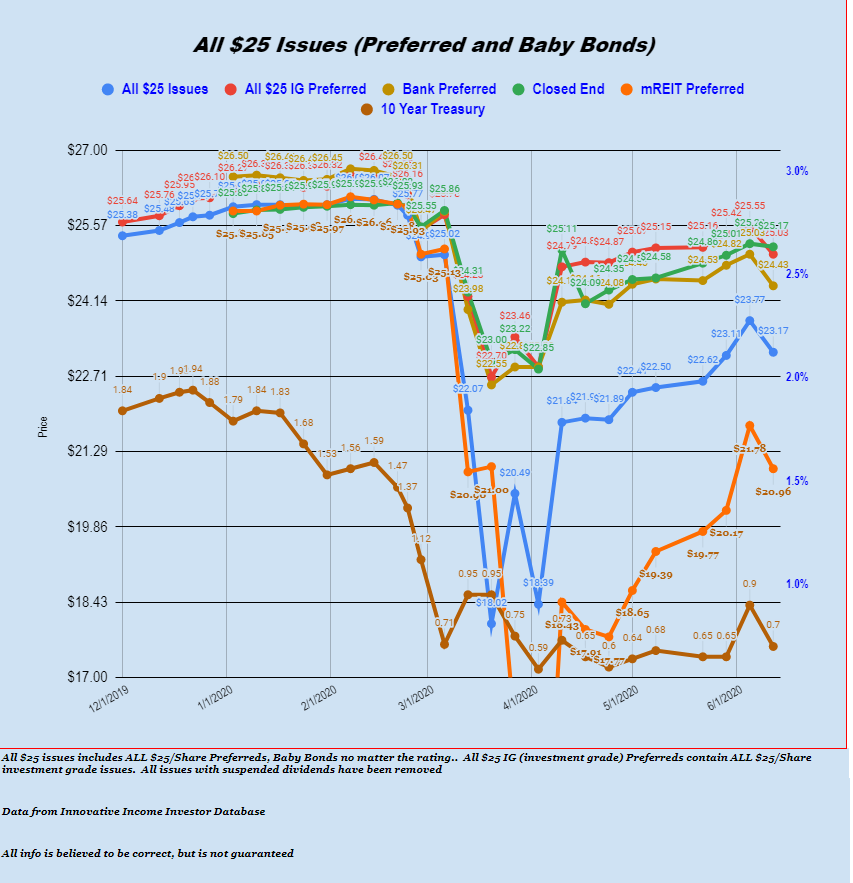

The S&P500 traded in a range of 2984 to 3233 last week before closing at 3041 which is a loss of about 5% on the week.

The 10 year treasury traded in a range of .65% to .92% before closing the week at .70%

The Fed balance sheet grew by only $4 billion last week–certainly the smallest rise in months.

The average $25/share baby bond and preferred stock fell by over 2% last week. Bank issues fell by 3%, utility issues by just over 2%, lodging REIT preferreds by 6%. This was the 1st losing week since back in early April.

Last week we had 3 new income issues announced.

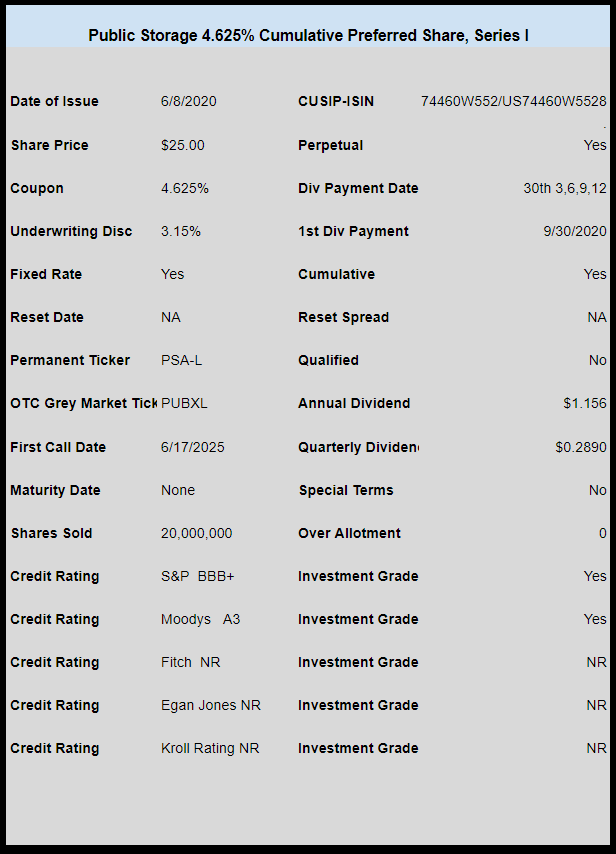

We started off the week with self storage giant Public Storage (PSA) announcing a new perpetual. The new 4.625% coupon issue is trading under temporary ticker PUBXL now last traded at $24.50. They have called the 5.375% PSA-V issue with the proceeds of the new offering.

Associated Banc-corp (ASB) announced a new non-cumulative preferred issue with a 5.625% coupon. The issue is trading under OTC grey market ticker ABBCL and last traded at $24.67.

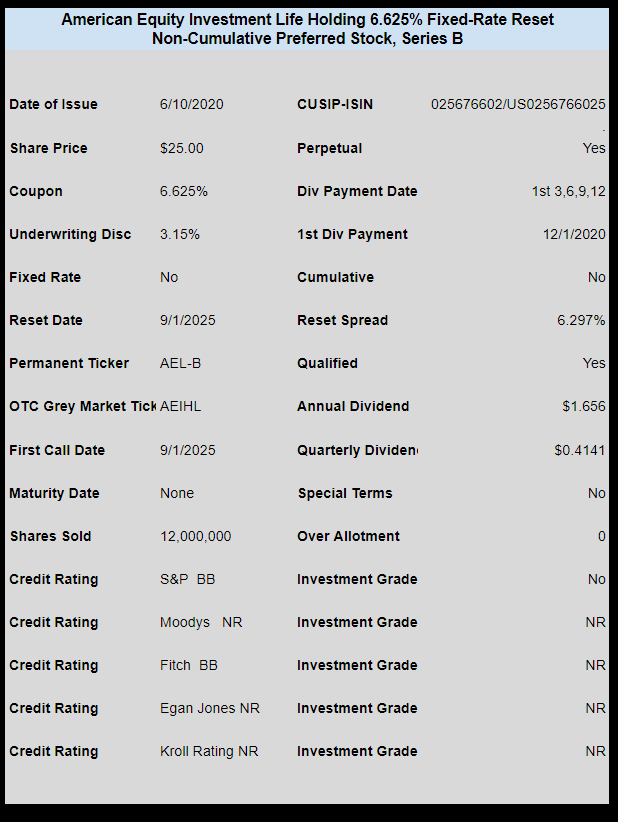

Lastly annuity provider American Equity Investment (AEL) announced a new non cumulative perpetual preferred that is a fixed-rate reset issue (reset every 5 years). The issue is trading under temporary ticker AEIHL and last traded at $24.56.