I’ve been looking around for something to buy—obviously a term preferred or baby bond with a maturity out a year or so. Certainly there is not much out there and my #1 favorite (XAI Octagon – 6.50% term preferred (XFLT-A)) doesn’t move lower and I already have maybe a 200% of normal position–have to resist going crazy.

Accounts are a tiny bit red today–just a tiny bit though as lower interest rates have helped to balance out macro downward movements. Honestly I have been somewhat surprised that we haven’t had that ‘baby out with the bath water moment’—it could come at any time-one never knows.

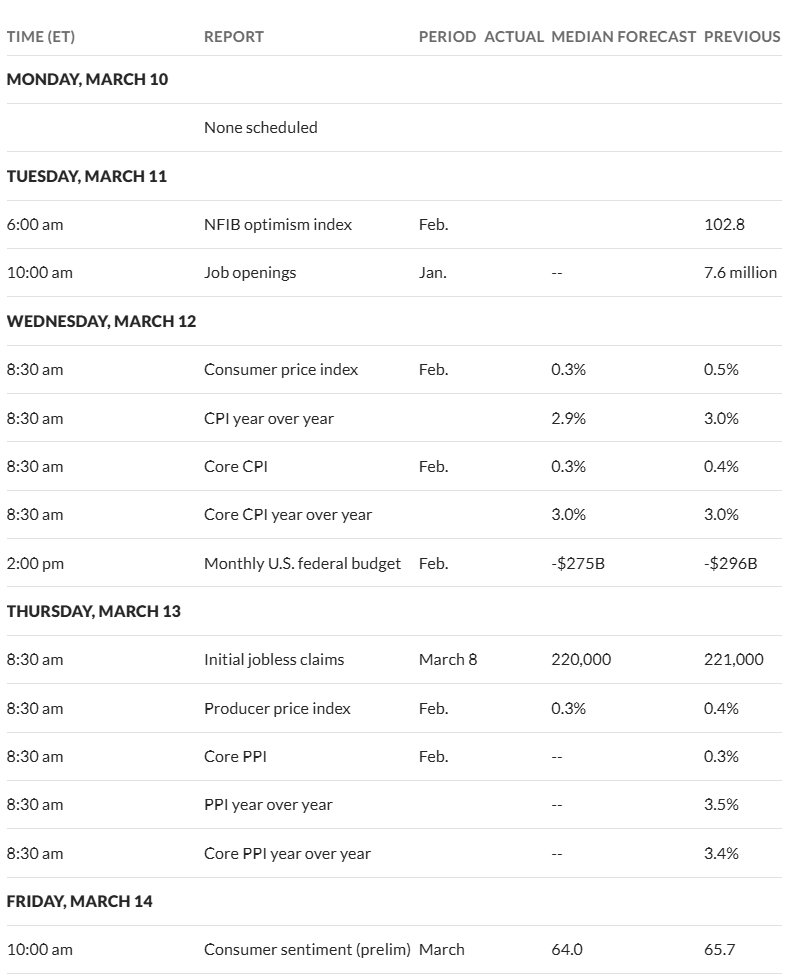

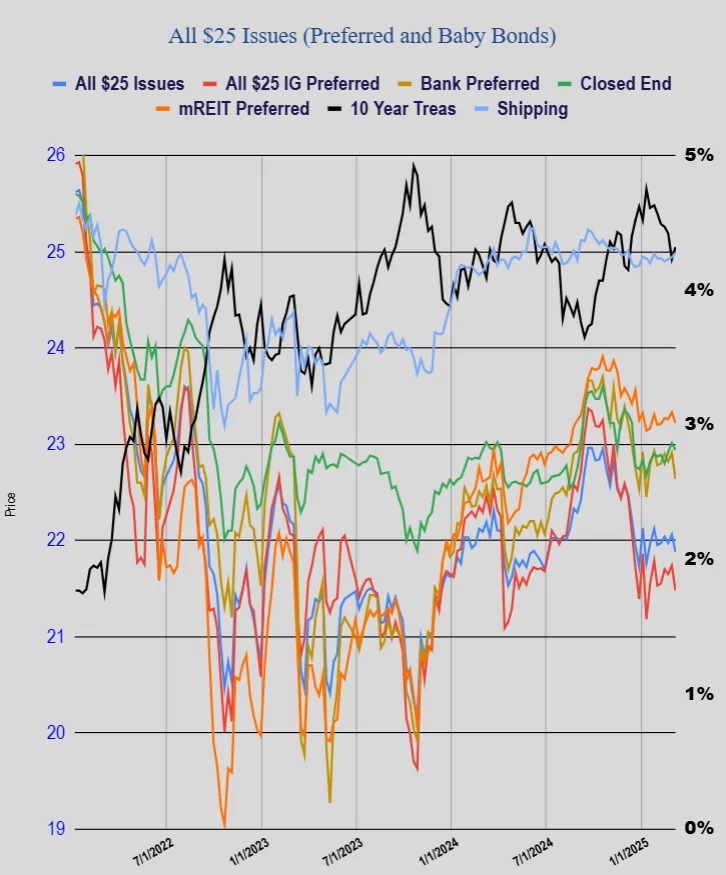

The 10 year yield is down sharply–off 10 basis points to 4.21%. No doubt that recession fears are taking hold. Equities just can’t get anything going–they keep trying to move higher–but sellers move right in to drive prices lower.

Well let’s see if we get a wild afternoon–or do we finally get a turn in stocks?