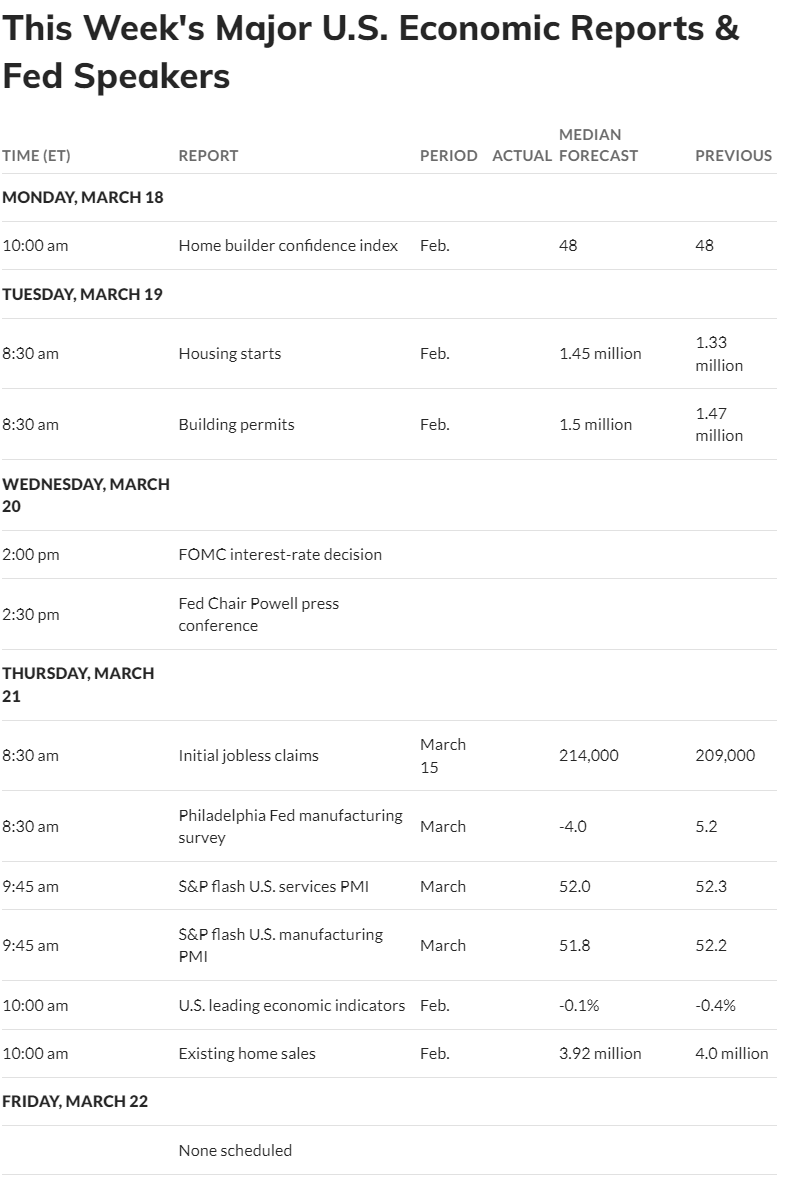

Well it has been a somewhat decent week–for common stocks and for income issues. Of course we had important economic news with the FOMC meeting and Jay Powell presser which markets decided was somewhat dovish–all news was good news I guess.

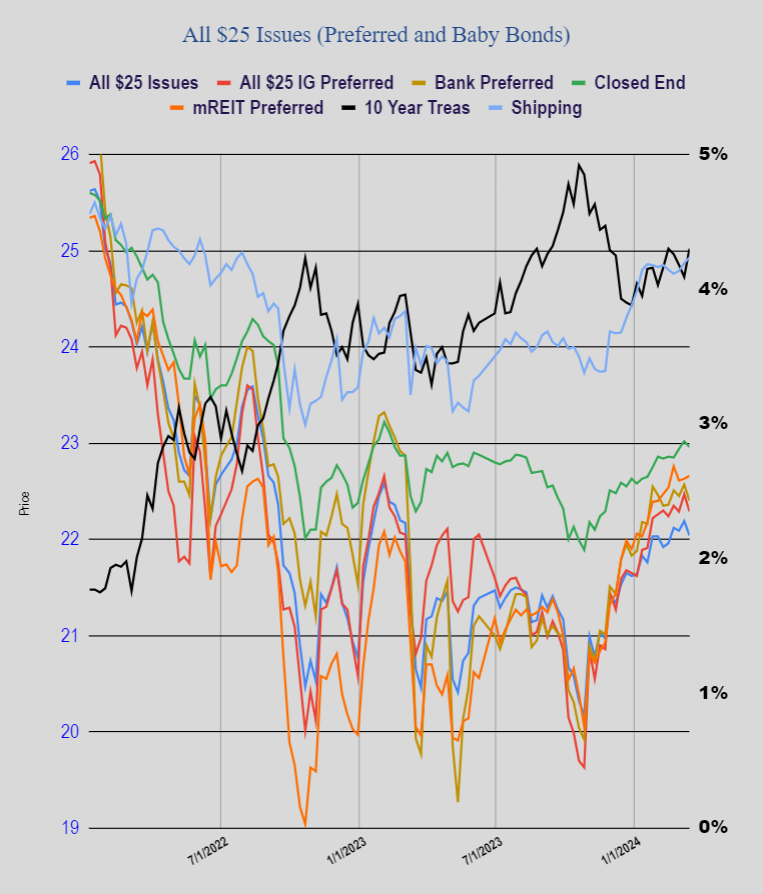

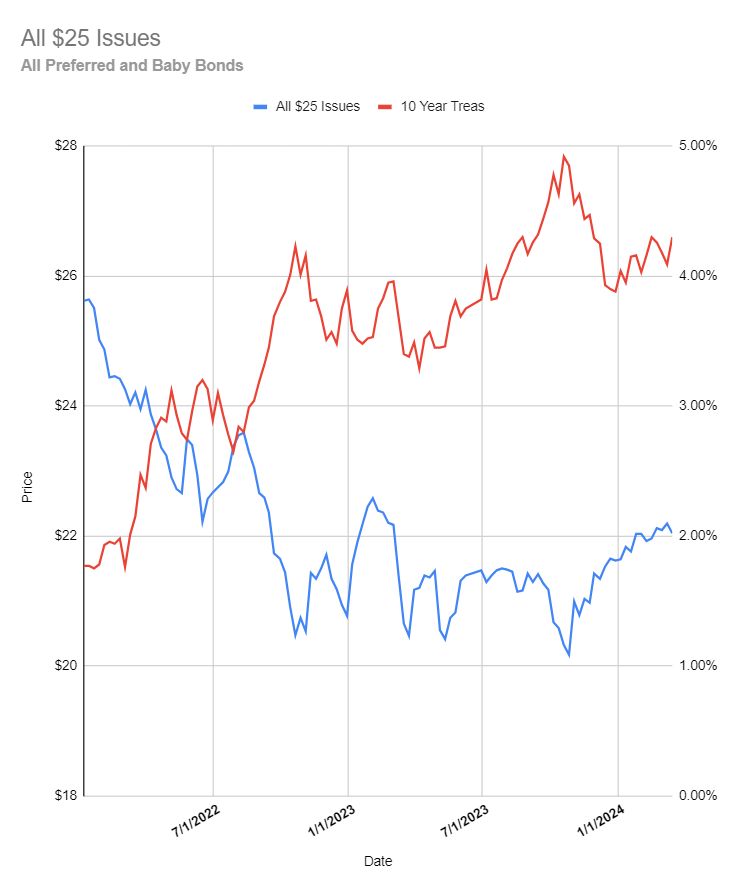

Interest rates as represented by the 10 year treasury have fallen a bit through the week—but the reduction was minimal given the rise in the S&P500. The 10 year treasury is at 4.27%–down a measly 3 basis point from last Friday–with the dovish Fed news one could have expected a 10 basis point reduction in yields.

The S&P500 is up almost 2% on the week and equity futures are up a bit this morning. One has to feel like equities are overvalued–but honestly compared to valuations we have seen in the past–huge price/earnings ratios–40, 50 and 60 times this market is just a bit overvalued and those traders who go short the ‘market’ may see bunches of pain ahead. Of course something could ‘break’ at any time, but as always one who invests in preferreds and baby bonds doesn’t want to see a huge equity tumble–it is not helpful to anyone. When one looks at the amount of ‘dry powder’ available that could move into the equity markets I think there is a higher odds of a ‘melt up’ than a ‘melt down’.

I see Brookfield BRP priced a new issue of perpetual subordinated notes last night–7.25%. The pricing term sheet is here. These are investment grade, but being a Canadian company interest payments are subject to 15% withholding in some acccounts.

Also last night JPMorgan put out a redemption notice on a bunch of $1,000/share fixed to floating preferreds–the press release is here.

I am back in the office after 6 days out and will do a little buying today–not sure which issue–we will see–lots of near cash on hand (money market). Accounts continue to hit almost daily new highs as giant sized CD maturities hit–most of which pay interest only at maturity