While todays moves in stocks is NOT really too scary, the further plunge in the 10 and 30 year treasury bond yields has to give one a bit of a startle. In addition gold is spiking a bunch higher – up $29 last I looked.

The 10 year treasury yield fell as low as 1.44% before bouncing a bit to 1.47%–we are not quite at new record lows, but at this pace it could happen soon. The 30 year bond was at 1.91% last I looked which is a record low–can you feel all of your investment grade investments being ‘refinanced’ soon? These falling yields are in the face of reduced liquidity from the Fed–obviously the fear trade is overwhelming other factors.

This corona virus issue is started to take hold in a big way–I mean riots in the streets in Ukraine overnight shows the power (and maybe danger) of social media. Information–both factual and ‘fake’ moves very fast.

Then on top of the virus issue we see that the purchasing managers index at 49.4 showing a slight potential in the economy slowing. It was only earlier this week that the Philly Fed Manufacturing Index came out extremely hot—everyone will have to make their own determination as to what the hell is going on for sure.

1 thing I know–if I was holding shares in either Triton International (TRTN) or CAI International (CAI) I would be studying trade disruptions carefully. Both of these companies are huge providers of containers moving back and forth between Asia and the rest of the world. Thus far the common stock of the company’s have not really reacted to virus related trade disruptions–certainly their preferreds haven’t suffered–all 6 issues are trading really strong. Certainly if the disruptions are a short term item the companies will do just fine–but a larger spread–who knows–these companies carry a ton of debt and need a continuous flow of revenue to make their payments–no room for error.

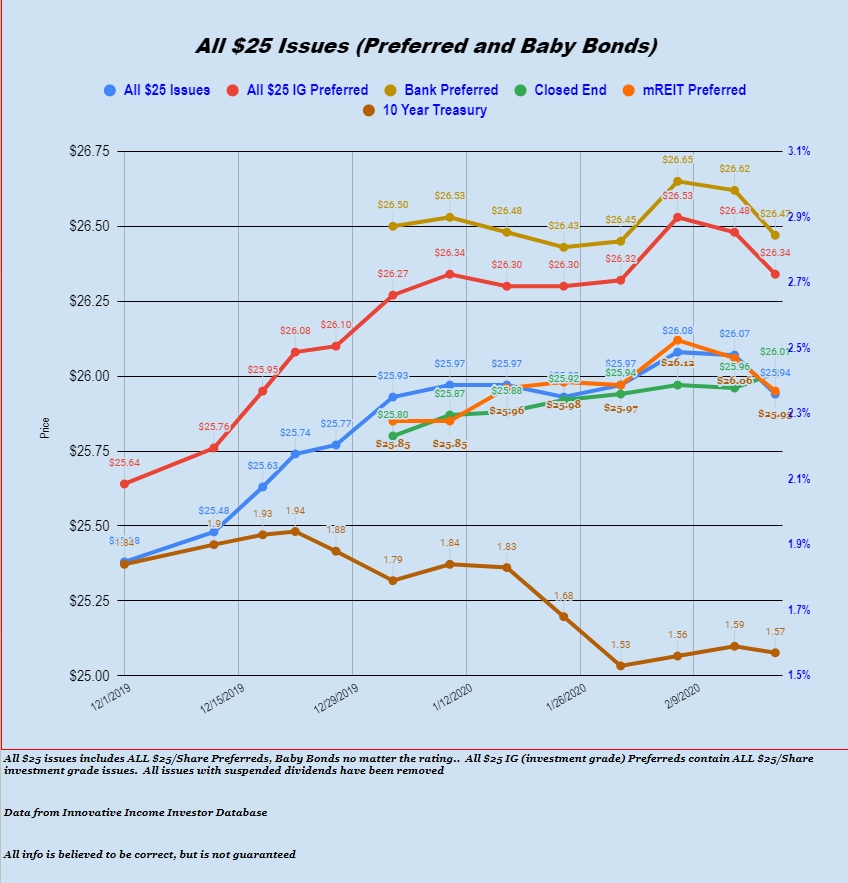

Looking over $25/share preferreds and baby bonds today I see mostly green. Investment grade is up 2 cents, while overall shares are up 3 cents. There is a lot of complacency in the income arena so it seems.

This is one of those days to fasten your seat belt into the close of the markets in 2 hours–with the weekend ahead will folks unload their risk assets (stocks)?