The wild ride continues in the equity markets–and will likely continue all through the current week with the tariff uncertainty being front and center. The S&P500 moved higher last week by 5.6%–it didn’t feel like a big up week to me probably because I focus on interest rates which are remaining stuck at fairly high levels.

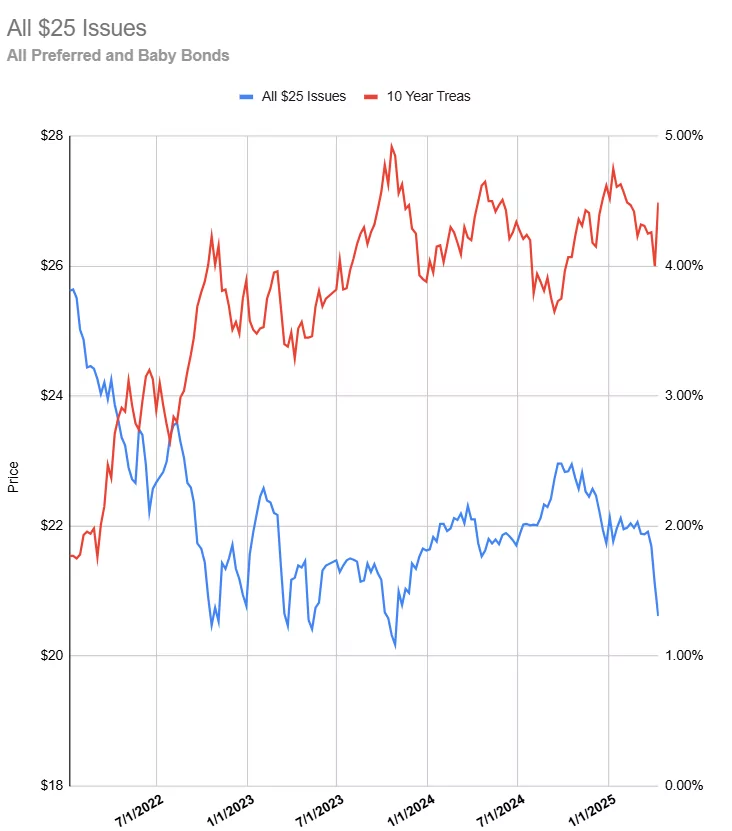

The 10 year Treasury closed the week at 4.49% which was a massive 50 basis points above the 3.98% close from the previous week. We had a number of treasury auctions last week and they all came off fairly good–just maybe at these higher rates there are buyers for our debt. We’ll see what kind of news comes out of the administration on the tariff front and whether we can get interest rates under control. At this moment (Monday 6 am) the 10 year Treasury is trading at 4.44%.

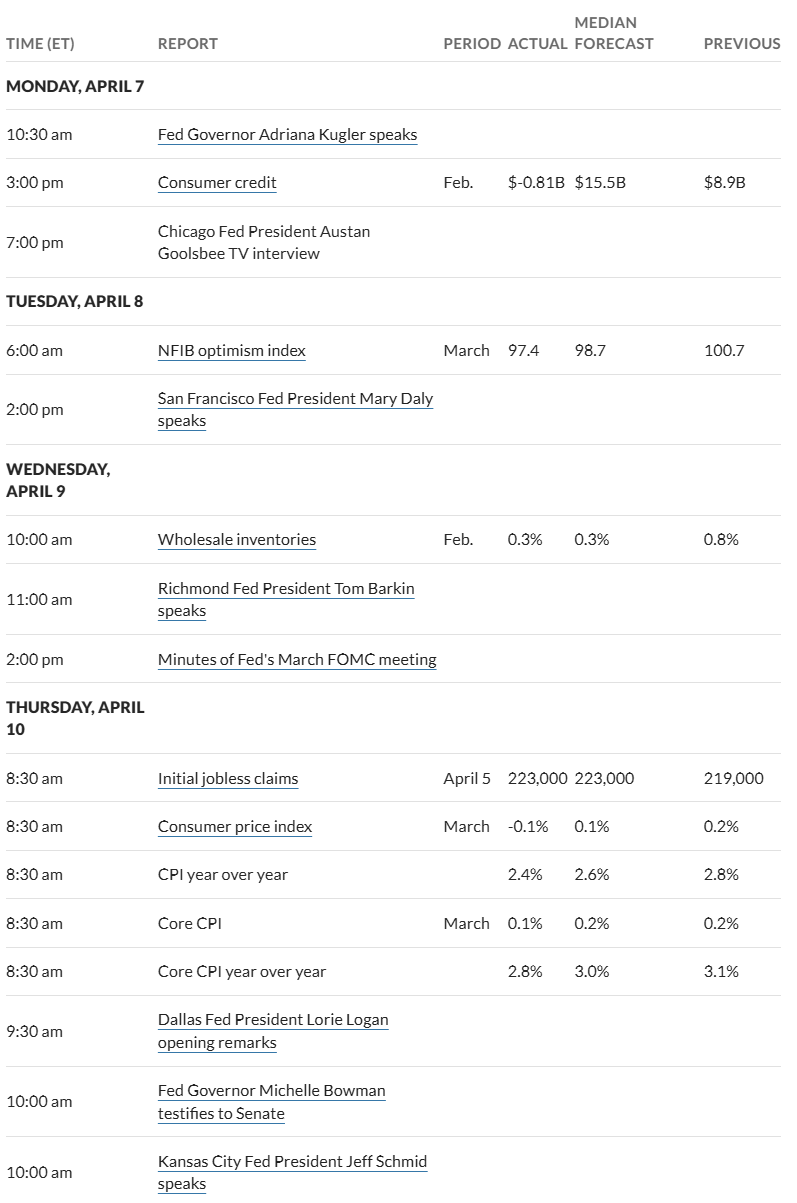

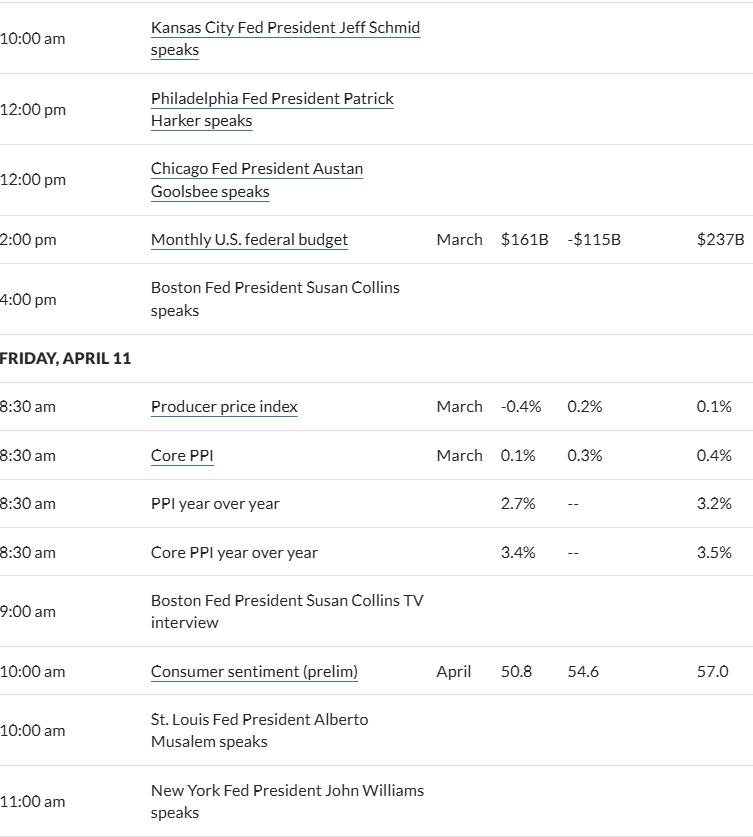

Last week had both consumer prices (CPI) and producer prices (PPI) announced and both came in fairly soft, but neither announcement moved interest rates lower and the numbers were perceived as ‘old news’–before tariffs start hitting.

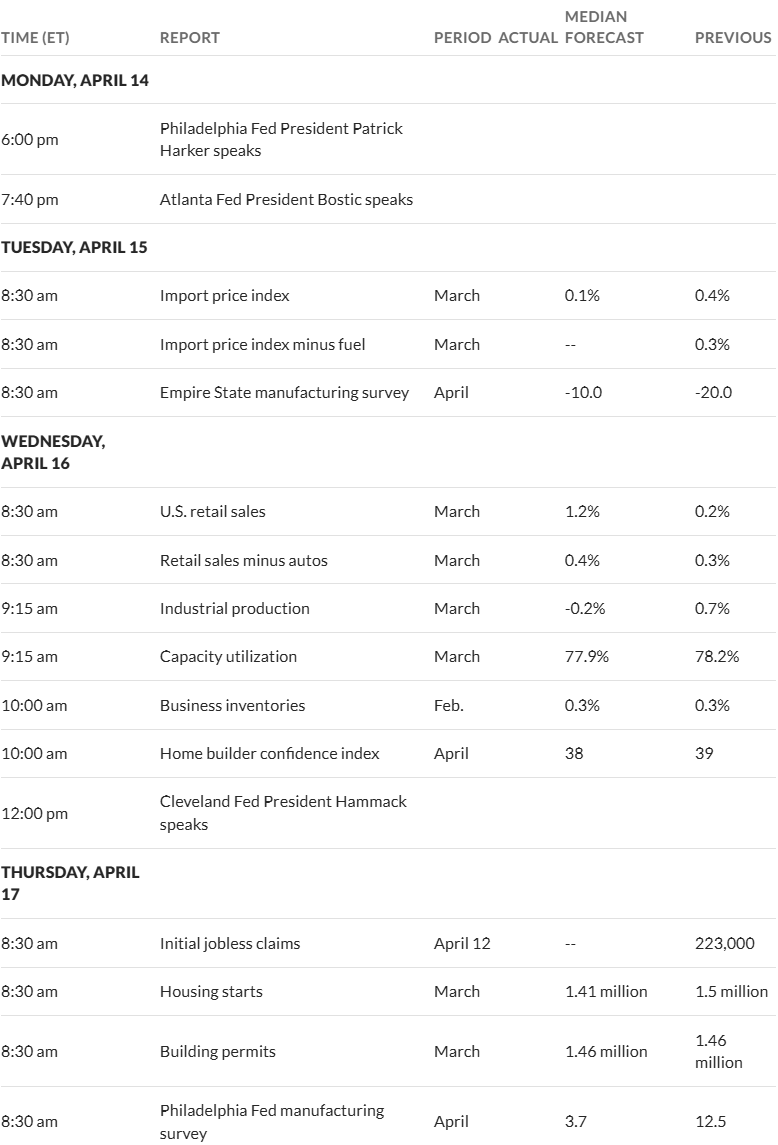

This week we have none of the most important economic news being released, although we have retail sales being announced on Wednesday–but it is old news being from March. Maybe we will see strong sales as folks moved to make purchases ahead of tariffs.

Another item to note is that mortgage interest rates took a large jump last week which without doubt when coupled with consumer sentiment falling will hurt the housing market if these high rates remain in place for long. Housing is one of the most important numbers I watch after inflation and employment as an indicate of future economic health.

The Fed reserve balance sheet rose by $4 billion last week–a bounce that occurs about once a month as the Fed continues to runoff their assets–now at the reduced runoff rate of $40 billion a month– of which $5 billion is treasuries with $35 billion being Mortgage securities.

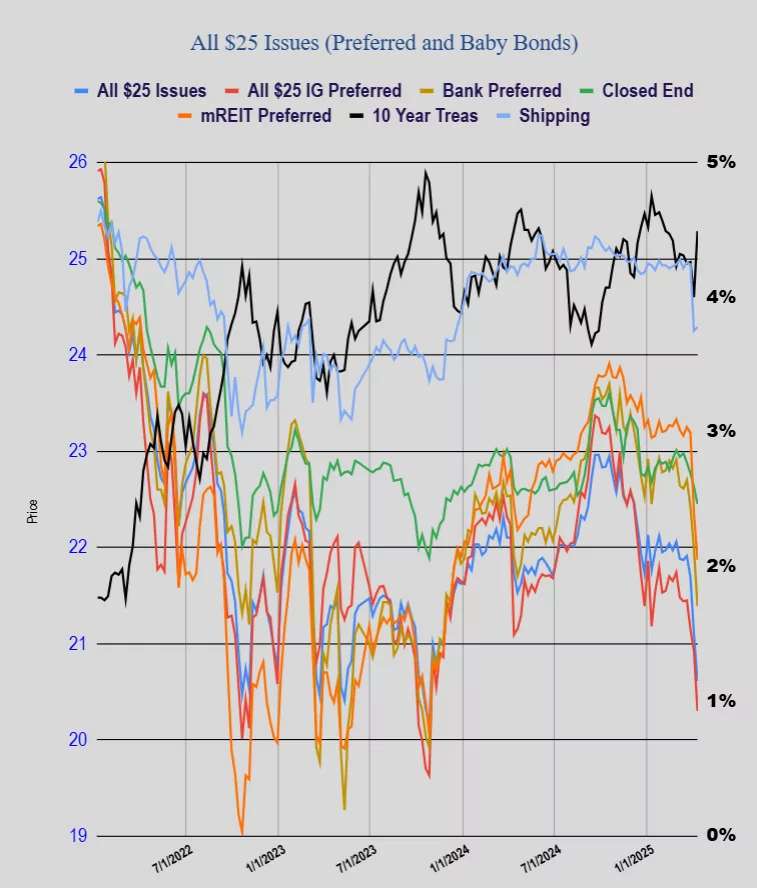

The average $25/share preferred stock and baby bond price took a shellacking last week with the average share falling by 49 cents. Investment grade issues fell 62 cents, banking issues fell 58 cents, CEF preferreds fell 18 cents, mREIT preferreds fell 48 cents and shippers actually rose by 4 cents.