The new senior notes from United States Cellular (USM) have been priced with a coupon of 5.50%. I had personally hoped for a 5.75% simply because these fit in my current wheelhouse pretty good (just a tick or two under investment grade) so I always hope for the best.

The company is no AT&T, but the financials have been reasonable–here is the 10Q from the quarter ending 9/30/2020. Revenues are relatively flat year-over-year, while net income was up nicely. USM has been a no growth company for many years and I don’t expect that to change–on the other hand the balance sheet is strong, which is an important factor when I am perusing the financials.

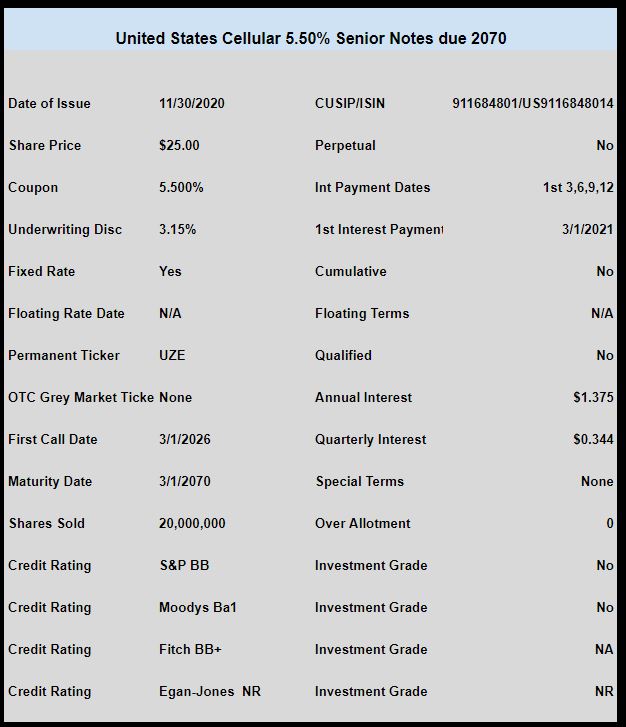

The issue will not trade on the OTC grey market, but for those who can’t wait for exchange trading you will need to call your brokers bond desk.

The pricing term sheet can be read here. Or you can see it below.

Has anyone been able to buy UZE as of yet. Not listed yet on Etrade. Thanks

It’s not listed on Fidelity either.

I purchased it through Schwab at $25.10, last I seen it priced was around 25.03.

Did you call bond desk? I don’t see it on web site

Yes, I bought it through the bond desk.

It’s a 2 billion dollar company that lets face it has risk associated with name/industry. The long term chart of the common is challenged. I think it’ll work out but do tread carefully.

Interesting that it’s neither cumulative nor qualified. How does that work? I thought only banks and insurance companies were non cumulative. Obviously not.

Jerseyvinney, This is a bond. A bond pays interest which is never qualified income. Also its a contractual payment, so it never is declared by Board of Directors which preferreds must have happen to dispense payment.

Thanks Grid. What tells you it’s a bond? Is it the ‘senior notes’ classification? Still learning.

Yes, Jersey. For our purposes it is a bond. Just different names. Like government debt. We lunchpail types tend to call them all govt bonds. But the learned people with correct terminology (something I dont do much) knows they are actually, Tbills, notes, and bonds (based on length of debt duration). Know matter what they are called they are still bonds and debt. They really arent preferreds at all. They just get lazily lumped into the category because they trade on stock exchange like preferreds do.

This exchange note buying phenomenon is a relatively new thing. Used to be they were just on bond market, then within past 25-30 years brokerages developed “retail debt” in “trust preferreds” such as KTH, GJH, etc. Most have been redeemed over time. Now you dont see these 3rd party debt stuff much anymore because direct company issued “baby bonds” are now frequently listed on exchanges.

Vinny, saw this exchange thought a word of caution might be appropriate, if your still learning. This, note is not investment grade as “Tim” pointed out, any rise in interest rates could cause a drop in principle, as 2070 is a long time. It might be better left to those that are “nibble” a have the experience. Not in my wheelhouse either.

Good point, Mike. Although I have a lot of perpetuals, I do try to get some shorter durations. And this issue is a perfect example where I can. My preference is owning the US Cellular 2033 maturity debt via GJH over this issuance. But as always there are trade offs in any decision. Thus why I tend to view them all collectively rather than isolated individual purchases.

Yes revenue may be flat but the group owns their towers and are the last large block of towers that could be bought. Interesting play. sc

Recently issued UZD 6.25% is trading at $26.76, callable 9/1/25 so the yield to call is 4.59%.

5.50% would be attractive if you could get it near par.

UZB and UZC trading ok and UZA trading at a decent premium. So, bought some by calling Vanguard

Pretty strong interest by major buyers. I see about 35 different trades of 1M+ shares.

https://finra-markets.morningstar.com/BondCenter/BondTradeActivitySearchResult.jsp?ticker=FTDS5089163&startdate=12%2F01%2F2019&enddate=12%2F01%2F2020

Sold out of UZB and purchased UZA. Betting UZB will be called. It appears this new issue is the close to the same amount of dollars as UZB and UZC.

They can save close to 9 million a year in interest by redeeming 10 million each of the two 7.25 issues or even more if they have any higher rate debt outstanding.

I don’t think the timing was accidental that one bond becomes callable tomorrow.

I was hoping for a 5.75 or 6% coupon, but its reasonable to expect these will trade higher upon them being available to trade. UZB or UZC would be the candidates they could call as a result of selling this new issue.

Revenues have stayed pretty flat and possible they will be scooped up by a larger player in later years. The lower priced debt doesn’t hurt that outcome.