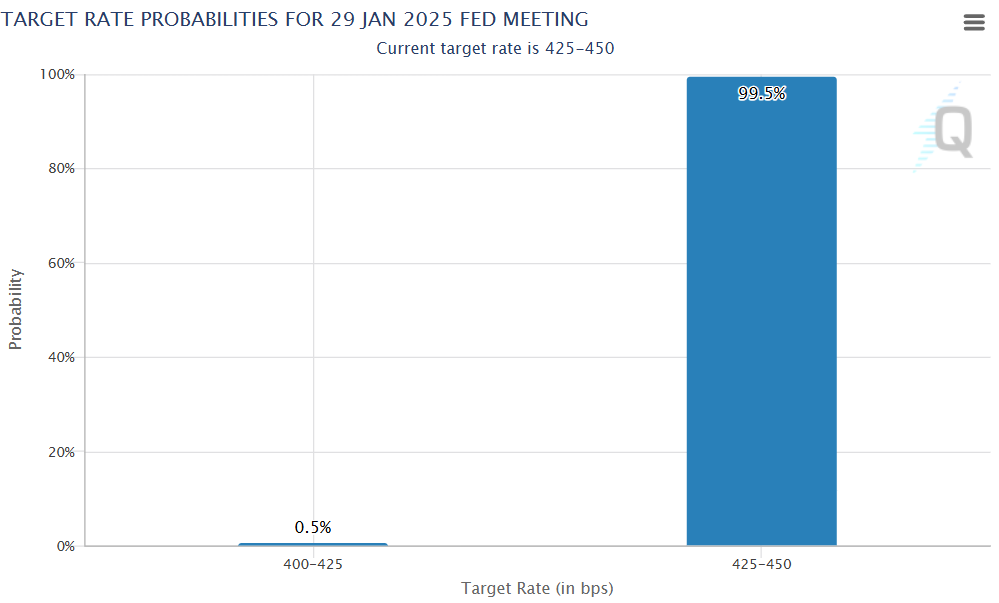

Markets are pretty quiet waiting on the FOMC to make their 1 p.m. (central) announcement on interest rates. Of course there is no doubt in anyone’s mind that the announcement will be NO CHANGE. The CME FedWatch tool shows the probability to be 99.5% for no change. Any deviation from this would set markets ablaze (one way or another)

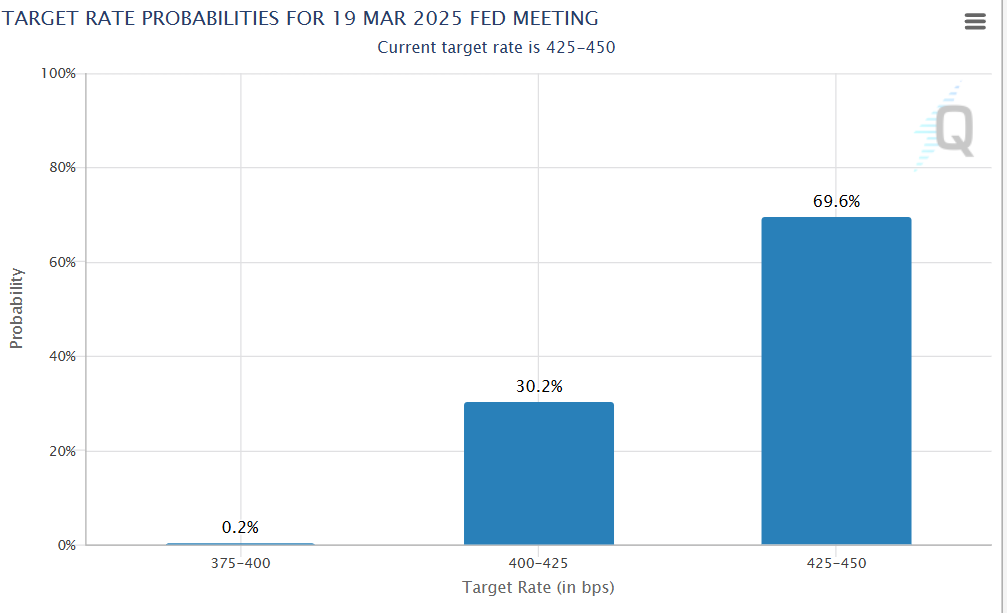

Even the current odds for a pause at the March meeting is 69.6%–of course the amount of data that will be released before this meeting is substantial so these odds will swing a bunch before the meeting.

We will get a decent read on how the economy is functioned tomorrow when the advanced read on GDP for the 1st quarter will be released–of course the number will be revised twice after that reading so honestly tomorrow is just a best guess.

Yesterday I did unload the lions share of my preferreds in Brighthouse Financial (BHF) (details on the ‘laundry list page). I booked losses of capital on both issues I held, but it has almost always been my policy to exit issues with even a small chance of any delisting and with the company planning to sell themselves I don’t want to hang around. This is NOT because I would expect an affect on dividend payments, but instead is because of the high probability of loss of capital in the share price.

The last time I had a similar situation was with Enstar (ESGR) , which announced they were being sold to Sixth Street–an alternative asset manager, in July 2024. I exited my shares in the Enstar 7% preferred (ESGRO) at $23.83 on the announcement and shares now trade at $20.65–it could take multiple years to recoup $3/share and I don’t need the stress of the unknown outcome in my life.

Well now it is time to ‘wait’ for 3 hours and see what Jay Powell brings to us.

Below are press releases from companies with preferred stock and baby bonds outstanding. Additionally, news of a more macro economic importance may be posted.

Shares had moved sharply higher in the last week–actually hitting the $27.80 area–were I would have sold, but the move escaped me until today when I finally got out at $26.67–a capital gain of around 4-5% to go along with the juicy dividends I have been collecting.

Nothing wrong with CCIF–just moved too high for a term preferred with mandatory redemption in 2028.

I hope to re-enter shares when they come back to earth—and they most certainly will drop back into the $25’s soon.

As noted by aj in the comments just now Brighthouse Financial (BHF) is looking to sell itself.

I have very modest exposure to 2 preferred issues which I may/may not exit with losses. My concern is a potential delisting of preferred shares–I will need to read the prospectus to see what it has to say on the matter.