Second, I was told by a representative of the compliance department at OTC Markets.com that HMLP-A would move to the expert market immediately upon delisting. And sure as heck, here’s the new symbol – HMLPF. https://www.otcmarkets.com/stock/HMLPF/overview.

BUT: It looks like it listed as “Pink, Current”. So it should trade at most US brokerages, and the “expert” listing info I got from the compliance dep’t. at OTCM was wrong, at least for now.

Third, I am nearly 100% certain that the ICE Exchange-Listed Preferred & Hybrid Securities Index (Bloomberg ticker PHGY) has not yet removed HMLP-A from its January, 2023 constituent list. (As I write this, ICE is still showing the 12/31/2022 date for all of its benchmark indices.) The reason I am so confident in this projection is that PFF, which uses the ICE Index as its benchmark index, as of Friday December 30, 2022 still holds 533,169 shares of HMLP-A. PFF gets an early look at changes to the ICE Index – for example, they got rid of several hundred thousand shares of the Pennsylvania REIT (PEI-B, PEI-C etc. now trading on the OTC Markets as PRETL, PRETM, and PRETN) so I am equally confident that the PEI preferred shares have been removed from PHGY. (The January, 2023 PHGY constituent list will be updated later today, and I’ll try to remember to post it.)

Fourth and finally, I believe this means that HMLP-A will be removed from the PHGY constituent list effective on February 1, 2023. That’s when the “fun” will begin for HMLP-A – when PFF is forced to start selling its shares.

Just a reminder that the 3 preferred issues from Drive Shack (DS) as well as their common shares are delisted effective today.

The company has been late filing their reports with the SEC lately and has had difficult financial times (for years). Common shares had traded down around 16 cents with preferreds in the $8 range.

Time to get back to real life after too many holidays – at least for me. In Minnesota with snowy and cold weather, being inside for these days is not to my liking. On the other other hand if you are a skier (downhill or cross country) or a snow machine rider maybe you are loving it. Obviously I live in the wrong state.

So last week, which was a 4 day market week, the S&P500 was off just 1/10th% as the trading range for the week was just about 1 1/2%–narrow considering recent history. Economic news was fairly sparse which helped in keeping the range narrow—but it is unlikely to be that way in the coming week.

The 10 year treasury was up 13 basis points to close the week at 3.88% compared to a close at 3.75% the previous Friday. The high yield for the week was 3.91% so we closed near the top.

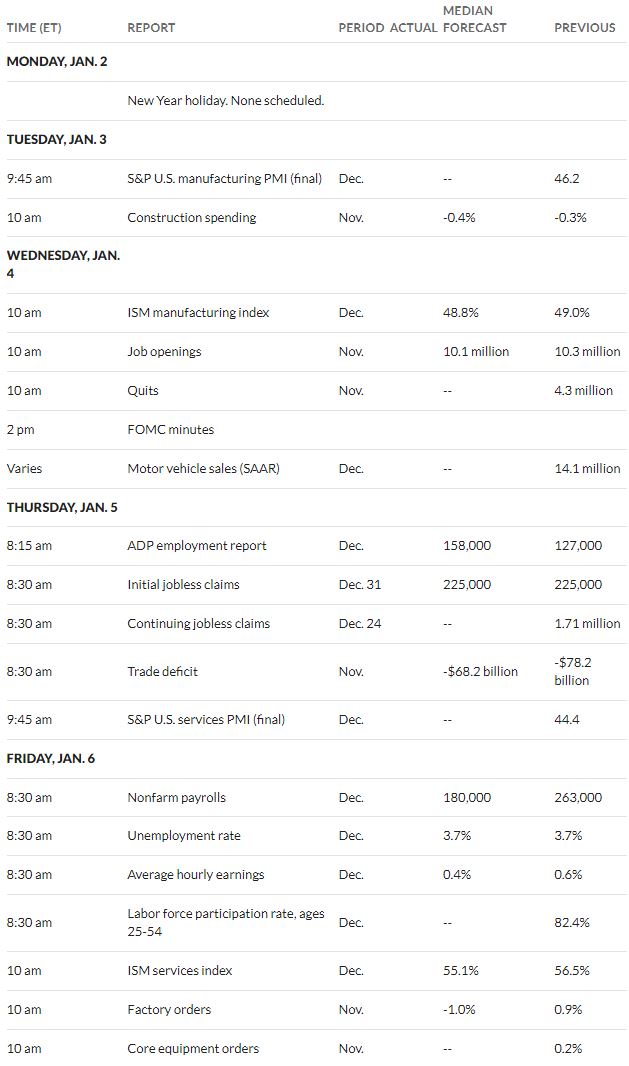

For the coming week we have a number of economic reports which will be market moving. We have the FOMC meeting minutes released on Wednesday for the last meeting and while it is ‘old news’ it will move markets. We have employment reports on Wednesday and Friday (ADP and then the government report on Friday)—this will move markets as the FED will assign a high weighting to the report for the FOMC meeting which happens on 1/31 and 2/1. They really want some softening in the jobs market.

The Federal Reserve balance sheet was down $13 billion last week–likely creating a little ‘tension’ for future numbers as the Fed looks at their monthly caps (maximum) of reductions of $95 billion, which they have been way below the last month. The Fed reserves the right to adjust their monthly cap dependent on financial conditions–a section of their statement on reducing the balance sheet is below –

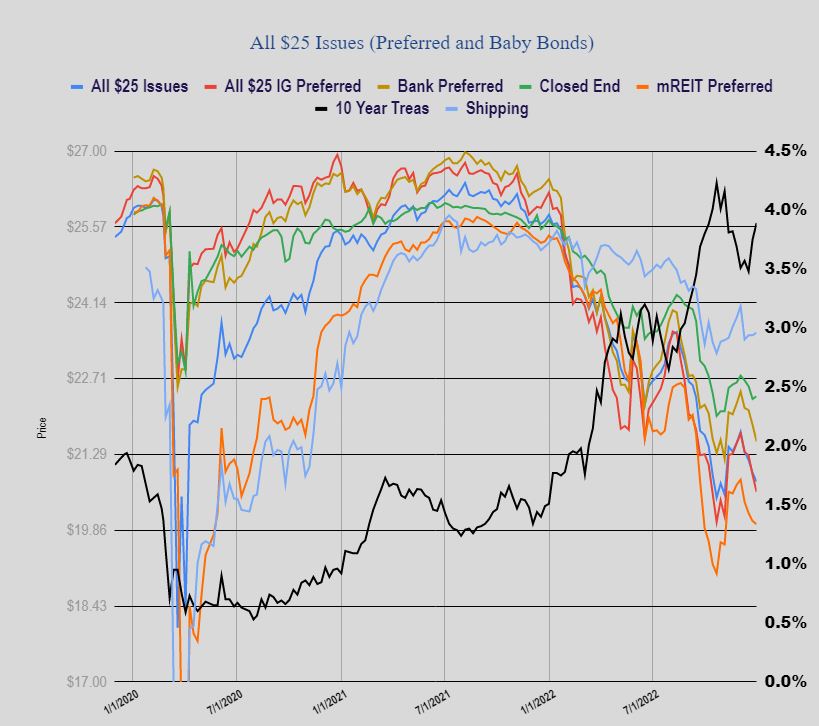

Last week we again saw losses in most $25/share preferred stocks and baby bonds – this time to the tune of 17 cents per average share. Investment grade issues were hammered lower by 32 cents, while banks were off the same 32 cents. mREIT preferreds were down just 6 cents and shipping issues were up a nickel.

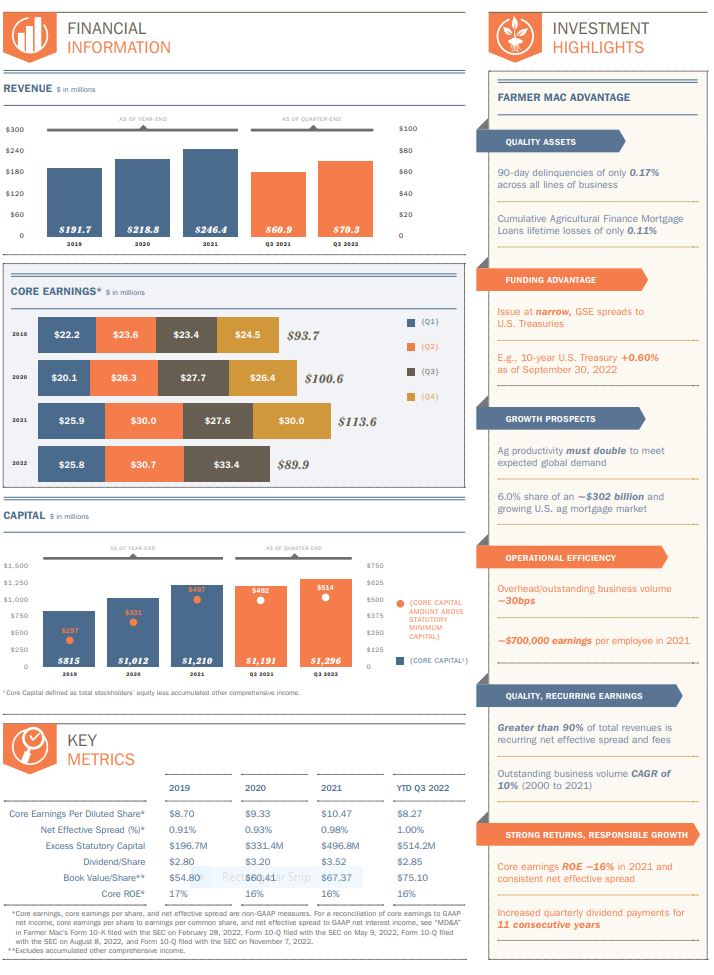

The Federal Agricultural Mortgage Corporation (AGM), also known as Farmer Mac, is a relatively large lender, primarily to the rural agricultural sector in the United States. This includes rural utilities (such as cooperatives like the one that supplies my electricity on the south side of the Twin Cities). Farmer Mac is not a primary lender, but only acts in the secondary market providing liquidity to the primary lenders. For instance the Farm Credit System members are primary lenders and work directly with farmers and ranchers.

I am reviewing this one because I mentioned this one this week and others have mentioned it and own some of their preferred shares. The company has 5 preferred issues currently outstanding with coupons from 4.875% to 6%, current yields from 5.08% to 6.93% (the 5.08% current yield is a fixed to floating rate issue). Yields to 1st optional call ranges from a -7% to 17%.

Here is Farmer Mac’s own description of their business–

Farmer Mac is a vital part of the agricultural credit markets and was created to increase access to and reduce the cost of capital for the benefit of American agriculture and rural communities. As the nation’s premier secondary market for agricultural credit, we provide financial solutions to a broad spectrum of the agricultural community, including agricultural lenders, agribusinesses, and other institutions that can benefit from access to flexible, low-cost financing and risk management tools. Farmer Mac‘s customers benefit from our low cost of funds, low overhead costs, and high operational efficiency. In fact, we are often able to provide the lowest cost of borrowing to agricultural and rural borrowers. For more than a quarter-century, Farmer Mac has been delivering the capital and commitment rural America deserves.

The company was chartered by congress in 1987 and was publicly listed in 1999–so they have been around for 35 years–not new, but also not old as these things go. While they are a government sponsored entity, the federal government doesn’t guarantee that they pay their debts or dividends so no one should be lured into thinking this makes a dividend payment or preferred share price bulletproof (witness Fannie Mae back in the financial crisis days).

The company has chosen not to have their preferred shares rated, but a review of their financials shows they are superior to virtually every other lender.

Below is a ‘fact sheet’ on the company. I realize the print is small but below the sheets I have a link to the original source document.

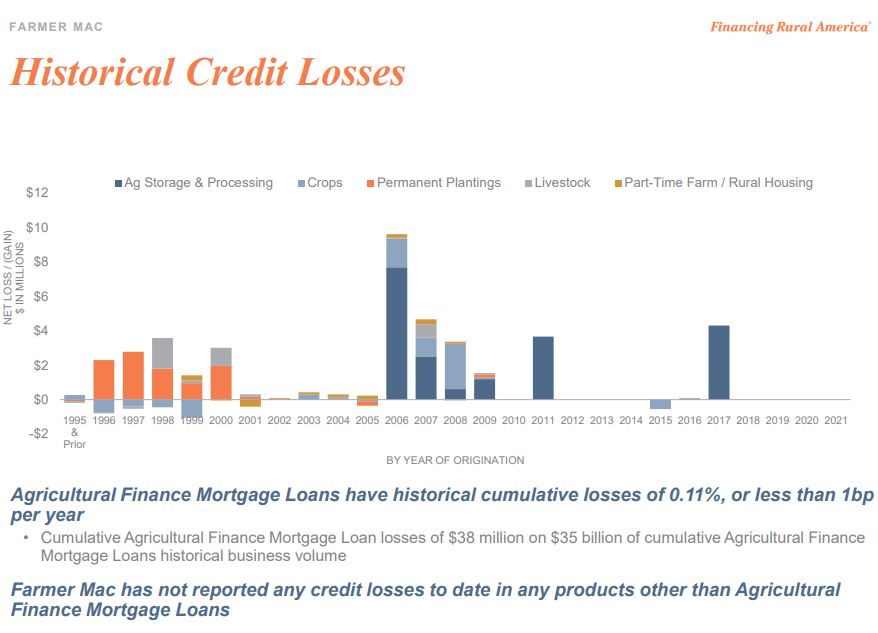

Note that they have sustained losses over the years of just .11% on over $35 billion of loan volume. Additionally they have not ever sustained a loss in the Rural Utilities, USDA or Institutional lines of credit businesses. Currently they have .17% 90 day delinquency rate–compare that to any other lender out there and you will find this is excellent–just for comparison sake I compared against U.S. Bank (USB) who I consider an excellent lender. USB has a rate of .11% (excluding non performing loans) or .30% including non performing loans.

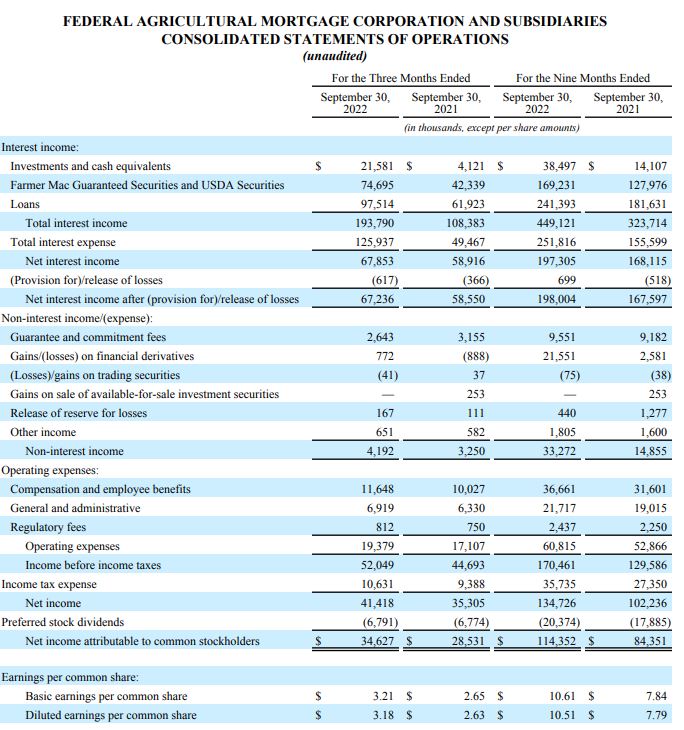

Below I have posted the consolidated statement of operations for the quarter ending 9/30/2022. Note that the net income has grown very nicely from the year ago quarter and year ago 9 month period. Look at the provision for loan losses–virtually NONE on a book of loans of around $25 billion.

As you review this operating statement you might note that the absolute level of net income is not huge for their book of business (loans). I think that is a fair observation–but AGM can borrow very cheaply and the loans they make are at very fair rates. The company only deals in 1st mortgage loans and they target loan to values between 40 and 50%—this is very conservative which greatly contributes to their loan loss ratio. Additionally when there are defaults on loans AGM rarely takes a loss because of the equity present in the mortgaged property.

So what about the performance of AGM on a longer time frame? Below is a chart for AGM which goes to company inception. You can see that the largest credit losses the company has ever had was in 2006 and it appears that the credit losses were about $10 million–almost a rounding error in their large book of business.

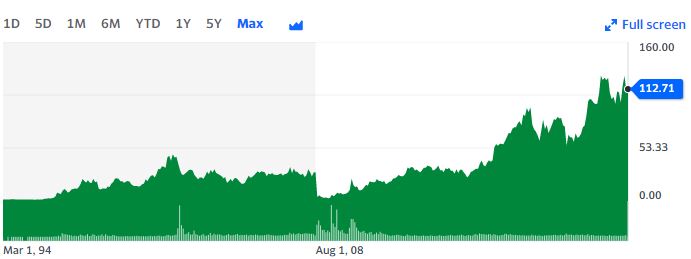

Now because most of us like to review the common share performance as a metric when considering purchasing preferred shares–how has the common done. We can see that the common shares traded all the way down to the $2.50 area in 2008–that is pretty scary. We know that we had the financial crisis then and that Freddie and Fannie Mac went belly up (essentially as they are still operating under a conservativeship to this day). What about Farmer Mac?

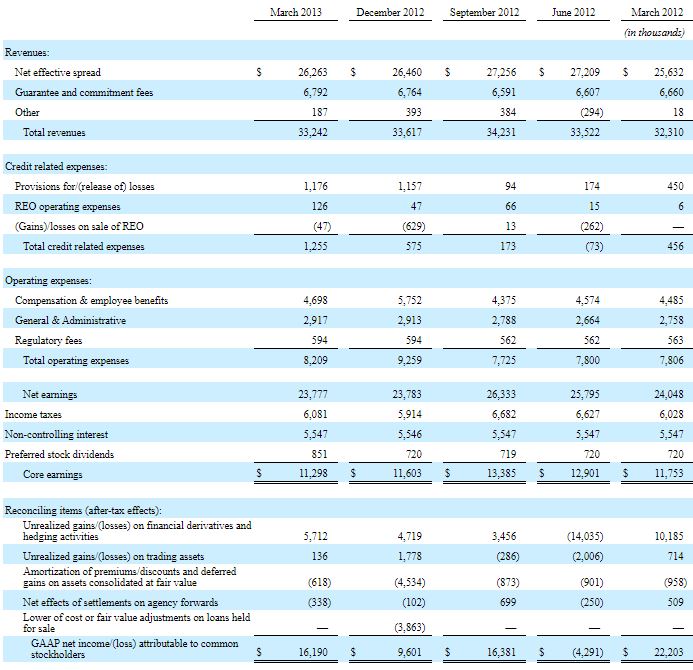

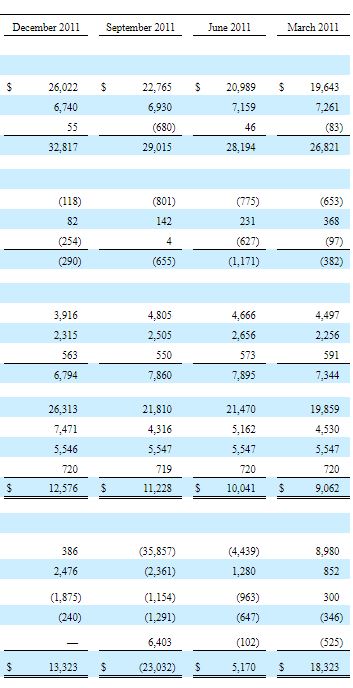

Normally I would simply go back to the 10-K (annual report to SEC) or quarterly 10-Q reports to find out what happened back then. But alas the SEC edgar system only goes back to 2013 for AGM and from the 2013 reports I can get back to data from 3/2011. Below are quarterly financials back to 3/2011–I have divided it into 2 pages in my attempt to make it legible.

We can see that they certainly had some challenging quarters and with their thin margins disruptions can take a toll. The provisions for loan losses were reasonable numbers–but as a percentage higher than they currently are at. On a GAAP basis adding in unrealized losses of hedging operations they sustained a couple quarterly losses–but no annual losses in 2011 and 2012. All in all, considering the financial crisis, these financials are somewhat acceptable. So why was the stock price $2.50 or so in 2008?

So I am without financials statements prior to 2011 so a Google search will have to do.

So here is what I find. In 2008 Farmer Mac held preferred shares in Fannie Mae and additionally they had exposure to Lehman Brothers. Because of these huge losses AGM had a capital ‘crisis’ in which the Farm Credit System Banks and Zion Bancorporation stepped in with a $65 million capital infusion.

Additionally there is another Forbes article titled “Farmer Mac Mowed Down by Fannie’ about this same time–I am unable to access this article.

In October, 2008 the congressional research service published a report specifically about the Farmer Mac capital issue. The report is here.

The bottom line is that Fannie Mae and Lehman Brothers caused a capital crisis at Farmer Mac–shares plunged in 2008 to the $2.50 area from the $30 area when the Fannie crisis started.

So do events from 14-15 years ago have relevance to today? I think that history tells us that we have to have our eyes and ears open all of the time and watch for systemic events. To think that one government sponsored entity would nearly start the dominos tumbling to other government sponsored entities likely was not considered likely at the time–but now we KNOW. As ‘knowledgeable investors’ we MUST pay attention to systemic risk where ever it might be.

While AGM has not suffered operating losses–this shows how investment losses and loss of capital can almost sink a lender.

With something new comes confusion–I need to add more information to the donation page.

Receipts coming from Paypal show donations to triplei201611_@_gmail.com. (remove the underscores) This is simply the email for the website.

I will add this info so as to not cause further confusion. My apologies to those that have been confused by my lack of info–it is a learning experience for me.

In the never ending story of contrasting economic signals the Chicago Purchasing Managers Index came in hotter than expected.

The index came in at 44.9 versus expectations of 40 and last months reading of 37.2. Of course nothing moves in a straight line and the readings in the last year have been kind of ugly–but ‘ugly’ numbers haven’t translated much into weakening jobs numbers.

Finally we get to put a wrap on this year–and to say I am ready for an end would be an understatement. This grind day in and day out has been exhausting and has created plenty of red in our preferreds and baby bonds. Of course it could have been worse–and maybe it will be, but that will be NEXT year–today marks the end of THIS year.

Now if I was a regular writer on Seeking Alpha I would have virtually NO losses–yes it is true. Since most of my losers have not been sold – they aren’t losses!! Actually I like SA and I use it for ideas, but now pretty much all of the most popular folks claim that losses aren’t losses at all–well I guess you just make up the rules as you go–when stocks are going up they are gains, but when they go down they are NOT losses. Oh well whether unrealized or realized losses they are losses. Everyone has their opinion and should do what makes them feel good.

Today the S&P500 futures are off almost 1/2%—thinking this is meaningful is kind of silly, although yesterday futures were green and we continued through the day with a pretty vigorous rally. We know that if we tossed a coin right now we could predict the regular trading day–without the futures market. I prefer flat to a bit up so we don’t get substantial bleed into the income issues

The 10 year treasury is at 3.86% right now which is up a couple basis points from yesterdays close. With only the Chicago PMI being released at 8:45 a.m. we shouldn’t see too much movement in rates.

Yesterday I took a nibble on the Federal Agricultural Mortgage 5.25% perpetual preferred (AGM-F) now with a current yield of 6.82% and yield to first call of around 15%. While my intention was to nibble on a regional/community bank I couldn’t pass up the current yield on this issue, that while unrated, is pretty much investment grade–I hope to write more on Farmer Mac in the next few days or week.

Today I will do no nibbling. I have my annual full body check for skin cancer. I am a picky person when it comes to doc’s and I need to drive an hour each way to my appointment–I could do it at Mayo locally, but I don’t need everyone knowing my business in this small town (not because of the clinic folks, but the ‘locals’ that see you at a clinic). When I find either doc’s or dentists that I am comfortable with I stick with them and will gladly drive an hour and I found that in Faribault, MN just east of me.

Monday markets are closed once again as folks recuperate from their holiday celebrations–won’t be a problem for me because a single glass of bubbly will be plenty.

Once again the equity indexes are up pre-market as has been true for days–and each day equities sell off once the regular session opens. Certainly there are plenty of reasons to sell-not the least of which is tax loss selling and I suspect there is plenty of that going on. If tax loss selling is a major contributor to the losses we should see an end soon–maybe even get some bounces.

Interest rates (the 10 year treasury) are trading around 3.87% this morning down a basis point or two from yesterdays close.

In minutes we get the weekly initial jobless claims number and while in the past this has been a number totally overlooked by everyone that is not the case anymore–everyone is searching for weakness in economic data and I think that the jobs numbers are some of the most important out there–it is hard to imagine a very soft economy until we see some weaker job numbers. We’ll see what we get in 15 minutes.

Yesterday we got weakness in pending home sales – this is another economic sign I think is important, but thus far the fall is sales has not translated to much lower pricing. Certainly there are pockets of price weakness, but many areas are flat to off a few percentages. Inventories remain tight in many areas–some areas have nothing for sale, thus prices have remained stable. We need to see some more weakness here. The Fed is watching.