The earnings are rolling in this week and while I don’t try to do deep dives on most of them I do pay attention on a macro level—and most of them are pretty damned good. I was surprised, in particular, how strong McDonald’s (MCD) revenue and earnings came out–just from a personal perspective we don’t stop there much anymore, but I guess many don’t agree with our assessment. General Motors (GM) had stellar earnings-Mary Barra has been and is one of the best CEO’s in the country in my opinion. If we are near a recession most company’s didn’t get the message.

First Republic (FRC) is tumbling this morning after their earnings release late yesterday–the banker has plenty of challenges as they lost 40% of their deposits last quarter. It will be many quarters before preferred dividends are paid on their preferred stock issues–if they ever are paid. In recent years it seems that it has become more acceptable to screw preferred holders and being non cumulative will FRC ever feel compelled to pay preferred dividends?

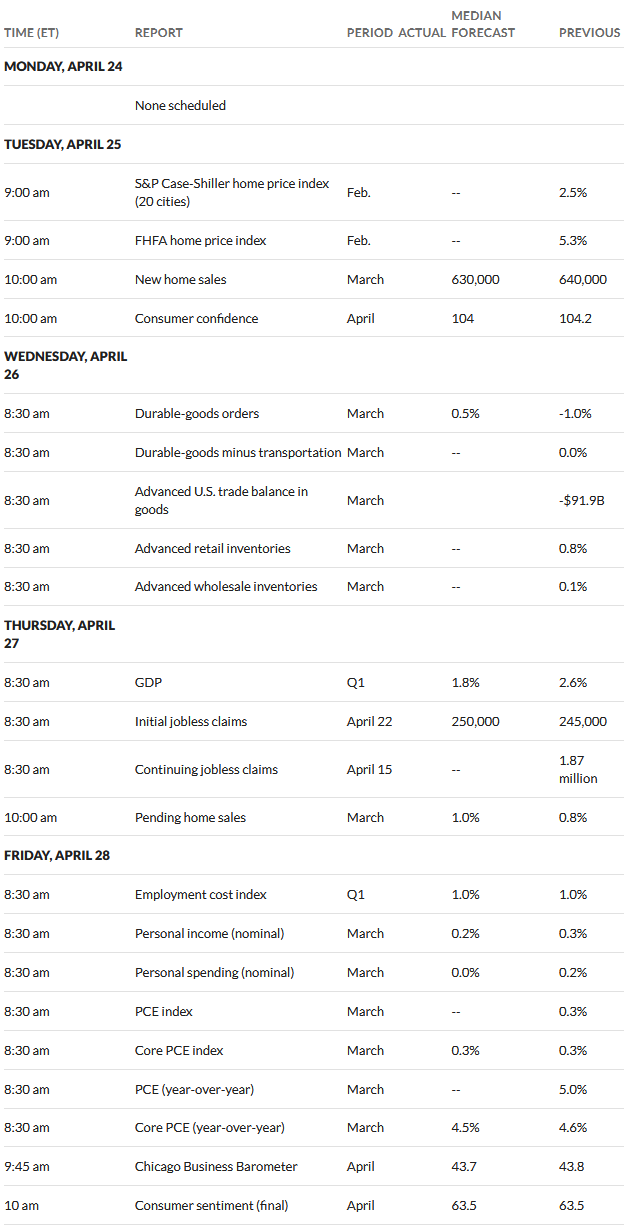

Today we have housing related economic news on tap. We will have the Case Shiller Price Index and FHFA price index both being released at 8 a.m. (central). Then we have new home sales and consumer confidence at 9 a.m. My own observations on the housing market is that everything being built is being sold – no huge subdivisions of unsold properties at this point in time. It will take a substantial jump in unemployment to shut down housing–everyone has a job who wants one.

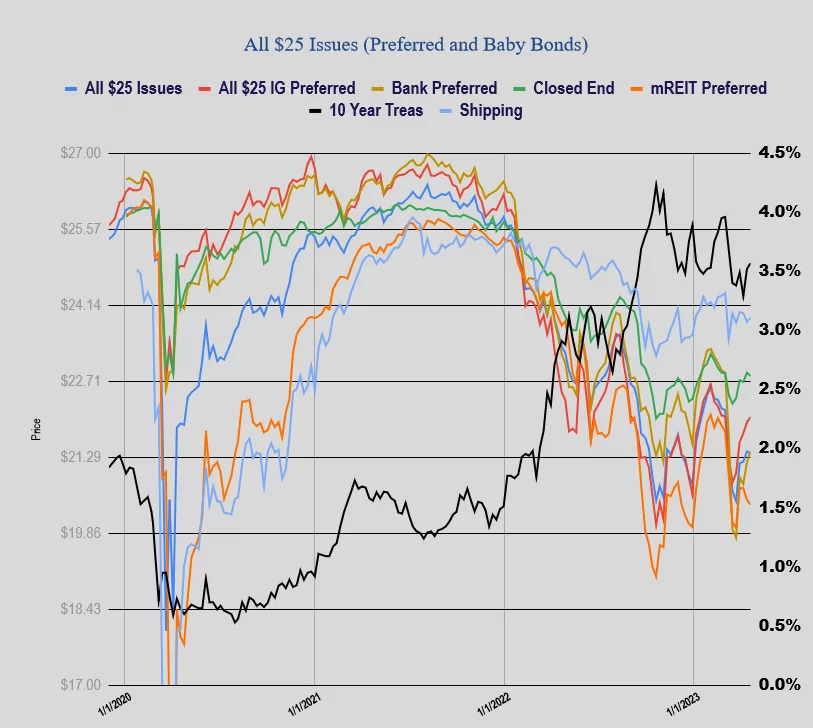

Yesterday, as has become typical for me, I didn’t open my accounts at all – will do that before markets open, but obviously I didn’t buy or sell anything yesterday. Honestly I want to add to my regional bank preferred holdings–great current yields are available in the 7-8% area, but I am resisting at this point in time. As Tex the 2nd reminds us any bank can been seized by the FDIC in an instance–all it takes is a Twitter and Facebook fueled bank run–and I need to wrap my mind around this fact and determine the correct level of commitment to this sector.

Well let’s get this market rolling–yesterday was another day of ‘paint drying’–will today be a day with market movement or will be have another enjoyable day watching paint dry?