Below are press releases from companies with preferred stock and baby bonds outstanding. Additionally, news of a more macro economic importance may be posted

While I haven’t done a darned thing, but watch today, I made a couple modest purchases late last week.

I initiated a position in the Saratoga Investment (SAR) 8.125% baby bonds (SAY) at a price of $25.20. Honestly I could have bought pretty much any of the Saratoga issues as they are all pretty equal–I already have a position in the 8.50% SAZ issue.

Additionally I added to my position in the Raymond James Financial 6.375% fixed to floating preferred (RJF-B) @ $25.30. I paid a bit of a premium, but most is accrued dividends. This issue is likely to be called 7/1/2026 so there is over a year before that possible occurrence.

This continues my quest to safely raise my portfolio income. Of course we all have our own definitions of ‘safe’, but these fit my definition–minimal volatility and at least 2% above the prevailing CD or money market rate.

NOTE–equity futures are off fairly sharply at 11 p.m. Sunday–with Moodys cut of the U.S. credit rating we may have some market gyrations.

The S&P500 moved up in a strong manner last week as it closed 5.2% higher than the close the previous Friday. Apparently the investing community believes ‘all is well’–well of course that is yet to be seen, but markets will do what they do and none of us has a power to change it—but have to adapt to it.

The 10 year Treasury closed the week at 4.44% which was about 7 basis points higher than the Friday before. The yield moved in a range of 4.38% to 4.54% on the week–a decent range, but no movement in either direction with conviction.

Last week we had both the consumer price index (CPI) and the producer price index (PPI) released and they both came in dovish at or below forecast. Is this meaningful? We’ll have to wait and see – as almost always we only know with certainty with the aid of 20/20 hindsight. Retail sales came in pretty soft and homebuilder and consumer confidence came in very soft as consumers are confused as to whether we are to expect inflation, bare shelves etc or not.

This week we have virtually no economic news that is typically noticed by markets– flash PMI (purchasing managers index) and LEI (leading economic indicators). Maybe investors will care this week–normally they do not. We do have bunches and bunches of FED officials shooting their mouths off all week long–virtually all of them saying nothing of importance.

The Federal Reserve balance sheet grew by $2.5 billion last week–the rate of decline in the balance is most certainly slowing and in theory this has helped keep interest rates in check by supply added demand as the Fed buys treasuries as bonds mature.

Last week, for the 4th week in a row, the average $25/share preferred and baby bond barely moved.. The average share was 4 cents higher, investment grade issues fell 2 cents and banks fell 2 cents, mREIT issues rose 6 cents and shippers fell 11 cents.

Last week was the busiest new issue week we have seen for a very long time.

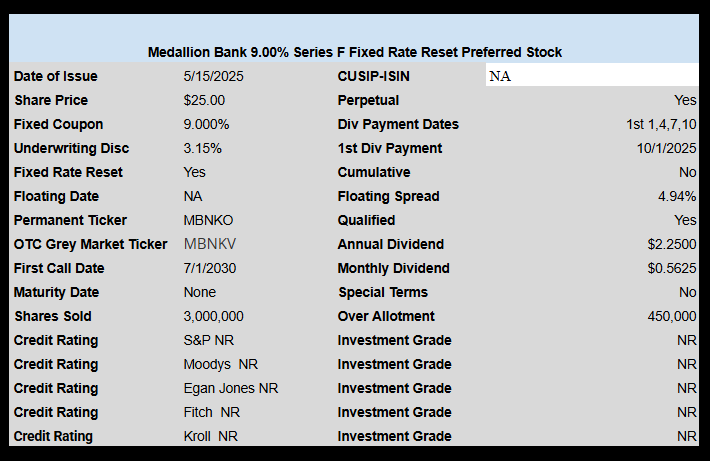

Utility Nextera sold a baby bonds, banker First Busey sold a preferred issue, mREIT Angel Oak Mortgage REIT sold a baby bond and Medallion Bank sold a preferred issue.

Medallion Bank has priced a new issue of fixed rate reset preferred with an initial coupon of 9%. It will reset at the 5 year treasury plus a fixed spread of 4.94% on 7/1/2030–then reset every 5 years thereafter.

Medallion Bank is a division of Medallion Financial (MFIN).