Wow the 10 year treasury is now trading at 4.63%–all based upon stronger retail sales continuing at strong levels. The consumer is saying buy, buy, buy–probably taking the credit card out as they just can’t help themselves.

Equities which started the day solidly in the green just couldn’t old gains as interest rates rose and the S&P500 is now down almost 1%.

Accounts are mostly red again today–worse than last week. I am eyeballing the RiverNorth Opportunities Fund 6% preferred (RIV-A) for my ‘safe’ bucket as it is off more than a buck in the last week with current yield approaching 6.50%–we’ll see if I take a nibble–maybe tomorrow. I like this issue at 6.50% with a A1 Moodys rating.

Well let’s see where the afternoon goes—no doubt there a fair amount of fear in the markets. I am not a seller–and not yet a buyer, but maybe soon.

Last week was a relatively exciting week–not necessarily in a good way, but lots of movement in stocks and bonds. Personally I had some damage done to portfolios, but not severe and will hopefully start to get some of the losses back starting this week. As it turns out most of the damage in income issues was done to the high quality (low coupon issues)—not a huge surprise as historically when interest rates move higher the high yield, mid level quality issues hold up best.

The S&P500 fell by almost 2% lost week, although the index had been down somewhat more on Friday. While the index fell on Wednesday as the CPI was announced at a somewhat hotter level than forecast it bounced back Thursday as PPI was tame, but once again tumbling on Friday.

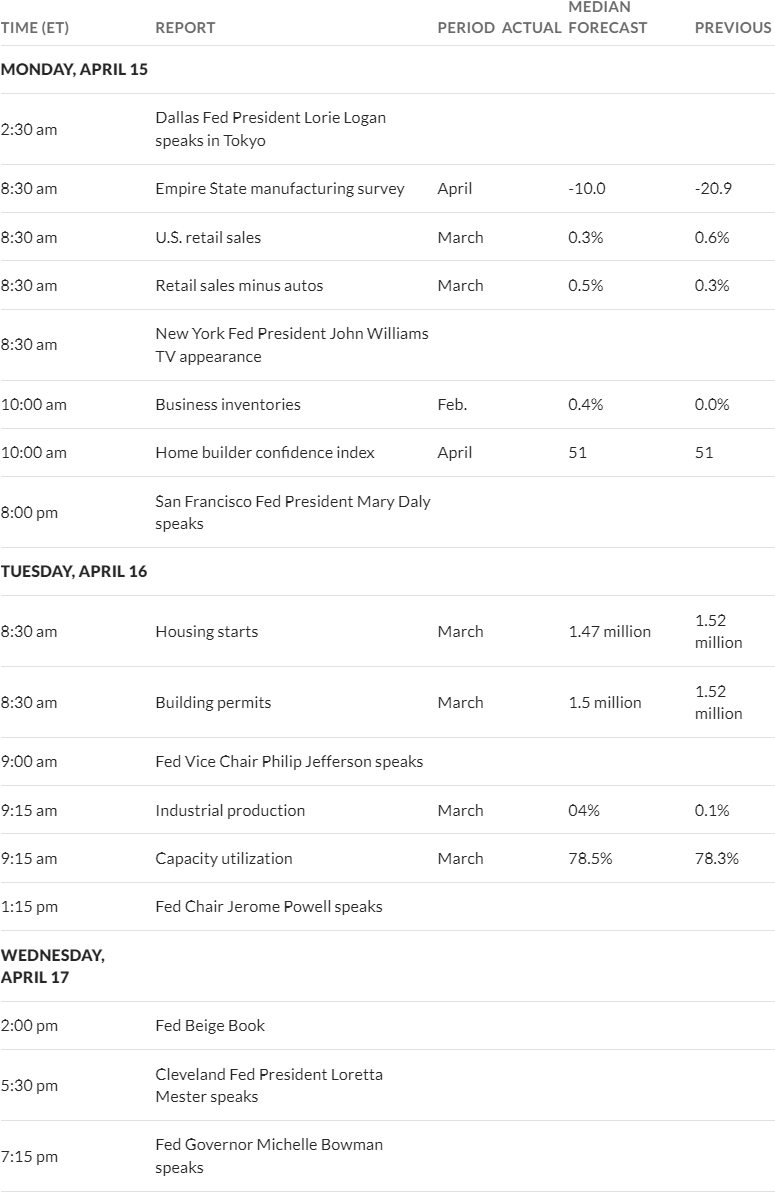

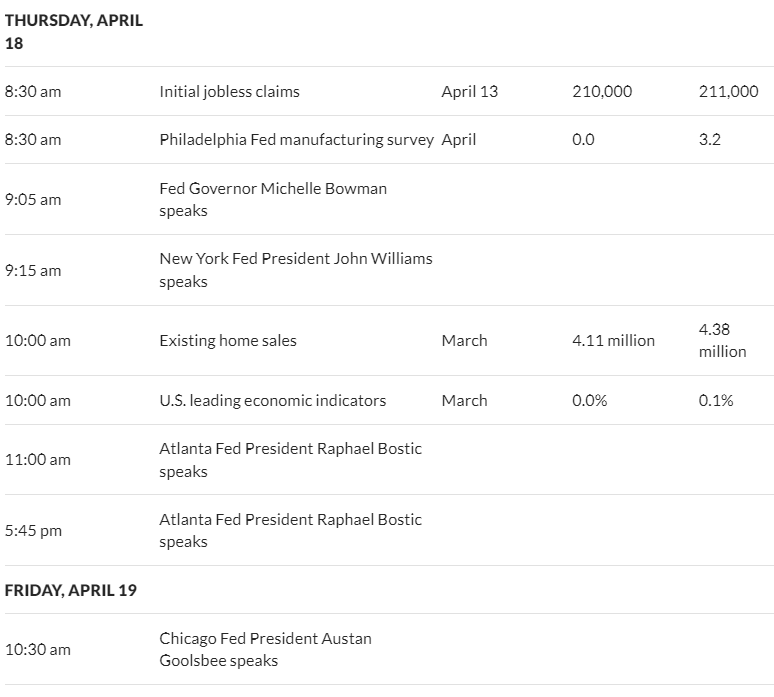

The 10 year treasury closed the week at 4.50% which was up about 12 basis points on the week. The yield had been as high as 4.59% on Thursday. The close of 4.50% was the highest yield we have seen since last November (on a weekly closing basis). This week we see leading economic indicators on Thursday and sprinkled throughout the we see housing numbers–home builder confidence, building permits, existing home sales and housing starts. We also see the ‘beige book’ for a rundown of what each Federal Reserve district is seeing in their area. And of course we will have the war situation in the middle east hanging over the markets.

The Fed balance sheet fell by $1 billion. Right now we can count on the assets to fall by the planned $90-95 billion each month–although the runoff will be somewhat lumpy. There is talk of reducing the runoff in the next couple of months.

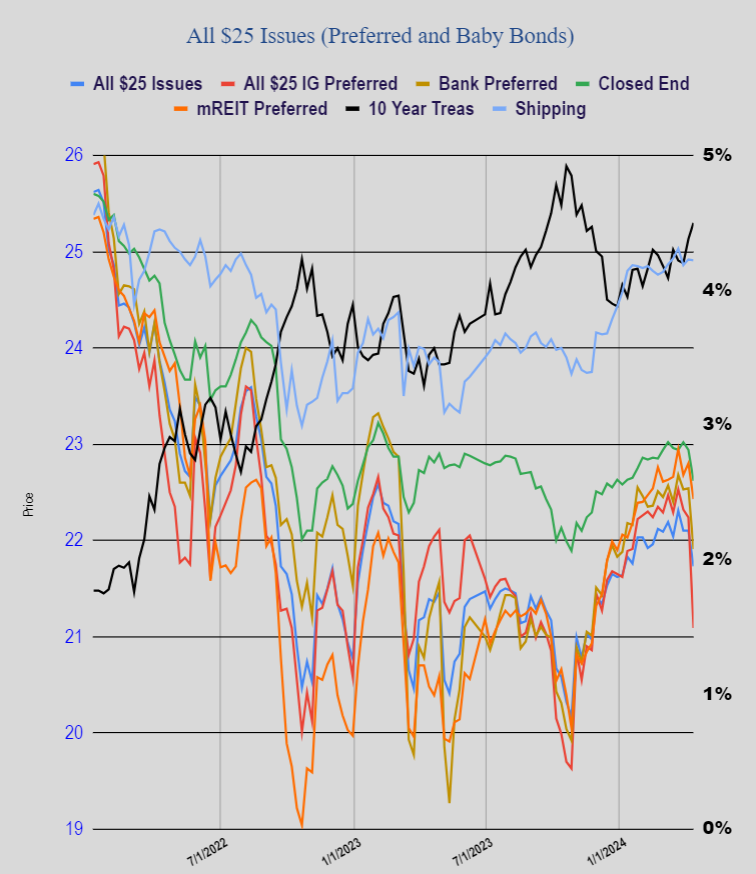

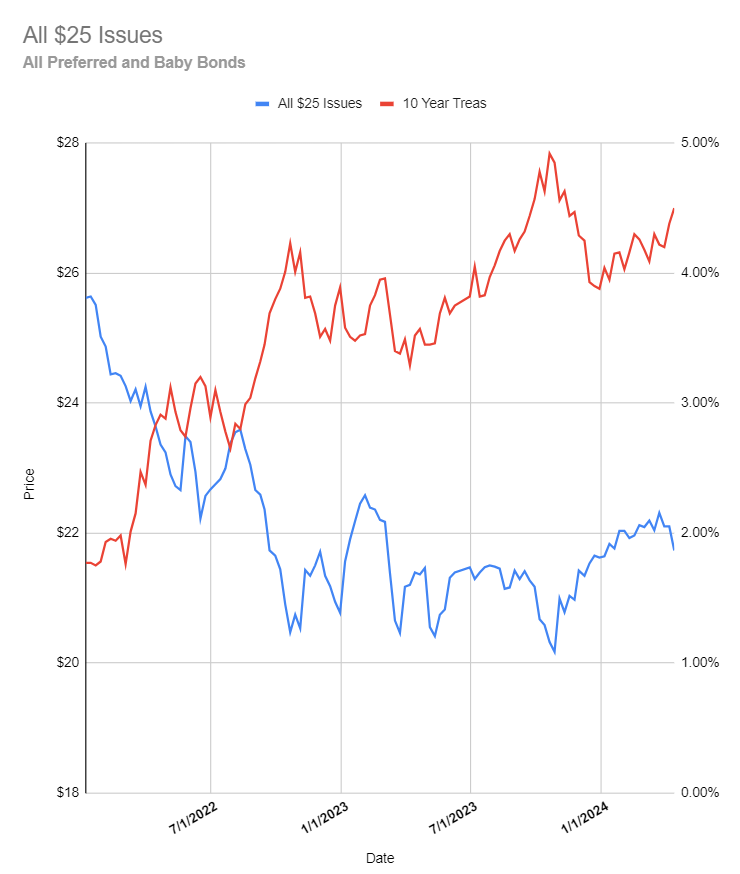

Last week the average $25/share preferred and baby bond fell by 1.7% (37 cents), which puts the average share at $21.73/share. Investment grade issues were beaten badly – down about a dollar, banks down by 63 cents, mREITs down 37 cents and shippers fell by just 1 cent.

Last week we had 1 new income issue price with a new baby bond from Great Elm Capital (GECC). The issue priced at 8.50%.

Here is my observation in this area of Minnesota. Many, many houses are sold with FHA or USDA loans—mostly with little to no money put down on a down payment. Realtors were many times telling folks that ‘yes rates are high’, but ‘when rates come down to normal rates you can refinance and lower your payment’ – implying 3-4% rates were normal.

Us ‘old folks’ know that 3-4% were abnormal rates–the exception, not the rule. When you have a giant sized portion of FHA and USDA loans you are in dangerous territory–when you have no ‘skin in the game’ so to speak just walking away is pretty darned easy.

We’ll obviously have to see where rates go, but the higher they go not only will we see a slower housing market, but the level of foreclosures will begin to rise. High rates for a few months–no big deal. High rates for a year or two–trouble.

Well it is Friday and from an interest rate perspective it has been a tough week–the 10 year treasury is now trading at 4.54% after hitting a high of 4.58% yesterday–20 basis points higher than the close last week. Of course we lost some money this week, but it has been a long time since we have had a losing week and with the high allocation to CDs these losses are very manageable–but I hope we don’t see these losses on a regular basis. I haven’t calculated the average $25/share preferred and baby bond loss on the week, but I would be surprised with anything less than 25 cents/share–I am guessing more like 50 cents. On the other hand we all know that if you had some shorter duration term preferreds and/or baby bonds your loss might have been just a dime or so—portfolio construction makes a huge difference.

Yesterday we saw a producer price index (PPI) number that was better than expectations. 1st time unemployment claims were at 211,000 versus a forecast of 217,000. Employment is not showing any signs of stress–certainly not any that is adequate to make the Fed think they are too tight–as you might remember I think the Fed is looking at employment as a key indicator.

You likely saw that short seller Fuzzy Panda (yes really Fuzzy Panda) has come out with a hit piece on Globe Life (GL) which has a baby bond outstanding (GL-D). The baby bonds fell to $14.94 late yesterday. I read through the accusations and all I can say is WOW. Either this is a company out of control OR someone has a vivid imagination. Whether this is balony or not I don’t get involved in this stuff–I have plenty to worry about without involvement.

So I close the week sitting on my hands–no buys or sells. For those believing interest rates have peaked there certainly were bargains available this week—even I am tempted–maybe next week.

Today we have the producer price index (PPI) on the calendar—the forecast is for prices to decrease—both the headline and core. After the hot CPI numbers yesterday this would be welcome. We also have a gaggle of Fed yakkers today–at least 4–to them I say ‘shut up–if you don’t agree on the future fine–but none of you knew what to do when we were at zero interest rates and none of you know what to do now. Let’s be data dependent!

Yesterday ended up being fairly painful–most of our accounts were down around .3%. It has been so long since we have seen losses like this that the reality of the loss is better than temporary mental pain. I suspect with our portfolios only 1/2 invested in preferreds and baby bonds and a steady stream of interest payments coming in that this loss was minimal.

Yesterday the 10 year treasury closed around 4.56%–17 basis points above the previous close. It has been a long time since we have gotten a spanking like this–I don’t think we will see a rise like this anytime soon–even a hot PPI today won’t get this reaction. BUT as I have mentioned time and time again I believe that we will see rising rates later in the year as treasury issuance of new debt overwhelms demand and investors ‘demand’ higher payments. We’ll see.

Obviously no buying or selling yesterday for me–can’t see any today or tomorrow excepting for CDs as more maturities of CDs keep rolling in. We’ll see what prices do–maybe next week I will add to issues that have been beaten down, but with my outlook on rates it doesn’t seem to make sense to add anything but shorter dated maturity issues.

Equities are off this morning–not dramatically, but 1/3%. After yesterday we could well see a bounce if PPI comes in at forecast, but we are going to have lots of uncertainty in the weeks ahead so it would seem to me (and what do I know?) that upward traction will be hard to come by with inflation keeping the pressure on interest rates.

With the hotter consumer price index this morning interest rates moved a full 12 basis points higher—up around the 4.50% area—ouch.

Holders of high quality, low coupon perpetuals and baby bonds with LONG dated maturities are experiencing some pain–the amount of pain is dependent on the construction of your portfolio. Short dated maturities have experienced significantly less pain. Even with my conservation portfolio construction I am off around .3% today and that is plenty painful.

IF one thought this was the high in interest rates one might say there are bargains being created today. Unfortunately I don’t believe we have seen the high–so of course i am not a buyer of long dated maturities in baby bonds or perpetual preferreds.

Certainly, I am not a seller of anything today–some issues which are falling I wish I didn’t own TODAY—but they are solid and will, over time, bounce back. This is simply life if you invest in anything at all.

Great Elm Capital (GECC) has priced the previously announced new baby bond issue with a coupon of 8.5%. The issue is rated BBB by Egan Jones.

Being debt this issue will not trade on the grey market–and likely won’t begin to trade for a week or 10 days. While one might be able to buy from their broker ‘bond desk’ this is little (if any) advantage to by before exchange trading.