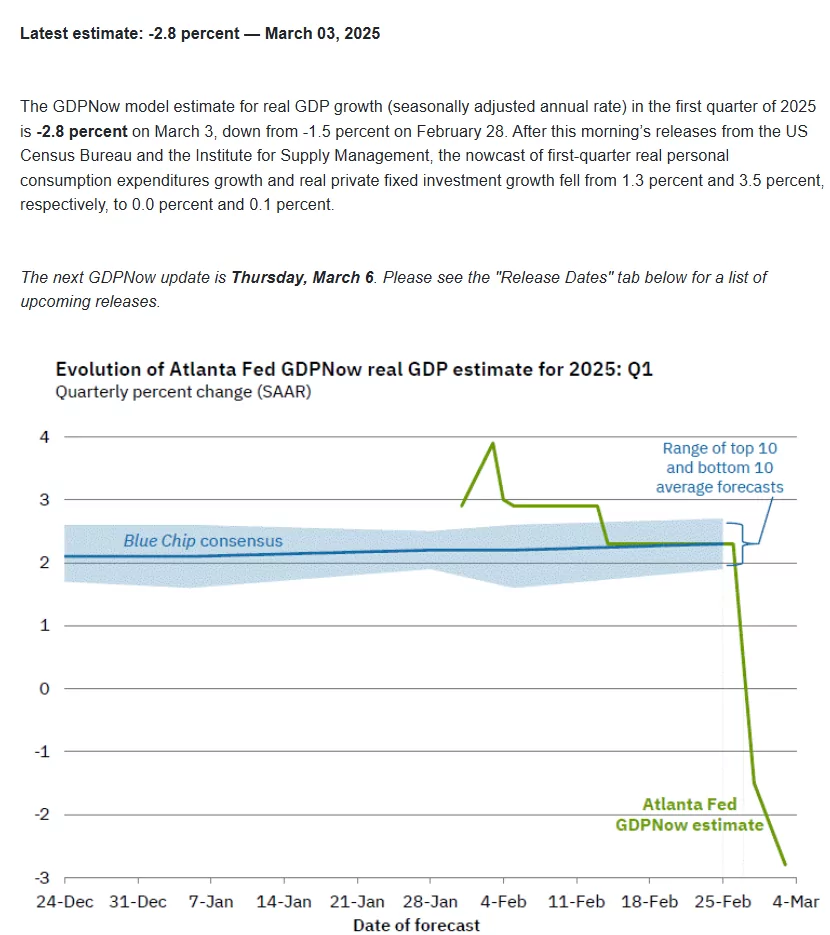

This morning the Atlanta Fed GDPNow model was updated.

The next update will be on Thursday of this week.

4/6/2025

Our site runs on donations to keep it running for free. Please consider donating if you enjoy your experience here!

This morning the Atlanta Fed GDPNow model was updated.

The next update will be on Thursday of this week.

Markets continue to move in a manner indicating no one knows for sure what is going to happen in the weeks ahead. As if we didn’t have our hands full with tariffs as well as many geopolitical events we now have the potential for a government shutdown next week.

In more normal times one could simply yawn about the government shutdown I think it is wiser at this time to pay attention. It would seem to me that with all the vitriol in the capital this shutdown could go longer and have more noticeable consequences.

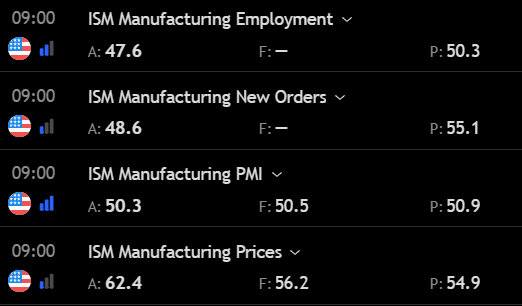

The 10 year treasury yield is trading lower once again today in the 4.18% area–helping to give just a tinge of green to income securities. Economic data–the institute of supply managers data–weak–except for the price reading which as hot.

I hate the uncertainty–absolutely hate it, BUT I have to deal with it just the same. Since our portfolios are giving us a respectable return (certainly not a super duper return) I guess I will mostly watch the drama unfold.

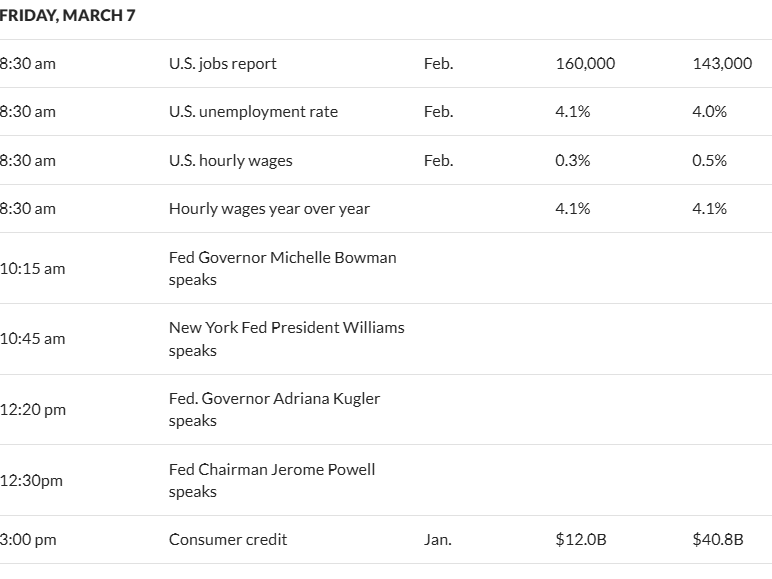

Are you ready for the week? Economic news is somewhat minimal this week–a least until the official release of jobs numbers on Friday. We can get a good hint of the economy by focusing on the jobs numbers (we also have the ADP jobs numbers on Wednesday). Also we will once again face the tariff issue at least on Tuesday of not all week long.

Last week we saw the S&P500 was off by about 1% last week with a strong bounce coming Friday afternoon which salvaged the week. The coming week we will see tariffs be activated on Tuesday against China, Mexico and

Canada—will they go into effect or will be they be paused? We’ll see as they will likely be extremely important to markets.

The 10 year Treasury fell by a huge 19 basis points last week to close at 4.23% as compare to 4.42% the Friday before. With the employment numbers being released on Friday and other more minor economic reports will likely be scrutinized closely we will see if rates break lower yet.

The Fed balance sheet fell by $31 billion as the Fed continues the balance sheet runoff. With rates falling lately I wouldn’t expect the Fed to be motivated to discontinue stop the run-off.

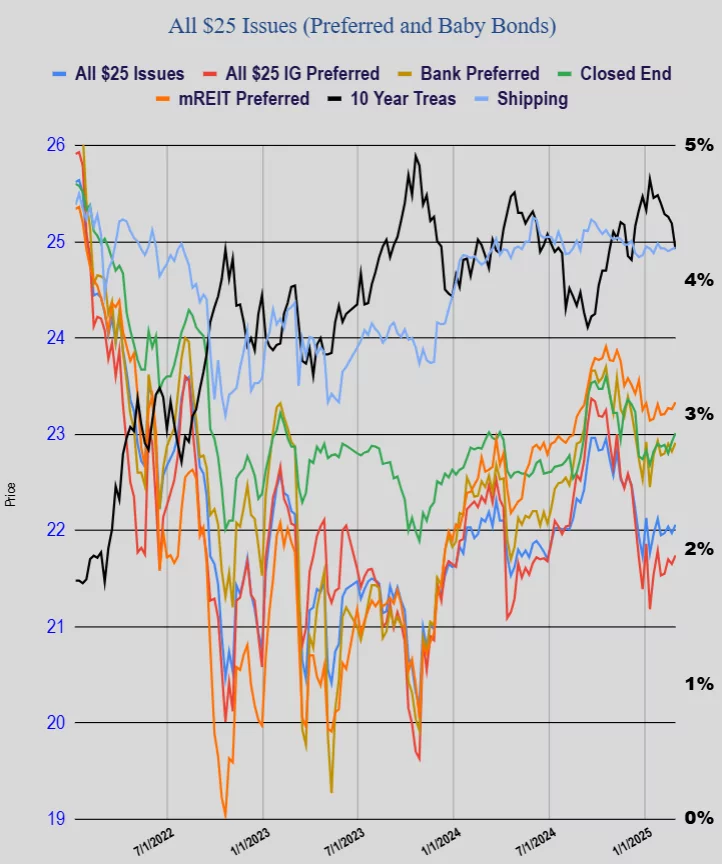

As might be expected the average $25/share preferred and baby bond rose in price last week–although quite modestly–only 9 cents. Investment grade issues rose 9 cents, banks 9 cents, CEF preferred up 8 cents, mREIT preferred moved 6 cents higher and shippers continue fairly steady and up 2 cents.

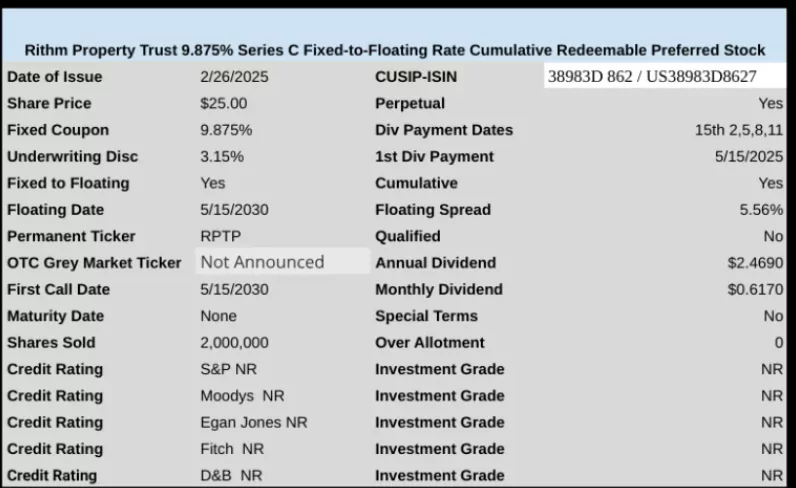

Last week we had 1 new income issue come to market as Rithm Property Trust (RPT) brought a very high yield issue to market–priced at 9.875%.

Here is a Wall Street Journal article that is simply meant by me to pass on items I find today–of interest to me, but maybe not to you.

The article deals with structured finance, including CLOs (collateralized loan obligations). Given that I have exposure to this sector I like all opinions.

Here it is. It should be accessible to all.

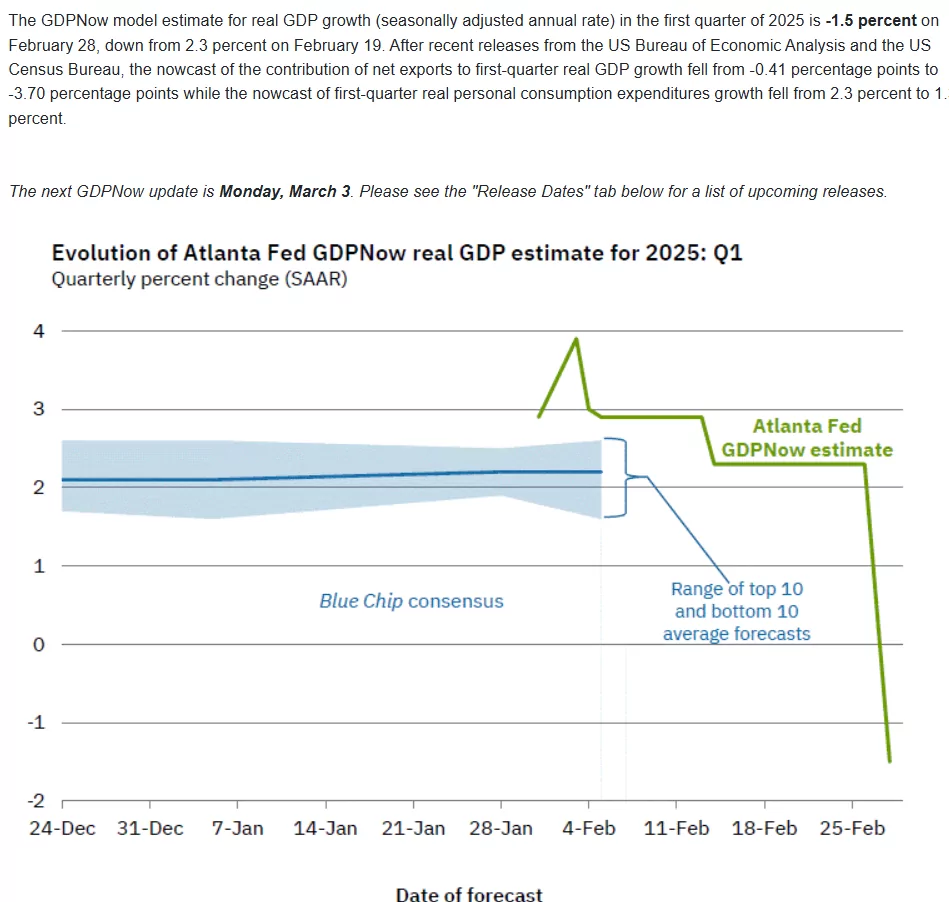

Yesterday the Atlanta Fed updated their GDPNow forecast with a dramatic drop for the 1st quarter. This tool is updated every few days and the next update is on Monday 3/3/2025.

Can the economy drop off the cliff that fast? Guess we will have to wait and see.

Further reading is here.