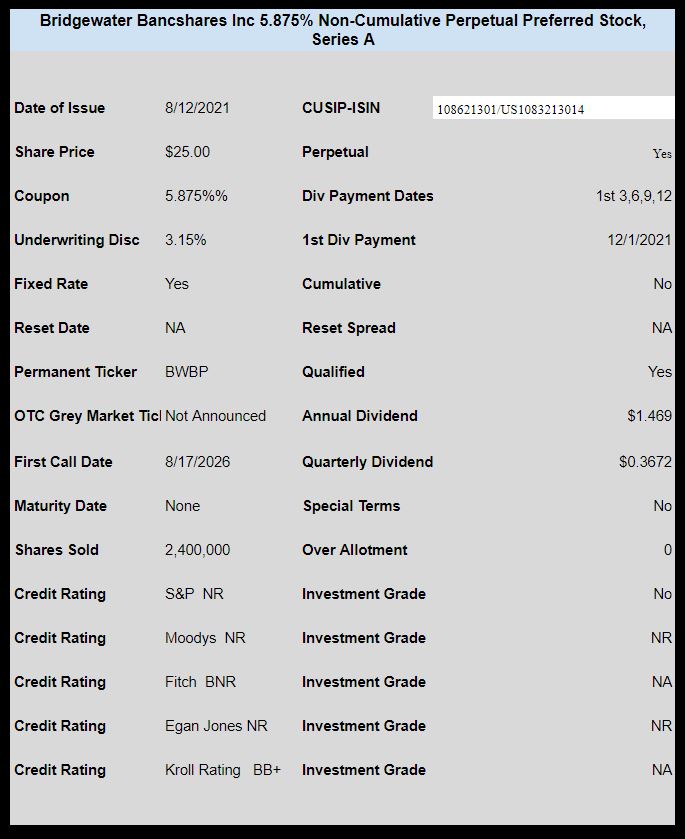

Minnesota banker Bridgewater Bancshares (BWB) has priced a new perpetual preferred share offering.

The issue prices at 5.875% for 2.4 million shares–there is another 360,000 shares for over allotment.

No OTC ticker has been announced at this time and this issue may start trading on NASDAQ at any time.

The pricing term sheet is here.

The preliminary prospectus can be read here.

af has been on top of this one.

Can anyone say whether this issue is expected to trade OTC Grey first? (That’s what I’d assumed…)

Bur–just started trading NASDAQ–BWBBP

The second press release says that the permanent symbol is BWBBP. Neither BWBP nor NWBBP seems to be active yet.

Now for your retired bankers in the group I would love to hear your opinion on this little bank. I read their website. $3 Billion in assets, 7 locations all in Minnesota, 214 employees, they pay their CEO one hell of a lot of money for a really small bank (over $1 Million annual salary), I have found trying to figure out bank statements above my pay grade so most likely will pass unless you bankers tell me your going to load up and WHY.

LarryL wrote over on Reader Alerts that “Bridgewater appears to be a very small community based bank in Minn. with $3.2 bil in assets, and a total of 7 branches. No common stock dividend. If the Chairman Jerry J Baack has a history in banking, I am not finding it. Jury is out as to whether I will take a flyer on this one.”

Jerry’s bio…would appear he has a history in banking…

President and Chief Executive Officer, Chairman of the Board

As the principal founder of the Company and the Bank, Jerry was responsible for all aspects of the Bank’s formation, including the initial capital raise, business plan, board and management team structure and recruitment, charter and regulatory approval. He currently serves as Chairman of the Board, Chief Executive Officer and President of the Company, positions he has held since the Bank was founded in 2005.

Decent bank led by industry veterans (CEO is paid a lot, but he has grown the bank significantly while maintaining solid credit quality).

Targeted commercial loan strategy, primary focus has been on originating multifamily loans. Growth is attributable to (1) targeted strategy / focus and experienced team and (2) consolidation within the Twin Cities market (TCF merged with Chemical, which then merged with Huntington. Old National has been aggressive in acquiring banks and Wells Fargo has had regulatory issues). Deposit portfolio is biggest knock on bank – but the low rate environment is helping to reset deposit balances over time.

Small bank to issue preferred. Typically preferred were only really open to banks with larger balance sheets. Looks like that has changed some.

Biggest risk is concentrated multifamily portfolio in Twin Cities. Credit quality has been solid, but that can always change. Housing market is tight, but cold weather and high taxes aren’t exactly a combination for continued growth.

BWB will continue to grow until the larger guys start noticing and begin to price loans aggressively. Market disruption from consolidation will continue to provide opportunity.

I like this in small doses. Will be an acquisition target once assets get north of $5 bn.

John, thanks for the info. What do you mean by “Deposit portfolio is biggest knock on bank”? What about the deposit portfolio makes it a (possible) negative?

BWB has roughly 30% of deposits in time and brokered deposits. Such deposits carry higher rates, transient and rate sensitive. With the low rate environment, BWB has been able to reprice funding costs lower, but such deposits are always viewed as less desirable and are not considered “core deposits.”

Thank you!