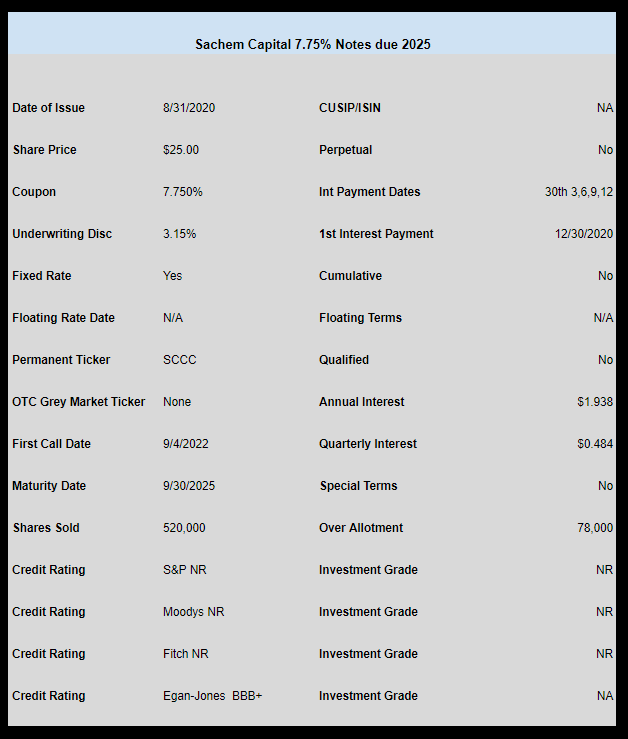

Hard money lender Sachem Capital (SACH) priced their new issue of baby bonds.

The coupon is 7.75%. The issue will trade under ticker SCCC in the next week or two.

The company has 2 other lower coupon issues outstanding and you can see them here.

The pricing for the issue can be read here.